The Central and Latin American telecom infrastructure landscape is undergoing considerable changes and 2020 is expected to be an exciting year across the region. Towercos (or should we call them infracos?) are finally eyeing opportunities beyond macro-towers and MNOs are actively exploring synergies and tower sales in preparation for 5G.

We have seen an unprecedented volume of acquisitions and consolidation moves over the last few months, including PTI’s addition of Telefónica’s assets in Ecuador and Colombia, Digital Colony and IHS’ debuts in the Brazilian market and Entel’s sale to ATC in Chile and Peru. Further, Oi and Telefónica have both announced their intention to divest considerable portions of their respective businesses while other MNOs keep assessing SLBs and gearing up to invest in 5G.

In the meantime, innovators and infrastructure leaders continue exploring new streams with the likes of American Tower and Phoenix Tower International scooping up existing fibre portfolios while starting to deploy their own dark fibre. The arrival of 5G will have a huge impact on the industry and regional MNOs are speeding up their 4G rollouts in order to be ready for the transition towards this new - and somewhat still mysterious - technology. Countries like Brazil, Chile and Peru are expected to hold spectrum auctions over the next few months while towercos are exploring new site typologies and trying to adapt their business model to better satisfy their customers’ changing requirements.

In this analysis, TowerXchange takes a close look at each country’s telecom infrastructure market, its characteristics and reports on the latest tower counts from across the region.

Mexico

The Mexican BTS market continues to grow, mainly due to the expansion of Red Compartida, with most towercos reporting tens of new towers in their portfolios. In the meantime, Phoenix Tower International entered Mexico where it now owns 974km (or 17 rings) of fibre and 355 sites.

As of January 2020, ALTÁN Redes’ Red Compartida covers more than 51% of the country’s population. Promtel estimates that the country has invested over US$638mn on the project’s deployment and the new network includes more than 4,400 BTS, 32,350 km of fibre as well as four data centers. In fact, the project has committed to cover 92.2% of the country’s population and will start focusing now on rural areas, which will drive a considerable demand for new macro sites in remote and challenging locations.

In November, Movistar signed a last mile wireless capacity agreement with AT&T to access its competitor’s 3G and 4G networks, hence AT&T and the whole tower industry will have to make considerable amendments and investments to adapt to this shift. Meanwhile, América Móvil has announced an investment of US$8,500mn to deploy fibre, towers and new technologies as the company is also getting ready to provide triple play services in the country.

The MNOs, that contract power through state-owned CFE, are now exploring the integration of renewables to cut down energy costs and looking to sign Power Purchase Agreements with the many international and local providers that are offering affordable power solutions across the country.

Mexico – Estimated tower count 34,285

Breakdown of ownership of CALA’s 192,968 telecom towers (Q1 2020)

Central America and the Caribbean

Telefónica is now finalising the transfer of its assets to Millicom and América Móvil hence the three MNOs are dealing with the different regulatory approval processes of each country. Towercos operating in the region are losing a client but new entrant Tigo and consolidator Claro are expected to invest big to complete their 4G rollout while focusing on rationalisation and network optimisation.

Belize has 379.7K connections and 100% penetration rate as of Q4 2017 according to GSMA Intelligence. With two carriers, DigiCell and Smart, and no active towercos to date, the country is too small to attract much attention from the tower industry, and our estimates suggest there are approximately 70-80 towers in the national territory.

Central America market highlights

- América Móvil’s takeover of Telefónica in El Salvador on hold, Guatemala completed

- Millicom closes deal with Telefónica in Nicaragua, Costa Rica and Panama

Costa Rica and Panama continue to be the most dynamic and interesting countries in the region, as the existence of three and four MNOs respectively guarantees good tenancy ratios and plenty of technology innovation in preparation for 5G.

Since telecoms were liberalised in 2008, Costa Rica has proved an increasingly fertile ground for towercos. Costa Rica’s regulator SUTEL, supported by the National Telecommunications Fund, has awarded two contracts to the state-owned utility Grupo ICE-which offer telecom services under Kolbi-to supply telephony and broadband services to 14 indigenous territories in the Atlantic and South Zone of the country. The initiative will receive around US$48mn from the government and will increase the demand for macro-sites in the included territories. SBA Communications remains Costa Rica’s largest towerco with 869 sites, followed by American Tower and Telesites. PTI, Continental and a handful of local firms complete the roster of towercos, who own over half the country’s towers between them.

In Panama, Millicom is set to invest over US$750mn over the next five years and towercos are currently exploring new typologies to satisfy the increasing densification needs of their MNO partners.

Costa Rica - Estimated tower count 4,063

Costa Rica quick facts

Towers 4,063

SIMs per tower 2,565

Mobile connections 8.6mn (Q4 2017)

Population 4.9mn (Q4 2017)

SIM penetration 175% (Q4 2017)

MNOs Kölbi, Tigo*, Claro

Towercos SBA Communications, American Tower, Continental Towers, Telesites, Phoenix Tower International, TOCSA

* Millicom in the process of taking over Telefónica

Source: GSMA Intelligence, TowerXchange

Panama - Estimated tower count 1,726

Cuba’s SIM penetration grew from 29% in Q4 2015 to just 40% in Q418 according to the GSMA, but that isn’t enough to get anywhere near the regional average. With only one mobile network operator in the country, ETECSA, who share around 500-700 towers with radio companies and TV stations, it will take some time for international towercos to be able to enter the island. However, TowerXchange is keeping a close eye on Cuba in light of its untapped market and undisputed potential to become a target of international towercos should the telecom market liberalise.

The only towercos active in the Dominican Republic are Phoenix Tower International, which runs a portfolio of almost 1,800 sites and Torresec.

PTI scaled its Dominican Republic’s operations thanks to a string of acquisitions including Teletower Dominicana’s 190 sites, Viva’s 545 towers’ portfolio and, lastly, the agreement to purchase the assets of Teletorres del Caribe, owned by Altice Europe (1,049 sites) for US$170mn.

Following a regional trend, market leader Claro, who owns around 1,400 towers in the Dominican Republic, is now integrating renewable energy in more than 40 sites across the country and plans to continue expanding its renewable energy use to power towers nationally.

Dominican Republic quick facts

Mobile connections 8.5mn (Q4 2017)

Population 10.8mn (Q4 2017)

SIM penetration 78% (Q4 2017)

MNOs Claro, Orange, Viva

Towercos Innovattel, Phoenix Tower International

Source: GSMA Intelligence, TowerXchange

In February, Tigo El Salvador sealed an agreement to sell up to 800 towers to SBA Communications for US$145mn. SBA Communications owns and operates 242 sites in El Salvador and this deal with exponentially grow the company’s footprint.

El Salvador - Estimated tower count 1,809

El Salvador quick facts

Towers 1,809

SIMs per tower 5,704

Mobile connections 9.6mn (Q4 2017)

Population 6.4mn (Q4 2017)

SIM penetration 150% (Q4 2017)

MNOs Claro, Movistar, Digicel, Red, Tigo

Towercos SBA Communications, Phoenix Tower International, Continental Towers

Source: GSMA Intelligence, Phoenix Tower International, TowerXchange

Guatemala is a complex country with a very competitive tower industry. SBA Communications, Torrecom, Balesia and Continental all operate in the local market which is characterised by a fairly strong regulatory environment and the huge influence of local communities – Consejos Comunitarios de Desarrollo Urbano y Rural (COCODES) – in the approval of new deployments. In spite of these difficulties, Torrecom and SBA Communications have achieved good levels of organic growth in the country and have added a combined 300 towers since Q2 2015. In October, Phoenix Tower International entered the market with the acquisition (from an unknown seller) of twenty towers.

Local billionaire Mario Lopez owns substantial equity in market leaders Tigo, and also owns most of the land under their towers, which makes the operator reluctant to participate in widespread infrastructure sharing. Could Tigo consider selling any of its assets following the sale and leaseback deals in Colombia and Paraguay?

Guatemala - Estimated tower count 4,002

Guatemala quick facts

Towers 4,002

SIMs per tower 5,380

Mobile connections 19.8mn (Q4 2017)

Population 17.1mn (Q4 2017)

SIM penetration 116% (Q4 2017)

MNOs Tigo, Claro, Movistar

Towercos SBA Communications, Torrecom, Continental Towers, Movistar, Phoenix Tower International

Source: GSMA Intelligence, TowerXchange

According to TowerXchange’s research, Honduras is home to two towercos, Balesia and Continental Towers Corp. For now, there’s been little visibility on the local industry and its potential with around 20% towerco penetration and the two carriers – Tigo and Claro – still holding on to their tower portfolios.

Honduras - Estimated tower count: 1,200

In spite of being a high-risk market, Nicaragua presents interesting build-to-suit opportunities. In 2018, the market stalled due to security issues for nearly seven months but now towercos have resumed BTS activities.

Nicaragua - Estimated tower count 1,364

nicaragua-tower-count.png

Towers 1,364

SIMs per tower 7,698

Mobile connections 9.2mn (Q4 2017)

Population 6.3mn (Q4 2017)

SIM penetration 148% (Q4 2017)

MNOs Claro, Tigo, CooTel

Towercos SBA Communications, Torrecom, PTI, Continental Towers

* Millicom took over Telefónica in May

Source: GSMA Intelligence, TowerXchange

In 2018, Phoenix Tower International announced the acquisition of 215 towers from Digicel in the French Antilles. While no further details of the transaction have been shared, this deal solidifies PTI’s position as the first towerco in the Caribbean.

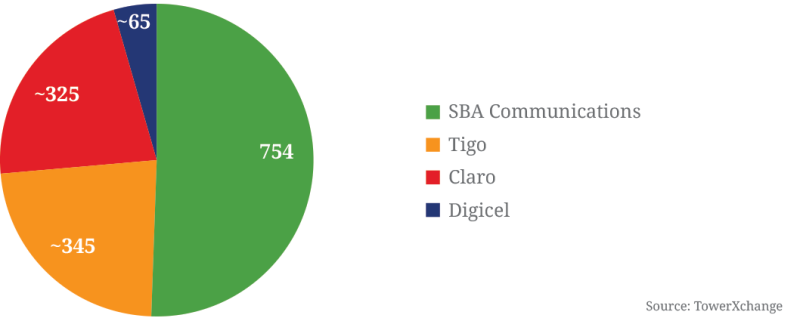

CALA top towercos - Q1 2020

Selected estimated CALA tower counts

Brazil

After a few years of recession with very little organic growth and poor M&A activity, Brazil is emerging again as one of the fastest growing and most dynamic tower markets in Latin America.

Over the last few months, Brazil has seen an unprecedented volume of tower deals and new entrances. Last December, Digital Colony announced the acquisition of Highline do Brasil II from Pátria Investments. Digital Colony absorbed a portfolio of 315 sites and around 180 BTS, creating a new consolidating force in the market. Also in December, Telxius acquired 1,909 sites from Vivo for around US$153mn and last month, regulator CADE approved the acquisition of Cell Site Solutions (CSS) by IHS Towers, which sets the entrance of the African-based player into Latin America and adds around 2,290 towers to the company’s global portfolio of more than 25,000 sites. Consolidation is likely to be Brazil’s number one tower market trend for 2020 as Oi, Grupo Torresur as well as other independent players are evaluating and discussing potential divestments and exits.

Anatel has also announced the terms of the 5G auction, scheduled for November, and MNOs are set to continue investing and rolling out their 4G networks while getting ready for the 5G auction, which will drive the country’s biggest rollout of macro sites, fibre and alternatives typologies to date. Further, the approval of the new telecom law—the PLC 79—will eliminate several restrictions that slowed down network investments for years and towercos are expecting a considerable increase in co-locations while receiving good volumes of BTS orders.

Brazil - Estimated tower count 64,730

Brazil quick facts

Towers 64,730

SIMs per tower 3,879

Mobile connections 221.6mn (Q4 2017)

Population 210.1mn (Q4 2017)

SIM penetration 105% (Q4 2017)

MNOs TIM Brasil, Vivo, Claro, Oi, Nextel, Algar Telecom, Sercomtel

Towercos American Tower, SBA Communications, Grupo TorreSur, Phoenix Tower do Brasil, CSS, Brazil Tower Company, AlfaSite, Centennial, QMC, Skysites, Telxius

Source: GSMA Intelligence, TowerXchange

Who sold their towers in Central and South America?

Bolivia

After many years of failed attempts, Bolivia finally welcomed the first independent towerco in 2019 after Phoenix Tower International sealed a sale and leaseback deal with Trilogy International Partners’ subsidiary NuevaTel. PTI has now a portfolio of 574 sites in the country and is set to continue expanding in Bolivia. Although Bolivia has always been perceived as a “risky market”, its new government and a competitive telco landscape with three solid players can make it a fruitful playground for bold tower entrepreneurs.

Bolivia - Estimated tower count: 4,343

Paraguay

Paraguay is one of the newest markets to open its doors to towercos, following the acquisition by American Tower of 1,400 Tigo’s towers at a value of US$125mn (of which 957 were transferred in Q3 2017). As anticipated, the valuation per tower in the Tigo/AMT deal is lower than the regional average (US$89,285 vs US$199,966). In fact, valuations are affected by the limitations on the length of land leases, currently capped at five years, as well as the rising real estate costs. Along with Millicom’s portfolio, Personal’s 1,100 towers could come to market soon and this would surely increase the interest of towercos in this new market.

In January 2018, the 700MHz spectrum auction took place and generated bids for US$84.5mn. Tigo, Claro and Personal all scooped spectrum allocation while State-backed Vox didn’t enter the bidding process.

Paraguay - Estimated tower count: 4,271

Paraguay quick facts

Towers 4,271

SIMs per tower 1,788

Mobile connections 7.6mn (Q4 2017)

Population 6.9mn (Q4 2017)

SIM penetration 111% (Q4 2017)

MNOs Tigo, Personal, Claro, Vox

Towercos American Tower, BTS Towers, Innovattel

Source: GSMA Intelligence, TowerXchange

Major tower transactions in Latin America 2011/2020

Colombia

Colombia’s long-awaited spectrum auction, which finally took place last December, has reshaped the telecom landscape and is now expected to drive major rollouts among the three winners. While both Claro and Tigo obtained some frequencies, Telefónica didn’t acquire any spectrum and the company could be existing Colombia or at least carving out its remaining portfolio. The Spanish giant has recently closed a sale of 621 sites with Phoenix Tower International. The auction also welcomed new player Novator Partners (the London-based owner of Chilean upstart operator WOM) who acquired 20MHz in the 700MHz band and 30MHz in the 2500MHz band.

The 700MHz spectrum licences include obligations to bring 4G connectivity to 3,658 rural locations across 32 departments, while all rural 4G networks must be operational in less than five years, hence demand for macro sites and co-locations is set to increase exponentially. Further, MNOs will have to modernise their network and are expected to bring new equipment to their current sites, while also signing new partnership to access each other’s infrastructure.

Colombia - Estimated tower count 18,127

Colombia quick facts

Towers 18,127

SIMs per tower 3,626

Mobile connections 56.4mn (Q4 2017)

Population 49.3mn (Q4 2017)

SIM penetration 114% (Q4 2017)

MNOs Claro, Movistar, Tigo, Avantel

Towercos American Tower, SBA Communications, Andean Tower Partners, Centennial, Golden Comunicaciones, Innovattel, Torrecom, PTI, QMC, Telesites, Tower One

Source: GSMA Intelligence, TowerXchange

Ecuador

Ecuador is the quietest of all Andean States especially since its MNO landscape is less attractive for towercos. Claro enjoys a dominant position in the country, while CNT is the government-owned player holding the third spot after Telefónica’s Movistar. In line with its regional strategy, the Spanish telco has recently sold 1,408 sites to Phoenix Tower International, who has become one of the biggest independent towercos in the country.

The government has announced a plan to boost rural connectivity, while incumbent players Claro and CNT have agreed a deal to jointly invest in rural infrastructure in remote areas, which will definitely benefit towercos with strong BTS capabilities in the market.

Ecuador quick facts

Mobile connections 14.5mn (Q4 2017)

Population 16.7mn (Q4 2017)

SIM penetration 87% (Q4 2017)

MNOs Claro, Movistar, CNT

Towercos SBA Communications, Innovattel, Balesia, Aplicanet, Ecuador Tower Company

Source: GSMA Intelligence, TowerXchange

Peru

Until late last year, Peru was one of the less penetrated tower markets in the region. However, the expansion of Telxius-which now has a portfolio of around 1,925 sites-and Entel’s sale of 1,262 sites to American Tower has massively increased the penetration of towercos in the country. Further, Peru’s economy, one of the fastest growing and most stable in the region, and the existence of four MNOs will drive good levels of growth and tenancy ratios.

The Ministry of Transport and Communications has announced a spectrum auction for 2Q20 and the successful bidders will have strong obligations for rural coverage and public connectivity. While both Entel and Claro will continue competing and investing in their 4G networks, it is unclear how Telefónica will move forward in the country. Towercos has been growing steadily and reporting considerable levels of organic growth and co-locations.

Demand for fibre, poles and alternative solutions will increase mainly in urban areas, while remote and rural locations will increase their importance for MNOs, especially after the auction. Last year, Telefónica launched Internet para todos (IpT) alongside Facebook and BID Invest, an open-access, wholesale broadband mobile internet service that is expanding coverage to rural areas.

Peru – Estimated tower count 14,855

Peru quick facts

Towers 14,855

Mobile connections 37.6mn (Q4 2017)

Population 32.4mn (Q4 2017)

SIM penetration 116% (Q4 2017)

MNOs Movistar, Claro, Entel, Bitel

Towercos: American Tower, Andean Tower Partners, Innovattel, Balesia, BTS Towers,

Telxius, Torrecom, PTI

Source: GSMA Intelligence, TowerXchange

Chile

Last December, market leader Entel sold 1,980 sites to American Tower on the MNO’s first biggest sale. The company, who addressed its strategy shift on a recent interview with TowerXchange, is fully embracing the towerco business model and will rely on its infrastructure partners for most of its growth in the upcoming years. Further, Entel will use the cash obtained on its transactions in both Chile and Peru to finalise its 4G rollout while also look at new typologies in preparation for 5G in both countries. Claro will continue investing and Telefónica’s future remains uncertain, as in other regional neighbouring countries.

The country’s telecom regulator Subtel has just closed the consultation process for the upcoming 5G spectrum auction, which is set to take place before the year ends.

Chile - Estimated tower count: 8,890

Chile quick facts

Towers 8,890

Mobile connections 26.1mn (Q4 2017)

Population 18.1mn (Q4 2017)

SIM penetration 144% (Q4 2017)

MNOs Movistar, Entel, Claro, WOM

Towercos American Tower, Andean Tower Partners, Antyl, Balesia, SBA Communications, Telxius, Torrecom

Source: GSMA Intelligence, TowerXchange

Argentina

After another tough socioeconomic year and a government change, the Argentinian tower industry has reduced its growth expectations. The opportunity remains there, as the country still needs around 50,000 towers, but regulatory barriers, a continuously challenging economic situation and a very adverse tax regime are set to continue slowing down the deployment of telecom infrastructure in the country.

The market is very fragmented and towercos own around 1,300 towers. Torresec is the market leader with 407 sites, followed by Telxius. GME Alliance, one of the first market entrants, has a portfolio of around 100 sites, while Atis Group, who received a US$100mn injection from Pátria Investimentos, has successfully developed 151 towers in the last couple of years. ATC, PTI and SBA are also present in the country with relatively small portfolios, awaiting for the industry to finally pick up.

Both Claro and Telecom will continue investing and growing their network at a slow pace during the first six months of 2020, hoping to rollout more agresisively in 2H20. Movistar plans remain unclear.

Argentina - Estimated tower count 17,324

Argentina quick facts

Towers 17,300

SIMs per tower 3,777

Mobile connections 61mn (Q4 2017)

Population 44.5mn (Q4 2017)

SIM penetration 137% (Q4 2017)

MNOs Claro, Movistar, Telecom Argentina

Towercos American Tower, SBA Communications, Atis Group, Innovattel/Torresec, Plata Tower Company, Teletower Argentina, Tower One, Telxius, CSS, GME Alliance

Source: GSMA Intelligence, TowerXchange

While the CALA tower industry continues to develop and reshape, we invite all regional tower experts to the fifth annual TowerXchange Meetup Americas, taking place at the exclusive Boca Raton Resort & Club (Boca Raton, Florida), 23-24 June 2020. For more information, click here.

The evolution of the CALA telecom tower industry 2013-2019 (Q3)