For a couple of years, Indonesia was a relatively quiet tower playground. This mature market enjoyed healthy levels of organic growth and welcomed some innovation initiatives from both towercos and MNOs, but besides Protelindo’s expansion and diversification efforts, the country’s tower industry didn’t offer any major news. After a few quiet years, Indonesia is finally enjoying a new wave of sale and leaseback deals while preparing for the potential entry of international investors and the planned exit of some private equity firms. In the meantime, 4G upgrades and 5G tests will guarantee plenty of opportunities for organic growth and new technology deployments.

Take the money and build

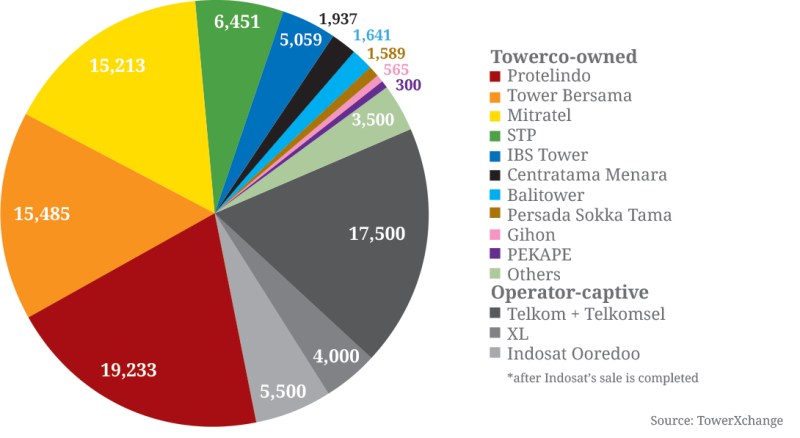

Last month, Indosat Ooredoo, the Indonesian unit of Qatar’s Ooredoo Group, finally announced the long-awaited sale of 3,100 towers to Protelindo and Mitratel for US$452mn. When the deals officially finalise – presumably before the end of the year – Mitratel will acquire 2,100 sites and Protelindo will absorb the other 1,000 towers from the operator.

Tower market leader Protelindo will add around 1,850 tenancies after acquiring a portfolio that has a higher tenancy ratio than the country’s average and the towerco, supported by Redpeak Advisers, has been able to obtain a better price than Mitratel. The deal reinforces Protelindo’s leadership and consolidation plans, while representing a relevant shift in Mitratel strategy as until now, its major shareholder PT Telkom was evaluating potential mergers and even a sale of the infrastructure subsidiary. Indonesia’s tower market evolves towards a three-player dominated scenario where Protelindo, Mitratel and Tower Bersama are expected to continue absorbing smaller players while also acquiring sites from the country’s populated MNO market.

For Indosat, this sets its first sale since 2012, when the company closed another sale and leaseback deal with Tower Bersama – but it will not be the last as the MNO still owns an inventory of 5,000 towers with the “on sale” tag hanging on them. Indosat has historically used its towers as a debit account, but this specific deal is not just about monetisation and will also enhance and maximise the benefits of the operator’s partnership with its infrastructure associates. Indosat has an aggressive rollout plan, aiming to catch up with competitor Telkomsel – which will require the MNO to enhance its expansion efforts beyond Java. This SLB agreement will strength the MNO’s relationship with counterparties Protelindo and Mitratel, who will be able to release financial pressure and offer more strategic locations, while building towers quicker, cheaper and more effectively.

Furthermore, Indosat’s competitor PT XL Axiata is also trying to sell its remaining passive assets and the other MNOs might follow. XL, who is the second biggest operator in the country, is trying to bulk up its balance sheet through the release of 4,500 sites on a deal that could be worth around US$500mn. The operator can use the money to pay down debt and accelerate its expansion outside Java too. The stock market would welcome the transaction; in fact, XL’s share price has notably increased since announcing its intention to sell earlier this year. The MNO would not have to deal directly with land leases and permitting, which remain critical challenges for new rollouts in Indonesia, and it will leverage towercos expertise and scalability while focusing on its core business.

Estimated tower count for Indonesia

Organic growth forecast

More good news – on top of potential acquisitions, Indonesia still holds plenty of greenfield opportunities and towercos are reporting very good volumes of BTS in a “big capex year”. Organic growth has been picking up since 2017, with MNOs rolling out 4G aggressively as well as expanding outside Java. Data demand continues to grow exponentially and this will drive more and more deployments, while the big players are also reporting a huge increase on co-locations.

In fact, the first nine months of the year have been the period with the highest organic growth in Protelindo’s history, as reported in Sarana Menara’s Q3 2019 results presentation. The company has added 3,375 new revenue-generating leases and has more than 1,100 new leases in the horizon.

The operators are all in and Indosat Ooredoo has committed to invest over US$2bn for its network expansion over the next two years. The company has already completed an overlay of its 3G sites with 4G equipment and is set to continue expanding outside Java trough build-to-suit and co-locations.

Market leader Telkomsel won’t be deploying as aggressively but will rather focus on site upgrades. In the first three quarters, the MNO has already deployed 22,000 4G LTE base transceiver stations on its national network while also expanding coverage across the country’s “disadvantaged, frontier and outermost (3T) regions as parts of Indonesia’s Universal Service Obligation (USO)”.

XL will continue expanding, perhaps not as much as the previous couple of years, when the company deployed many new sites. Contrarily, fourth player Hutchison 3 is definitely stepping up its game to steal some market share from the above leaders. The MNO is building 8,000 new 4G and 4.5G-enabled BTS and targeting between five and ten million new subscribers in 2019. On a strategic plot twist, Hutch has closed a deal with Protelindo to renew 85% of around 6,000 leases expiring in between now and 2022, and the MNO has also announced its plans to add around 18,000 base stations to its network. Towercos have plenty of new business in the pipeline!

Fibre, DAS and more

The imminent arrival of 5G and the search for new revenue streams are pushing Indonesian towercos towards innovation. In addition, the traditional tower market is maturing and both fibre and data centres are becoming attractive targets for strategic and financial expansions for both towercos and investors.

Protelindo, who has closed two strategic fibre acquisitions in recent years, is now building two different fibre networks while also fibrerising existing sites in an effort to meet MNOs requirements and gain a competitive edge in preparation for 5G.

STP is also investing on diversification and improving its value proposition with fibre and DAS. To date, the company has 37 indoor DAS networks and 3,000 km of fibre optic networks throughout the country, including 1,643 km in the Greater Jakarta Region. STP is also exploring new site management alternatives and has recently closed a partnership with NTT DoCoMo to test the use of drones for its sites inspection.

Small cells, IBS and DAS will continue increasing their presence, especially due to the restrictions against macro-towers now in place in major cities like Jakarta.

PE exits and new foreign investors

Last year, the Indonesian government announced its intention to relax some restrictions on Daftar Negatif Investasi, the country’s Negative Investment List which is restricting international investment in certain industries, including telecom infrastructure. Since the announcement, representatives from the U.S. Government and even some North American towercos have been meeting with the Ministry of Communication and Information Technology while officials at the U.S. Embassy have been organising some activities and discussions with local authorities to support the idea.

In October, the President Joko Widodo appointed his new cabinet and reinforced his intention of opening up the country’s economy through changes on the negative investment list. Although the possible consolidation on the MNO front could discourage international players, many towercos and big funds have their eyes on the market and this “opening” could absolutely reshape both Indonesia’s and the whole regional Asian tower landscape.

Moreover, there have been many rumours about STP and IBS’ investors looking for a buyout so if the country reduces restrictions on foreign ownership, international players can make a big entrance by acquiring existing portfolios. Alternatively, Protelindo, Tower Bersama and Mitratel might be interested in consolidating their position further.

The country is one of the early embracers of the traditional towerco business model in Asia and despite being one of the most mature markets in the region, is again becoming one of the most attractive ones. Operationally, innovative vendors and suppliers can pursue prolific partnerships with towercos that will continue increasing their portfolios with new builds. Financially, lenders, legal experts and private equity investors will definitely have lots of fun with the current M&A forecast. And indeed, MNOs will continue expanding across new regions, while also demanding fibre and new structures for urban densification in the transition towards 4G and 5G. Removing telecom infrastructure from the negative list could be a huge game changer and global investors and towercos will be following the news closely. Innovation, diversification and M&A opportunities in the country will be again discussed at the 6th TowerXchange Meetup Asia where Protelindo, Indosat Ooredoo and Redpeak Advisers among many others will gather to analyse all the growth opportunities that the market holds for innovative towercos, investors and vendors.