Marc Ganzi needs no introduction in this journal. The serial digital infrastructure investor and operator recently announced that his Digital Colony venture had not only reached agreement to acquire Zayo, and their 130,000 route miles of fibre in North America and Europe, for US$14.3bn, but also closed its first fund, Digital Colony Partners, with more than US$4.05bn in commitments. Alan Burkitt-Gray, Editor-at-large of Capacity, a sister publication of TowerXchange, recently caught up with Marc who generously shared his provocative and exciting vision of digital infrastructure.

Capacity: Please describe the relationship between Digital Bridge, Digital Colony and Digital Colony Partners, and the core thesis you share.

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

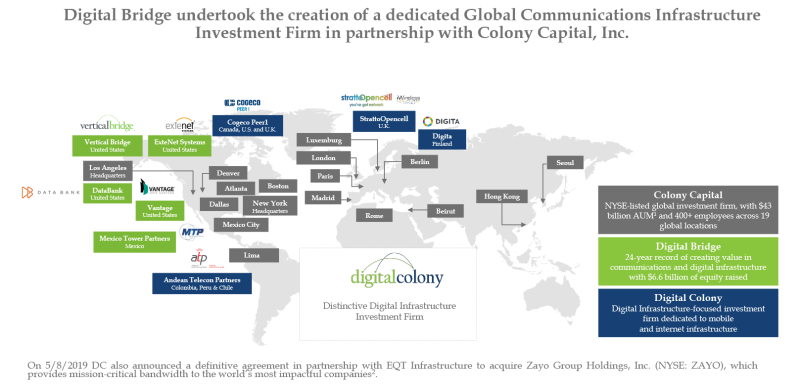

Digital Bridge was started in 2013 with the mindset towards investing in digital infrastructure, and was founded by myself and Ben Jenkins. The primary objective was to put our personal capital to work behind management teams, ideas and platforms that we really felt represented the best opportunity for investing in the future of digital infrastructure on a go-forward basis. At Digital Bridge, we raised capital as we identified each opportunity rather than investing from a dedicated fund, which can be extremely difficult, and we primarily focused on North and Latin America. We are coming up on the sixth anniversary of Digital Bridge, and I believe we have established ourselves as the leading global investor, owner, manager and operator of digital infrastructure.

Last year, we launched Digital Colony, as a way to invest in digital infrastructure on a more global scale. It’s a joint venture between ourselves and Colony Capital, which is a multi-decade highly experienced global real-estate investor, and they understand the importance and relevance of digital infrastructure as a subsector of the real-estate industry.

As far as this relates to Digital Colony Partners, this is Digital Colony’s inaugural fund, as well as my own first time launching a formal SEC fund. At the end of the day digital infrastructure is probably more parts real estate than technology. This fund brings together our three-decade track record, their four-decade track record, and really puts the best athletes on the field together with a value proposition that is appealing to investors and good for the long-term growth plans of our customers. The early returns look good, and we are thankful that the fundraising process was very successful.

The Digital Bridge core thesis and ideas resonate through all the investments we make through Digital Colony Partners. Through Digital Bridge Holdings and Digital Colony, we are managing nine different investments globally, and we feel reasonably good about our place in the world as an investment manager. Moreover, as an active day-to-day manager of these assets, on a global scale, we feel like our operating expertise is second to none.

Capacity: Please explain why it’s more real estate than technology?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

If you look at digital infrastructure, and you see the sort of things that are required to build these types of assets, you really get a good feeling for many concepts that are resident in real estate assets today. When you think about data centres and towers and fibre networks, they require entitlements, they require a real property interest, whether that’s owning the land, whether that’s an easement, or a long-term lease. All of these assets require heavy real-estate concepts, because you need a long-term duration to place this mission-critical infrastructure. Remember, when you place infrastructure, it’s on land. Fibre’s underground, you need an easement; a data centre is sitting on land, you need to own the acreage, or you need a long-term lease; a cell phone tower sits on a parcel of real estate and you own that land or you have a lease.

Underpinning the security of these cashflows for the investors are completely ingrained in real-estate principles. And the difference between being a good operator and a bad operator is your ability to understand those nuances – how to ingrain yourself into those communities, get the entitlements, have the right agreements, make sure you’re fully compliant with local municipal, county, state and federal regulations – there are so many different jurisdictions that relate to building real estate. You have to understand those principles very carefully. The folks that are really good are the ones that build the best locations – and the folks that aren’t very good at that end up running into trouble.

That’s the underpinning. The base layer of this business is heavily engrained in real-estate principles, and when you start layering up, and you think about the execution – that’s where the technology comes in. You have to understand engineering, you have to understand structural engineering, you have to understand wind loading, you have to understand power density. There’s a variety of engineering concepts in telecommunications infrastructure that are very intricate and very complicated.

A provider and owner of this infrastructure has to really live up to one key standard: the ability to make sure the facility is always running, and that the service of that asset is uninterrupted. This is where you start moving into telecom, which is, can you and do you, as an owner-operator of this very unique real estate class, have the ability to operate at five-nines standard? Our facilities are only as good as the two tenths of a second they fall down. We are very focused on that, we are very focused on ensuring that our customers have uninterrupted service, and that whether it’s a fibre connection, a data centre connection or a tower connection, even a small-cell connection. These are the things that matter and the things our customers judge us on. They judge us not only on our ability to build the facility and to provide the facility, but they also want to make sure it’s going to run well, in an uninterrupted fashion.

The strategic moat in this business is pretty simple – you have the real-estate entitlements which are very difficult, and on the other side of the fence you have the technological, operational part of the business, which is also quite difficult. Once you combine the two unique skill forces, the real estate and the telecom operations, you can imagine it’s hard. Not many people can do this, especially on a global basis.

Capacity: What are the selection criteria?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

Infrastructure assets are not all created equal. When infrastructure investors come into our sector, and raise these big funds and they say they’re interested in digital infrastructure, they often don’t realize these aren’t like toll roads, shipping ports, or water treatment facilities. You can’t paint digital infrastructure with a broad paintbrush. In fact, I would argue it’s incredibly surgical painting and it’s very intricate. And the intricacies are first embedded in what I call the asset test – ensuring we have a great location and a great facility that’s been engineered to accommodate multiple users – that’s the key – multi-tenanted, multi-use facility so we can grow cash flow.

The third part of the asset test goes back to that collateral piece - making sure you have good fee, you’ve got the right entitlements, making sure you’ve got all the permits necessary for the assets. These things are essential.

And last but not least is counterparty credit risk. We spend an inordinate amount of time here looking at the quality of our customers, reviewing their balance sheet, reviewing their P&L, reviewing their business plan, their value proposition to their customers. Are they investment grade or are they non-investment grade? The most important thing is: What is the paper you have with that customer? Do you have a lease? Do you have a licence? Is it bankruptcy protected? Do you have early termination provisions? Do you allow the customer to grow in the space without remunerating us? There are so many nuances in these master lease agreements and master licence agreements that the different between a tower being worth eight times cash flow and being worth 25 times cash flow is directly correlated to the quality of the paper.

When we say the quality of the paper, we mean the quality of the agreements between you and the counterparties. These are the details we’ve learned over 26 years of business. We’ve negotiated over 40,000 leases across the globe – in the data centre, fibre, tower and small cell space. Having that purview of 40,000 agreements certainly affords you a lot of battle scars.

We’ve done a lot of learning since we got started, so what I can say is we’ve been thoughtful, we’ve taken our time and we’ve curated contracts with folks with our counterparties, and with our customers that can endure the test of time. Guess what: the relationship endures the test of time. If you read a bad piece of paper that doesn’t align your interest to your new customer, it inevitably leads to friction, and what I would call that landlord-tenant tension.

We’ve prided ourselves in building fair lease agreements with our customers that get them what they want to achieve in terms of their tenancy and allowing them to grow their technology, but at the same time respecting that we’ve taken the risk in building the facility, and that we’re going to be rewarded for that risk. And that’s really the key to the final aspect of the asset test – counterparty credit risk and the quality of the contract you have with the customer. These are the details that matter.

The second part is the business plan – once you’ve appropriately screened the quality of the asset – is that you have to have a fundamentally solid business plan. You’ve got to have good market demand for the asset, you’ve got to have high quality management lined up, you have to understand back-office systems, you have to understand how to finance the asset class correctly. And then you have to have a plan to afford the asset and how to organically build the cash flow. If all of those characteristics are resident, you’ll do quite well. If you don’t have those things covered up and understood, these investments typically don’t perform well.

Capacity: Do you ever start investments from a green field site, a project, or is it finding and acquiring assets that are already there?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

Our bias is to find the best management teams first. That’s key. People create alpha, the assets don’t create the alpha. You could have the best data centre in the world but if it has no thought leadership, it’s an empty building with a bunch of cooling. We try to find the best athletes - the men and women who can help us guide the asset to a place where customers are going to want to be there, and most importantly they’re going to stay. And they’re going to grow with us. You can’t do that without people.

Once you find the right people, then you can create the right platform. People create platforms, platforms don’t create people. We first focus on the human capital aspects of this digital infrastructure investing

Once you find the right people, then you can create the right platform. People create platforms, platforms don’t create people. We first focus on the human capital aspects of this digital infrastructure investing. Once we have the platform, we can pivot to buying assets or we can build assets. But you’ve got to have the solid foundation of the platform before you can make a capital allocation decision, which is around building versus buying.

Oure view on building versus buying is they’re not mutually exclusive. Why? That asset test applies – we have the same underlying principles. When we start buying assets at 20%, 30%, 50%, 100% higher than replacement cost, you stop buying and you start building – it’s the old adage in real estate. We take a hard-line real-estate approach to buying versus building, and we’re constantly looking at where M&A prices are, versus building a new asset.

For more than 25 years we’ve been building these assets. We’ve built some of the largest data centres in the world, we’ve built some of the largest fibre networks in the world, and we’ve certainly built towers all across the globe. So we’re not afraid to build. And we have great customer relationships that allow us to afford us that privilege to build for them. It is a fundamentally classic real-estate buy versus build decision, and we’re constantly monitoring what it would take to buy versus what it would cost to build a brand-new facility.

Capacity: You retain the original brands of your acquisitions - the different companies from the outside look as though they’re separate entities…

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

That’s good. It looks as though our design is translating well to the external world. It’s by intention. The idea is we want to partner with great people, and we want our management teams to have their own identity. At the same time, we have our own expression round here: Stay in your swim lane. By being disciplined and staying in lanes, it allows those companies to be a category killer in their own right. For example, StrattoOpencell, in the UK is super-focused on providing small-cell connectivity for MNOs and property owners in the UK. It doesn’t sell enterprise fibre. It doesn’t fill data centres. It’s laser-focused on addressing a problem in the UK, which is horrific indoor coverage and spotty outdoor densification coverage. And so, by being super-disciplined and super-focused, it’s gone from being a company that didn’t exist a few years ago to being the largest small-cell provider in the UK. And that was by design, not by accident.

That’s where discipline and focus come into play. We want to make sure our companies do operate independently but realize they have the full-facing credit of the Digital Bridge team. We provide advisory services, help on the balance sheet, we help on M&A, we help on IT systems, we help on recruiting and HR. We provide a litany of services to our portfolio companies. But at the end of the day, what is bedrock for us is a focus on finding a great management team, ensuring they can make the best decisions, and arming them with capital, people and processes to be successful.

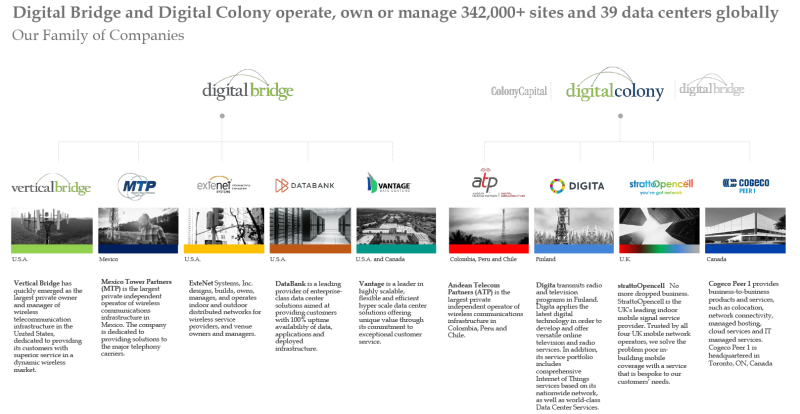

There are situations where our portfolio companies do get together and collaborate. And we’re constantly encouraging collaboration between the companies. For example, we have amazing collaboration between ExteNet and Vertical Bridge. Why? Vertical Bridge is the largest private tower owner and operator, ExteNet is the largest private small-cell operator in the US. They call on the same carriers all the time so it wouldn’t surprise you that sometimes they go on carrier calls together. It’s an opportunity to provide a holistic solution for a customer. Another example: Vertical Bridge owns thousands of acres of real estate, much of it in dense urban areas, and DataBank is doing edge computing. They are working together to create an edge data centre product. They are rolling out small data centres in large urban areas where we have a lot of power, we’ve got a building, we have a ton of fibre. DataBank has the customer relationships and Vertical Bridge has the underlying real estate or the entitlement. So it’s a great way we can take something that was not necessarily a core asset at Vertical Bridge, and overlay the DataBank edge computing strategy and you get a force multiplier.

We encourage that collaboration: Vantage and DataBank work together – DataBank does core colocation, one megawatt and below. If you take a look at what Vantage is doing, it’s one megawatt and above. Each of them very specifically understands their swim lane and when a customer wants to downsize Vantage can pass that off to DataBank, and when a DataBank customer wants to upsize and go one megawatt plus, they can hand that customer off to Vantage, and it really makes sense. It ensures none of our customers – whether they’re in artificial intelligence, IoT or content, cloud computing, medical storage, government agencies, enterprise users, whoever it is – has the infrastructure they need. We want to make sure that fish doesn’t swim through that net. We want to catch everything in the net and that there’s always a place for us to support a customer in their digital infrastructure needs.

Capacity: To what extent are your sales and marketing efforts integrated across entities?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

The top executives at Digital Bridge are constantly sitting with customers. It’s in our DNA because we’re operators. We’re not ivory tower guys and girls. Our staff and team here have been operating networks for decades. The thing we enjoy the most is we love sitting with customers – it’s great to sit with our customers because they can give us feedback on our portfolio companies. They can tell us what’s coming down the road. We’re not operating as an infrastructure business at the Digital Bridge level, so those conversations can be incredibly open and transparent. We’re not there trying to pitch them something. We’re really there to listen and to say “Listen, we’ve got this ecosystem, $16 billion of assets globally, we’ve got all these sites, all these people, these resources. How do we best support you?”. It’s also “What are you seeing? Where’s Google going, where’s Amazon going, where’s Microsoft going, where’s Verizon going, where’s Vodafone going?”

Our customers realize that these conversations help us support them. Our primary reason for existing is to support our customers, and we’ve never lost that focus. As an investment manager, it’s easy to get lost in trying to raise more money and manage more assets under management or chase fees – that’s not Digital Bridge. Digital Bridge is focused on the question “how do we support these multi-decade customer relationships as they embark on building arguably the most complicated networks in the world?” And when you think about the intensity that’s required to build 5G, it’s a lot more sophisticated than other wireless networks. We need to be active listeners. We need to have this dialogue around the world with customers trying to figure out how to support them.

Capacity: Do these acquisitions come to you, or do you have an acquisition team that hunts the globe?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

We have a team that executes these ideas globally. Our headquarters are in Boca Raton, Florida, and we have an office in London and New York City. We’ve got people that are looking at assets in Europe, North America, Latin America, that’s really our purview at the moment. However, we’ll also look at Asia and Africa. We look at everything. We try to be thoughtful when opportunities come along.

how do we support these multi-decade customer relationships as they embark on building arguably the most complicated networks in the world?

This is really a sign of things to come because the world is adopting technology so fast. Across the planet there are nine billion connected devices. That’s only going to grow. When you think about the total number of connected devices, and you think about the future and what’s coming, we’re going to have 25 billion devices connected to the internet of everything. That’s huge. You’ve got roughly four billion mobile internet users across the globe, and we’re going a add another billion over the next six years. This is massive growth.

Capacity: Do you set different criteria in terms of growth and profitability across Digital Colony’s asset classes?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

We have this disciplined framework where we look at each asset on its own two feet. That gives us an added advantage compared with other investment managers.

The first criterion you have to look at is risk tolerance and for digital infrastructure, there is a spectrum that from left to right is lower-risk to higher-risk. On the far left you have assets that are incredibly safe, and the safest assets are typically hyperscale data centres, towers, and sub-oceanic cables – usually governed by very long-term contracts with customers that cannot terminate, and once they sign an agreement, they typically stick anywhere from ten years to 35 years.

And then in the middle of the road you find three different kinds of assets that have a medium risk: small cell networks, wholesale fibre, and colocation data centres. These are contracts that are typically five to 15 years and have a little more volatility.

As we migrate to the far right, we see businesses that have high risk – managed services, hybrid cloud computing, applications, spectrum and enterprise fibre. These are extremely volatile because they have no contract duration – like spectrum – or a one or two-year contract. It’s characterised by high churn, as much as 1% per month if the business is unstable. You have to be rewarded for that risk. You get higher returns, but you have much higher alpha in terms of the risk tolerance, and much shorter-term duration of contract.

What’s really fun about what we get to do is, we walk in the door every day and we get to make these asset allocation decisions on behalf of our investors. We’re building a balanced portfolio, which is currently operating in Europe, Latin America and the US. What we see is that the returns in the US are the most stable, followed by Europe, and third would be Latin America, which has its fair share of volatility. If we want to chase higher returns, we invest in that part of the world. If we want to go for the safest returns, we stay here in the U.S. If we want to chase alpha somewhere in the middle, we chase Europe. This is the portfolio construction. You’ve got the geography of being in Europe, Latin America, the U.S., and then we have these different asset classes – enterprise fibre all the way up to hyperscale data centres and towers – and we play all parts in between. The hope is you create and construct a balanced portfolio that measures the right type of risk, the right type of reward and supports the right type of customer with the right credit profile.

Capacity: Where are you going into as investor, either announced or not yet announced?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

We’re spending our time on all three continents. There a lot of opportunities happening in all of the subsectors – there’s new sub-oceanic cabling systems being built, new towers being built. We’ve had an upsurge in core colocation, in rack space. The notion of hybrid cloud is very interesting because corporate users want to turn a certain part of their applications over to the cloud yet they want to keep storage and their own systems to themselves. They’re not quite comfortable putting all of that in the cloud. Most IT directors are making a fair and balanced approach to how they manage their IT loads. The major benefactor of that is somebody like a DataBank, which has a hybrid cloud solution and offers disaster recovery and colocation. That’s been a nice, pleasant surprise this year.

I would say another pleasant surprise has been tower leasing. We’re starting to see 5G amendments, as the carriers think about long-term network architecture, and our tower businesses in the Nordics, Mexico and the U.S. are all experiencing an uptick in leasing. That’s great.

As much as small cells and densification and cloud computing and hyperscale are all going strong, we revert back to where we started, which is owning a good tower asset or owning a good data centre as the best way to achieve organic growth.

Capacity: How did you pick the telecoms industry when you started?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

As it relates to digital infrastructure, I don’t think anybody went to college for it. When I went to college back in the 1990s, my ambition was to be in finance and real estate. My background was doing real-estate acquisitions and financing. When I got my first job out of college I was working at a REIT, doing M&A work and buying distressed real estate.

Somehow in 1993 we had a couple of these things called “antenna leases” for some of our buildings. Because I was the young kid from Wharton, everyone thought that I knew something about technology and that I was smart. The leases dropped on my desk. I started negotiating these leases with something called cellular telephone companies – and they wanted to sign these 30-year leases with us. As a real-estate investment trust we had a tenant that was begging us to sign a 30-year lease. You can’t imagine how excited everyone got at the company that somebody wanted to sign a 30-year lease for space that was deemed a liability, the roof, collecting rain! When people started paying us thousands of dollars for rooftop space, a light went off in my head – clearly more people were going to call us about this stuff.

In 1994, I met up with two guys who had also gone to Wharton who had started a cellular telephone company – they educated me about everything about cellular networks and how the FCC has these auctions and so on. Cell phones were coming, and it was going to go to digital. There was just going to be this massive surge in real estate. The three of us got together – I understood real estate, they understood cellular communications, and we put these skills together. With a common interest in helping carriers identify and lease their real estate for digital networks. That was my journey. It was completely accidental. Like all great things in life.

What’s great is those two guys are my partners today – Alex Gellman is co-founder and CEO of Vertical Bridge and Jeff Ginsberg is the COO at Digital Bridge, and the three of us have been together for 25 years.

Capacity: Anything you can say on the record about Zayo?

Marc Ganzi, Co-Founder & CEO of Digital Bridge, and Managing Partner at Digital Colony:

No, unfortunately I can’t.