A thriving independent tower industry has emerged in China, providing invaluable supplementary construction capacity alongside China Tower. Independent towercos own just under 80,000 sites in China – that’s around half the total in either Sub-Saharan Africa or Central and Latin America. To understand the economics and investment opportunities in Chinese independent towercos, TowerXchange spoke to our old friend Jiatu Zheng, General Manager of the China Independent Tower Alliance (CITA), which was inaugurated in 2017.

TowerXchange: What is driving the growth of the independent towerco market in China?

Jiatu Zheng, Secretary General, CITA:

With the rapid development of mobile Internet and Internet of Things (IoT) technologies, the demand for wireless data and wireless network points of presence increases greatly. To meet the increasing demand for wireless data communication, a large number of sites for communication base stations need to be constructed to meet the requirements of communication networks. Especially in densely populated urban areas, customers have high requirements for seamless coverage of data signals. Therefore in public places such as urban roads, parks, squares, and commercial pedestrian streets, a large number of cell sites need to be constructed to meet the signal requirements of wireless networks. To achieve quick site deployment, future cell sites must meet basic functions and integrate hardware devices such as municipal street lamps, public security surveillance, and smart city infrastructure to achieve resource sharing.

TowerXchange: Please help our readers understand the unit economics of the independent tower sector in China: what does it typically cost to build a tower? What are typical lease rates for one, two and three tenants? What are typical annual maintenance costs?

Jiatu Zheng, Secretary General, CITA:

There are essentially two types of tower: ground stations and floor stations. Using the ground station as an example, the tower is divided into the common ground station, the landscape tower, and a simple constructed tower. The construction cost varies according to the height. The higher the tower, the higher the site construction cost. If the auxiliary facilities are not included, the construction cost of a tower is between 160,000 and 300,000 RMB (US$22,600-42,400), for a common ground station, from 30m to 50m height. For the landscape tower, from 20m to 40m high, the construction cost is between 90,000 and 210,000 RMB (US$12,700 to 29,700). For a simple tower with a height of less than 20m, the construction cost is about 40,000 RMB (US$5,600).

For the lease rate, for key customers, there is no differential pricing between them . When two key customers co-locate, a 25% discount is granted, and the three tenants are granted a 35% discount. For a common customer, there is no preferential rate. Where two tenants share a tower, a common customer is offered a 20% discount, with three tenants that rises to a 30% discount.

The typical annual maintenance cost of a tower is RMB 3500-6000 (US$500-850).

TowerXchange: How are independent towercos regulated in China? Is there a formal licensing regime for independent towercos in China?

Jiatu Zheng, Secretary General, CITA:

Currently, it is mainly recorded in the provincial communications authority, and there is no other supervision.

There is no formal licensing system for independent towercos in China.

TowerXchange: How does the independent towerco sector function in relation to China Tower Corporation (CTC)? For example, is a city or local network planner allowed to assign a substantial new build project to an independent towerco rather than to CTC?

Jiatu Zheng, Secretary General, CITA:

Independent tower companies and CTC have a competitive and cooperative relationship. This should be viewed with a positive attitude. Our core value is to do a good job in China’s communications industry. Generally, a project is first given to CTC for construction. If CTC cannot handle the whole project, then bidding is opened to independent tower companies.

TowerXchange: How does the MIIT want the independent towerco sector to evolve in China? Would MIIT prefer to see CTC deploy all the new towers, or do they consider it healthy to have competition and capacity provided by a recognised, formal independent towerco segment?

Jiatu Zheng, Secretary General, CITA:

As the most important ministry in the country, the Ministry of Industry and Information Technology, of course, follows the country’s policy. Chairman Xi has made it clear that it is necessary to support the development of private enterprises, stimulate the vitality of all kinds of market entities, and strive to achieve better quality, more efficient, fairer and more sustainable development. This extends to include support for the participation of private enterprises in the communications field and other key areas, encouraging private enterprises to invest in shares, including in the related fields of national infrastructure construction. Independent towercos are a powerful supplement to the construction of communications infrastructure in China, especially in the construction of difficult sites.

As for communications infrastructure construction, there are many difficult sites and special scenarios. The co-construction of CTC and other independent towercos will promote the healthy development of telecom industry. If there were no competition, CTC may refuse to build the difficult sites. If so, how will we achieve full network coverage?

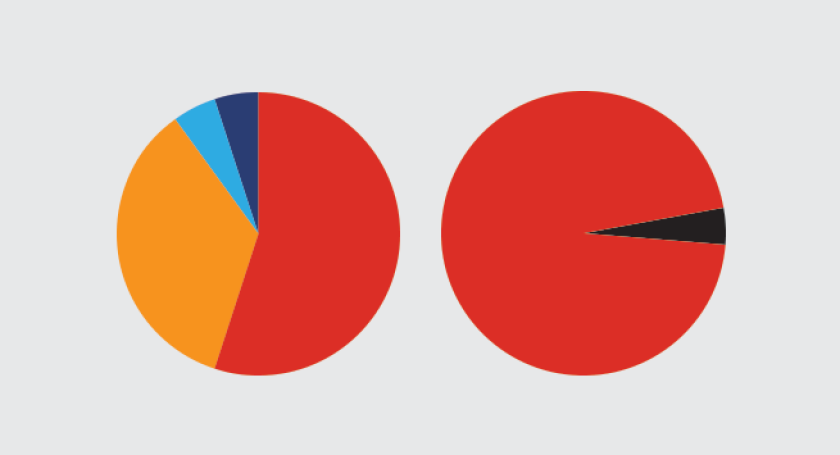

CTC is the main force for communication infrastructure construction in China, of that there is no doubt. However, CTC cannot always meet the entire requirements of the MNOs, so the independent towercos are a powerful supplement to fulfil the construction of difficult sites. For example, more than 900 site construction requirements were given to CTC’s local branches by China Mobile in 2017, representing less than 50% of their total requirements that year. By the end of 2018, more than 70% were completed by the independent towercos. This is enough to prove the importance of independent towercos.

Figure one: China’s new build by site typology

TowerXchange: How would you respond to international investor concerns that China’s MNOs still own the majority of equity in CTC – as such independent towercos’ customers own your biggest competitor – does that mean you can get an attractive, investible contract from those MNOs?

Jiatu Zheng, Secretary General, CITA:

The ownership of CTC is mainly distributed among three operators, and there is no absolute holding. The shares are owned by three operators’ headquarters. The tower construction is performed at two levels, by the provincial and municipal cities. In provinces and cities, the majority of operators welcome the independent towercos to participate in tower construction because of dissatisfaction with the local CTC (involving a series of problems such as efficiency, site deployment resolution, maintenance, and electricity fees). In addition, in cooperation with the independent towercos, operators generally can obtain a more favorable rental price than CTC. The preferential rate is generally controlled between 5-10%; it’s a win-win deal.

TowerXchange: Who owns the land under towers in China? How long is a typical land lease? What are typical margins between the cost of the land and the lease revenue generated from tenants?

Jiatu Zheng, Secretary General, CITA:

All land in China, including the land under telecom towers, is owned by the country, China. All the units and individuals only have the right to use. The typical land lease period is ten years. The typical margin is generally less than 20%.

TowerXchange: How transparent is the permitting of a new tower in China? How many different authorities are involved? How long does it typically take? Once you have a tower permitted, are there any protections against another towerco building another tower on the other side of the road?

Jiatu Zheng, Secretary General, CITA:

Generally speaking, the construction of a new tower is subject to a bidding process. The winning bidder builds eligible and qualified towers according to the requirements of the bidding document. The total cost is 200,000-500,000 RMB (US$28,300-70,800).

Municipal approval units include: Garden, City Construction, Law Enforcement Bureau, Planning Bureau, Communications Authority, Radio Committee, Industry and Information Bureau, et cetera. The construction period is typically about one month.

If a tower had been built, other units are not allowed to rebuild, according to document (NO. 92) issued by the Ministry of Industry and Information Technology (MIIT).

Figure two: CTC versus independent towerco market share in China

TowerXchange: What kind of infrastructure are China’s independent towercos deploying? What is the mix of traditional three legged macro towers, monopoles, rooftops, city poles and smart poles?

Jiatu Zheng, Secretary General, CITA:

The cell sites deployed by independent towercos include all the mentioned types. The approximate proportion of tripod towers, monopoles (“single pipe towers”), rooftops (“tower poles”), and urban poles is shown in figure one.

Basically, rooftops represent more than half the new build. Ground based towers consist mainly of monopoles (including a few camouflaged as trees). Although the concept of urban poles and smart lamp poles is very popular, it has not yet entered the large-scale deployment phase. The reason is very simple: MNOs have not yet deployed 4G and 5G extensively.

TowerXchange: Which stakeholders typically come together to deploy smart city infrastructure in China? Who owns the lampposts, and who is best placed to convert lampposts to smart poles? What role is played by local and central government, by MNOs, by building owners and by infrastructure companies like towercos?

Jiatu Zheng, Secretary General, CITA:

At present, the government, operators, CTC, independent towercos, and some social enterprises all want to be involved in the smart city infrastructure construction to share the 5G cake.

Currently, the lamp poles in urban areas are typically owned by the street lamp bureau under the government. However, CTC and independent towercos are the most suitable entities for turning lamp poles into smart tower poles. The current business model of telecom tower leasing is most mature and operates at the largest scale.

Local and central governments mainly play the role of parents to promote the construction of smart lamp poles. The MNOs drive demand and also represent the largest financing source. The original lamp pole ownership remains with building owners and street lamp bureaus. Tower companies can be financial contributors to the reconstruction. They integrate the power and resources of each party, reconstruct the lamp poles according to the requirements of MNOs, and lease them to MNOs, to complete the whole business chain.

Figure three: the fragmented structure of the Chinese independent towerco market

TowerXchange: How many towers would you estimate China’s independent towercos own in total today?

Jiatu Zheng, Secretary General, CITA:

The number of towers owned by independent towercos in China is about 80,000 today. With the concept of co-build, co-sharing, the number of new towers is decreasing every year, but tenancy ratios increase continuously.

TowerXchange: We would like to understand the structure of the independent tower market in China. How many independent towercos are there with more than 1,000 towers and who are they? Roughly how many independent towercos are there with 100,1,000 towers?

Jiatu Zheng, Secretary General, CITA:

Independent towercos with more than 1,000 towers include the following companies:

- Guodong Group

- Beijing Miteno Infrastructure Investment Co., Ltd.

- Jilin Sunho Communication co. Ltd.

- Bright Financial Leasing Co., Ltd.

- Beijing GuoLian ZhengTong Communication Technology Co., Ltd.

- Beijing Netstone Information Technology Co., Ltd.

- Zhejiang Longpiao finance leasing Co., Ltd.

About 100 independent tower companies have 100-1,000 towers in China.

These small companies build towers based on their own capital. They have localised social relations and construction capabilities, but their funds are generally limited. Because most are cashflow funded, the advantage is that there is no need to pay high interest, the disadvantage is that they lack capital to expand. Therefore, on the one hand, they have built towers to collect rent, on the other hand, they have limited opportunity for further development. This is the concrete manifestation of China’s typical farming culture: self-sufficiency model. A small number of companies either have a listed company background (such as Miteno), or have a close relationship with banks or foreign capital providers (such as Zhejiang Longpiao). These few companies are expected to become the outstanding models of Chinese independent towercos in the next three to five years through their own organic growth, and through mergers and acquisitions.

TowerXchange: Are independent towers being bought and sold in China? Can we learn any valuation benchmarks from those transactions, or are they too diverse?

Jiatu Zheng, Secretary General, CITA:

There is no problem with the free trade between independent tower companies in China. The MNOs can also support this.

Currently, two valuation methods are available in the market. One is construction cost plus profit premium valuation; the other is the revenue valuation method, that is, based on the ten year contract amount, the transaction price is valued at three to six years’ revenue.

TowerXchange: How are China’s independent towercos financed today?

Jiatu Zheng, Secretary General, CITA:

Currently, there are three financing modes: First, a loan secured against collateral of existing assets from a bank; second, listed companies secure capital market financing; third is the finance leasing model or private lending. In general, financing costs are relatively high and difficult.

TowerXchange: Why do some independent towercos in China want to secure international investment? What do they want the money for? Why can’t capital be raised locally in China – for example, how expensive is bank debt in China?

Jiatu Zheng, Secretary General, CITA:

In China, it is recognised that private enterprises obtaining bank loans is difficult. As mentioned above, the financing cost of listed companies are relatively lower, the other two methods are relatively high, generally between 8-15%. However the cost of international investment can be reduced to 3-8%, thus all independent tower companies want international investment.

TowerXchange: Does government want to encourage international investment in independent towercos in China?

Jiatu Zheng, Secretary General, CITA:

Of course, China is strengthening the efforts of opening up to the outside world, and telecommunications infrastructure is also benefit from the government’s policy. Foreign capital is welcomed here.

TowerXchange: Are there restrictions on foreign direct investment in Chinese towercos – for example, could an international investor acquire a controlling 51% stake? Could they acquire 100%?

Jiatu Zheng, Secretary General, CITA:

As CTC is a state-owned company, it completed an IPO in Hong Kong in 2018. Direct investment in CTC is not a good opportunity. Honestly speaking, you can barely get the chance. For independent towercos, the country has no special regulations. Recently a policy change also liberalised the restriction against 51% holdings.

TowerXchange: What are the potential exit strategies for an investor in a Chinese independent towerco? IPO? Sale to CTC?

Jiatu Zheng, Secretary General, CITA:

China’s independent tower company’s investor exit strategy is mainly selling to peers, that is, mergers and acquires among one another, and this pattern will increase over the next two or three years. The reason is that the IPO threshold is too high: many of China’s independent towercos can not reach the level required to IPO.

CTC has not made any acquisitions of independent tower companies nor their assets for the time being. This is because CTC’s management team is worried that to do so might lead to a business pattern which will affect their own construction ability, wherein independent towercos are seen as site builders, CTC as buyer.

TowerXchange: What are the typical contract structures of Chinese towercos? For example, what is the typical term (duration) of the contract? How would you characterise the longevity and security of tower cash flow in China?

Jiatu Zheng, Secretary General, CITA:

China’s tower enterprises, including CTC, basically use the contract template and settlement mode signed between CTC and the three operators.

The typical contract period is ten years, although a few are for five years. The typical terms and conditions are adjusted according to the price system of the CTC. The price of independent towercos increases or reduces with CTC’s. At present, the general construction cost of static investment recovery period is three to five years, dynamic investment recovery will often be four to seven years. Although the period is relatively long, there are no worries with the overall payback because the three major operators are large state-owned enterprises, the credit is backed by the country, and China has been increasing its efforts to clear debts since 2018.

TowerXchange: Can you share typical EBITDA margins of China’s towercos?

Jiatu Zheng, Secretary General, CITA:

In China, the tower companies are undertaking strict maintenance and assurance performance indicators, with higher financing costs than international peers. Therefore, in China, the EBITDA profit margin of tower enterprises is not as good, usually between 6-15%.