The Egyptian telecoms market is one of the largest in the MENA region, presenting considerable opportunities for growth. 4G will underpin future investment coupled with opportunities for new build, co-locations, tenancy amendments and rural connectivity. Such opportunities have recently piqued the interest of international tower companies who are vying for two newly issued infraco licences, which TowerXchange expects to be issued by early 2020. TowerXchange examines the tower landscape and growth opportunities, putting Egypt in the spotlight.

Egypt’s tower landscape

There are around 24,000 sites in Egypt with an even split between Vodafone, Orange and Etisalat. Telecom Egypt (through the brand WE) had built 1,300 by the end of 2018 (data from Telecom Egypt 2018 Annual Report), and are working on reaching 2,000 sites today. Approximately two thirds of Egypt’s sites are ground based towers, with one third being rooftop sites, primarily in major urban areas. In 2010 and 2011, five Egyptian companies were awarded licenses to lease space on towers. The five companies were EEC, Alkan, ECMTS, Mobiserve’s Mobitower and HOI MEA, with each being awarded a license for a 15 year period. TowerXchange understands that of those five licenced towercos only HOIMEA has built and leased space on towers, and only on 38 sties which the company is reportedly looking to sell.

There has been much bilateral sharing between operators in the market because of the high number of subscribers per tower. For example, of the 6,166 towers that Orange owns, they share 20% (1,208) with other MNOs. They also lease space on 1,071 towers owned by other operators in the market. Most of the towers built in Egypt are thought to be relatively robust structures and so capable of carrying two or three tenants and so additional co-locations are thought to require only minor structural modifications. Rooftop sites are prevalent in the major cities, with over 90% of Cairo’s sites being rooftop structures. These structures are inherently less suited for co-location and so much of the opportunity for increasing tenancy ratios will be outside of the major metropolises.

Grid connection for tower sites is slow and expensive and so generators are widely used, often two per site due to the high loads. Fuel remains cheap by international standards and so the case for hybrid solutions is reduced; although fuel subsidies are gradually being phased out. MNO’s are looking to attract international investment into green energy with the operators looking to deploy hybrid/green solution in the coming years.

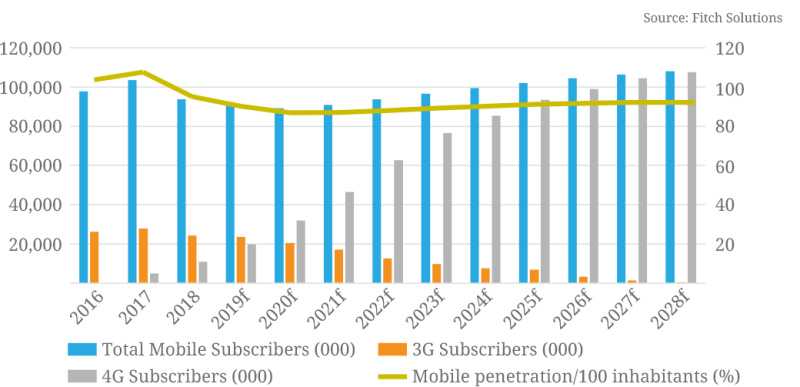

Figure 1: Total number of mobile subscribers

Towerco Opportunities

There have been no tower transactions of scale in the market, however the region has attracted international interest for some time and a number of towercos have vested considerable time and resource on the ground assessing the opportunities that exist. High requirements for new build and co-locations has attracted the interest from American Tower, IHS Towers, Digital Bridge and Eaton Tower all being linked to potential opportunities in the market. In a bid to enter the market, licences have been applied for and it is understood that the regulator (NTRA) is due to issue two new licences, with one being awarded to a major international towerco, by Q1 2020.

With one of the highest number of SIMs per tower in the world, a growing subscriber base, rollout of 4G just beginning, and operators in need of expanding their network, the potential for new build in the market is high. In order to increase 4G capability and capacity, all four MNOs are planning new build sites. In a bid to raise its profile and market share, Orange is looking to add 700 new sites starting with an estimated 200-300 sites in early 2020. Whilst Telecom Egypt currently has up to 2,000 towers it has recently entered its second phase of network rollout with a deployment of an additional 1,500 sites. The operator is also projecting 1,000 new build sites to be rolled out starting with 200-300 in early 2020. Etisalat and Vodafone are expected to be planning to add 300-500 new towers per year over the medium term.

With devaluation of the Egyptian Pound, a need to invest in 4G equipment and potentially buy additional spectrum to keep up with 4G demand, Egypt’s MNOs are looking at how to best manage their capex: giving towercos build to suit contracts instead of investing in new site build themselves represents one such strategy.

For a towerco, this presents an exciting proposition; a potential of 1,500-2,000 new BTS sites with the four MNOs. There is a healthy co-location potential on sites and opportunities for decommissioning also exist with significant parallel infrastructure in the country.

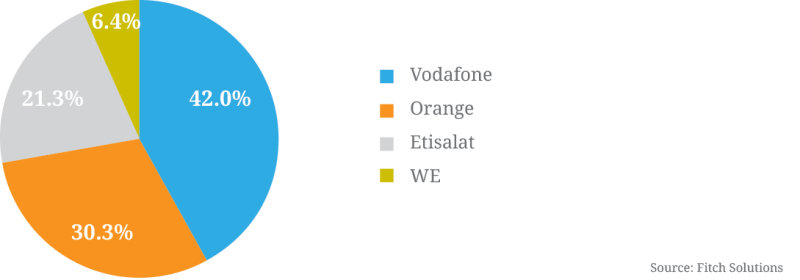

Figure 2: MNOs Market Share

Egypt’s mobile market

The mobile market in Egypt is one of the largest in the region. There are four mobile network operators serving a combined market of 93.986mn subscribers as of June 2019 (source: Fitch solutions)

Disruption following the launch of new 4G-only WE led to market turbulence and from 2017 to 2019, the number of subscribers in the Egyptian market dropped by 10% to just over 90 million, but growth is expected to resume sometime during 2020 with mobile subscriber growth to increase from 2021 onwards at a rate above 3% annually. According to Telecom Egypt, 61% of population is below 30 years and c.2mn new customers enter the market annually and Fitch Solutions expect 4G to reach 90% penetration by 2025. There has been competition on pricing amongst the operators, in an effort to defend their established businesses from Telecom Egypt-backed newcomer WE, however operators are also conscious as to not sacrifice too much revenue by competing too aggressively on pricing.

State owned fixed telecommunications operator Telecom Egypt being the newest market entrant, directly launched 4G mobile services in September 2017. Telecom Egypt, which operates under the brand “WE” joined established operators Vodafone, Etisalat and Orange in the country. The award of a mobile license to Telecom Egypt was given as part of a new regulatory framework approved in 2016 by the National Telecommunications Regulatory Authority (NTRA).

According to this regulatory framework, the existing mobile operators Orange, Vodafone and Etisalat were allowed to introduce 4G service beside their 2G and 3G services, and the incumbent operator Telecom Egypt (TE) was allowed to provide 4G services and provide 2G and 3G services through national roaming with the existing mobile licensees. In addition, the regulatory framework allows Orange, Vodafone and Etisalat to provide virtual fixed-line services using Telecom Egypt’s network.

Telecom Egypt-controlled WE is still rolling out its infrastructure and it will be several years before it can claim to have a fully national presence of its own; in the meantime, it is using the networks of Etisalat Misr and Orange Egypt to fully service its customers’ 2G/3G/4G connectivity needs.

Market leader Vodafone saw a fall in its subscribers from 42.3mn to 39.5mn in June 2019, giving them a market share of 42%. Although its share is declining, it leads by a considerable margin and is shrinking at a slower pace than second-ranked Orange. Orange (which operated under the Mobinil brand until 2016) has dropped it market share by 2% in a 12 month period to 30.3% as of June 2019 (source: Fitch Solutions).

Etisalat, which has been steadily losing market share, has 21%. Commercial launch of 4G networks by all four MNOs was achieved in 2017, although 4G coverage is primarily only available in Cairo with major rollout still required elsewhere, including rural areas. It is expected that 3G will be phased out and the rollout of 4G will be widely available within all areas of the country.

With high demand for 4G services expected to keep increasing, each of the operators requested additional spectrum from the regulator. The agreements Telecom Egypt had in place while it builds out its 2G, 3G and 4G networks will come to an end by 2022, meaning the next couple of years are crunch time for reaching national scale through its own network.

Egypt’s ICT 2030 Strategy

Egypt’s Ministry of Communications and Information Technology (MCIT) has plans to build a new telecoms network at an estimated cost of EGP40 billion (USD2.44 billion) as part of the first phase of development of the country’s proposed new capital city. Financed by the Administrative Capital for Urban Development (ACUD,) the new capital’s owner and developer, the work is expected to begin over the next six months. The MCIT is striving to achieve a digital economy and Egypt’s Information and communications technology (ICT) 2030 strategy supports the development of the communications sector both regionally and internationally which will undoubtedly contribute to the economic growth of the country.

The NTRA is also currently developing telecom infrastructure in several smart cities within the framework of announced national strategic projects. In 2017, Egypt announced plans for 5G trials, further underscoring the importance of digital transformation in their future. In March 2019 Telecom Egypt and Nokia signed a MoU to introduce a 5G network and test use cases.