I have struggled to write about India for quite some time as every week, news emerges that will complicate the already tangled web of events affecting the local telecom tower market. But as I look closer, the Indian landscape is finally approaching re-definition, with only a few decisions remaining before the market achieves a “new normal”. Here is an overview of where Indian MNOs and towercos stand.

In the latest chapter of the never-ending Indian saga, Brookfield Asset Management and Reliance Industries have finally reached an agreement under which the Canadian fund will invest INR252bn (US$3.7bn) in the units proposed to be issued by Reliance Industries’ Tower Infrastructure Trust. Said trust holds 51% of Reliance Jio Infratel, the infrastructure entity recently created to own and operate Reliance Jio’s tower assets.

With the move, Reliance Industries looks at deleveraging Jio Infocomm and Jio Infratel’s balance sheets (as well as its own) and at professionalising the latter as an independent tower business.

The agreement has been signed by Reliance Industrial Investments and Holdings, a subsidiary of Reliance Industries, and BIF IV Jarvis India, affiliated with Brookfield and the deal is currently subject to final due diligence and regulatory approval.

Jio: a varied and growing portfolio

Jio Infratel is still developing its 175,000-tower portfolio, which was valued at around US$5.4bn when carved out. Once completed, the towerco will run the largest pan-Indian portfolio ahead of the combined Indus Towers and Bharti Infratel, with 163,000 sites.

Even before the transfer of assets to the towerco, Jio embarked into an impressive build-out effort. Jio co-located on around 30,000 of 43,263 sites previously owned and later acquired from Reliance Communications, with the rest organically built. Jio Infratel has announced plans to grow its portfolio to 260,000 sites in the near future (although that figure is believed to include co-location on third party sites).

While Jio’s growth trajectory has been impressive, it’s also been noted that around 40,000 sites that Jio deployed so far are single-tenant lampposts not immediately apt for co-location. This urban portfolio is in prime locations and still enjoys Jio as tenant but the valuation for these assets surely takes into consideration their inability to host multiple tenants.

Indian MNOs still struggling

The Indian telecom landscape is hardly a stable one, with mobile network operators struggling to find the balance between staggering data demand growth and ARPUs that have been declining for years now.

Since the entrance of Jio in early 2016 (soft launched in 2015), with its aggressive price strategy and competitive data offers, the MNO landscape has completely reshaped. Aircel and Reliance Communications both went bankrupt, Vodafone and Idea Cellular merged, Tata Docomo merged with Bharti Airtel and the latter also took over Telenor India. The MNO scenario changed even further, with the acquisition of Hutch by Vodafone, prior to the latter merging with Idea, the merger of Virgin Mobile with Tata DoCoMo, the merger of MTS India with Reliance Communications prior to its bankruptcy and the exit of Videocon, who ceased to operate following its spectrum sale to Airtel.

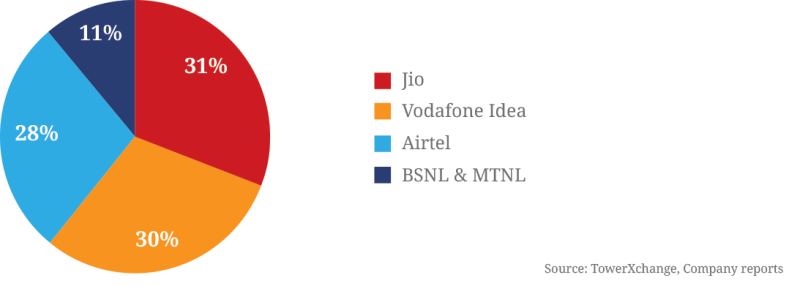

To date, the MNO landscape sees Jio leading the market with a 31% market share, Vodafone Idea following closely with over 30% share, Airtel at 28% and State-owned BSNL and MTNL at just over 11%. Jio has surpassed Vodafone Idea as market leader this past June, in part thanks to the strategy adopted by Vodafone Idea to set a minimum recharge plan with the goal to eliminate low-revenue users. The plan caused the MNO to lose 67.2mn subscribers since December and triggered an associated increase in ARPU, and in the latest earnings’ call, Vodafone Idea CEO Balesh Sharma backed the plan and said the company is “confident of improving churn as well as ARPU.”

The stock market didn’t see the move as positive, with Vodafone Idea’s share dropping over 26% following the earnings’ call and analysts are now reassessing their estimates following a mildly optimistic view of the market based on Bharti Airtel’s stable Q4 figures.

While Vodafone Idea struggles to sustain its new plan, the two State-owned entities BSNL and MTNL have been under severe financial stress for years now, unable to fight back against brutal price competition.

BSNL has doubled its losses since last year to over US$200mn and MTNL has reported losses of around US$50mn. Both operators have been suffering due to shrinking revenues over the past few quarters and are dealing with extremely high employee costs (BSNL has 166,000 employees and MTNL 21,679) which mean poor revenue-to-wage ratio. In fact, while the average percentage of an MNO’s income devoted to employees varies between 3 and 5% for private operators, that percentage hikes to over 75% for BSNL and 87% for MTNL. In a nutshell, it would not be surprising if further changes occur to the Indian MNO landscape and one of the potential outcomes could be the sale or carve-out of assets, including around 75,000 towers, of the two State-owned MNOs, with both options having been discussed for years now.

On a positive note, BSNL and MTNL are both actively sharing their towers with other MNOs, with Jio as their main tenant, having rented 8,307 sites from BSNL and 137 from MTNL.

Bharti Airtel has enjoyed a positive last quarter with Bank of America Merrill Lynch upgrading the stock to buy and raising the target price following the MNO’s move to increase its tariffs and the IPO of its Africa unit, which has strengthened the operator’s global position.

India’s tower ownership - Q219

Is Indian infrastructure a good bet?

Bank of America Merrill Lynch’s analyst Sachin Salgaonkar was recently cited by the Economic Times of India stating that “Despite muted near term growth prospects of the tower industry, we expect 900mn 4G users on an average consuming 12Gb of data” and that most of the data demand will be met using “towers rather than by small cells or in-building solutions.”

In an MNO landscape dominated by a price war, towercos are likely to be in charge of building the majority of towers for the MNOs who hardly have capital and time to invest in their own infrastructure rollout. But the demand for new builds isn’t likely to even out the effects that the MNOs turmoil has had on tenancies. In fact, tenancy churn has hit all major entities Indus Towers, Bharti Infratel and American Tower in 2018 and is continuing to do so in 2019.

The merger between Vodafone and Idea Cellular generated more than 57,000 tenancy losses but further churn is expected in 2019 and 2020 (over 20,000), which will be only partially offset by exit penalties, as recently noted by S&P’s Indian research firm Crisil.

The tenancy crisis is one of the reasons why Indus Towers and Bharti Infratel have decided to join forces, with the merger expected to complete before the end of Q319. The process has already received all permissions and is pending only the Department of Telecommunications’ approval for enhancement of foreign direct investment limit, as pointed out in a recent analyst call by Bharti Infratel’s Chairman Akhil Gupta.

So the new shape of the Indian telecom and tower landscape is made of three solid MNOs, namely Jio, Vodafone Idea and Bharti Airtel, with the fourth State-owned entity still in trouble, and three strong towercos, Jio Infratel, Indus-Bharti and American Tower as well as an array of smaller towercos, many of which are likely to look for a buyer.

In fact, the towerco scenario beside the top three entities is still turbulent. GTL Infrastructure for example, with its 28,000 sites, has reported three years of losses (amounting to a total of 71%). Its revenue has dropped 36% since last year.

Brookfield will get involved in the ownership of Jio Infratel, whose assets see Jio Infocomm as anchor tenant. And this can only be good news since the MNO has been reporting strong financial gains in the last quarter and more than 50% growth in subscribers from last year, having added 116mn users in the past year.

Indian MNOs market share - Q219

Canadian funds keen to invest in India

Canadian fund Brookfield has been active in India for a decade now, having already invested over US$10bn across multiple sectors – energy, commercial real estate and now, telecom infrastructure. And it’s only one of a few Canadian funds involved in India, including CDPQ, CPPIB and PSP Investments.

The drivers behind investing in telecom infrastructure are well known to many but the attractiveness of India might be less obvious. However, India has been a hotspot for Canadian funds for a few years now and they have good levels of experience and expertise in infrastructure investments.

While investing in Indian towers is not for the faint-hearted, the country presents strong yield and growth opportunities matched with the attractiveness of scale, which aren’t easy to combine in telecom towers. With the current MNO consolidation and associated tenancy churn, it may be a good time to “buy low” in Indian towers. As previously mentioned, the Indian telecom market is experiencing a stellar growth curve of data consumption, which Ericsson’s latest Mobility Report predicted will reach 18Gb per month per subscriber by the end of 2024, having reached 9.8Gb at the end of 2018.

Once again, one of the major breakthroughs in the Indian data market was caused by Jio and its generous data plans, which pushed users to finally use mobiles for video streaming and other data-heavy functions. While 5G is not imminent in India, 4G densification and overlay will keep pushing MNOs to stretch their financials and towercos can only benefit from this growth tailwind.

Last but not least, Brookfield has been eyeing deals in Indian towers for at least three years. In 2017, it got very close to acquiring 45,000 towers from Reliance Communications in a US$1.6bn deal – towers which then got absorbed by Jio – and in 2016, it was reportedly in talks to take over a majority stake in Bharti Infratel. Over the past three years, Brookfield not only negotiated large deals with other key players across India but got a real-life chance at understanding what it means to do business in the country.

While a venture in India is far from a walk in the park, TowerXchange is confident about Brookfield’s ability to positively partner with Reliance Jio Infratel and turn the towerco into a force to be reckoned with in the local infrastructure ecosystem.