An audience survey at the 5th TowerXchange Meetup Asia proved again that Myanmar is the most attractive investible tower market in Asia, narrowly edging out Indonesia, India and China. In the last five years, the Myanmar telecom industry has evolved from a single stated-owned operator that monopolised an underdeveloped market, to a competitive and diverse landscape, where four operators and dozens of independent towercos are driving infrastructure deployment, generating the highest organic growth rate, and already one of the highest tenancy ratios in the region.

Telecommunications in Myanmar has come a long way and the government has played an instrumental role in pushing the industry forward. Key institutional reforms, the implementation of a modern telecom law and a transparent licensing process for both operators and tower companies has created a very favourable regime for local and international MNOs, infrastructure developers and investors. The country was again one of the most popular topics at the fifth TowerXchange Meetup Asia, where several panels, roundtable discussions and speakers analysed and highlighted the great opportunities that Myanmar holds.

The evolution of Myanmar’s regulatory regime

We were honoured to welcome Mr. Soe Naing, Director at the Post and Telecommunications Department (Ministry of Transport & Communications, Myanmar), who spoke at the event for the first time. Mr Naing provided an eloquent regulatory overview, which dissected how the government has boosted infrastructure deployment and tower sharing with its forward-thinking approach and policies.

Back in 2010, a few political reforms were the initial steps for the liberalisation of the country’s telecommunication industry. Then, in 2012, a foreign investment law eliminated several restrictions and paved the way for international companies to enter Myanmar. A Telecommunications Act in the following year, Telenor and Ooredoo’s licenses in 2014, and the creation of an independent regulatory body in 2015 were also critical steps ahead of the birth of a competitive and healthy tower market.

In 2013, Myanmar had one operator, less than 7mn phone users and 7,600 km of fibre. Now, the country has more than 52 mn phone subscribers and 68,000km of fibre with an internet penetration of 90%. Liberalisation has seen teledensity increase from 13% to 102.6% today. The reforms have improved internet speed (24 Mbps, second only to Singapore in the region), quality and overall coverage.

Stakeholders have recognised the importance of tower companies as Myanmar has licensed over 40 towercos who have built almost 10,000 towers in less than five years. The regulatory framework has encouraged tower sharing and colocations, has enforced zoning regulation to protect existing towers, and PTD projects tenancy ratios, already around two, to reach 2.5 by 2020. US dollar rents, with inflation related escalators applicable to 100% of rent, and non-cencellable contracts have all contributed to the creation of a highly investible tower industry in Myanmar.

Furthermore, the government has been working closely with the Central Bank and Myanmar Investment Commission, which has enable the entrance of international investors such as TPG. Now, the Ministry of Transportation and Communication has set very ambitious goals but the industry is still facing several challenges that will require more reform, considerable investment and collaboration across the telecom ecosystem.

What lies ahead?

Mr. Soe Naing perfectly summarised the future objectives for the industry. The government is already preparing new spectrum allocation to enable 5G deployment, while aiming to establish a fully independent regulator—the Myanmar Telecom Commission. Additionally, the once state-owned operator MPT needs to finalise its corporatisation process, while the telecoms industry has to increase its community engagement in order to continue expanding.

The goals are set but this dynamic market brings plenty of challenges for tower providers, MNOs and vendors. Power continues to be a key issue, with 65% of the towers in remote, off-grid locations, where communities can be reluctant and infrastructure deployment can be logistically challenging. Data consumption keeps increasing exponentially and 5G will push the industry to look beyond traditional towers and explore alternative technologies and solutions. The government has created a Universal Service Obligation Fund to facilitate investment in rural coverage, while significant progress has been made toward the enablement of mobile financial services and smart cities.

Industry perspectives

Right after PTD’s keynote, Myanmar’s panel discussion continued the conversation that TowerXchange started back in September, when we travelled to Yangon to explore this evolving market. Representatives from Apollo Towers, TPG, edotco, Delmec, MPC and OCK Yangon took the stage and weighed in on Mytel’s impact, key operational challenges, consolidation and more.

Hardiman Telecommunications’ Paul Carpenter set the scene. He suggested Myanmar now had 16,000 towers, 3,000 rooftops, and 25,400 tenancies, with an average tenancy ratio on towerco sites of 1.74x.

TPG, represented by David Goldstein, has been one of the most active private foreign investors in the market, and in Goldstein words, they are just getting started. The company entered the market through Apollo Towers in 2014 and consolidated its position as the second biggest tower portfolio with the recent acquisition of PAMEL: “The regulators have done a fantastic job. First, they’ve enabled foreign ownership and led a very transparent, pragmatic privatisation process that created an attractive scenario for us. Now data usage keeps increasing as users consume lots of content on their phones and this growth, plus the new operator, will keep driving the need of towers and tenancies,” Goldstein commented.

2018 has been a very positive year for towers in Myanmar and edotco has had been growing prolificly. The company has added 600 sites and added 1000 tenancies to its portfolio in the last year. They have done BTS for both Ooredoo and MPT as well as taking over the management of Ooredoo’s energy assets, including power as a fundamental change to the company’s business model in the country. Innovation is in edotco’s DNA and the company has been busy testing ground-breaking solutions such as carbon rooftop poles, and a combined solar and wind power site generating 8kW of power, as well as new builds in remote areas. edotco are also proud to have partnered with Energize the Chain, who they met at TowerXchange in 2016, to commission five sites with the Ministry of Health to aid in the distribution of vaccines.

In a similar move, Apollo Towers has also taken over management of Ooredoo’s energy equipment on their sites. The towerco has been dealing with power for other clients since they entered Myanmar and Ooredoo asked them to apply that expertise, which in the words of Apollo’s Chief Commercial and Strategy Officer Yves Monnier, is very challenging, especially due the high uptime SLAs of certain sites, that sometimes approach 100%. Monnier commented positively on the potential consolidation of power assets, as Mytel’s entrance and PAMEL’s acquisition will allow them to optimise power cost by managing all the assets with a single team.

Equally, OCK has been also working very closely with its main client Telenor in optimising energy consumption in order to reduce opex, which is a pass through model. The Malaysian tower company is increasing its utilisation of solar and wind solutions – increasing from 60-100 hybridised sites in the coming year. Renewables are reducing MNOs’ opex as well as minimising maintenance costs due reductions in genset runtime. While focusing on optimisation and energy saving, OCK has also increased its portfolio and the company is now working with all four MNOs, as mentioned by OCK’s Yangon CEO Omer Chappelart.

The demand is there, but does Myanmar have enough capacity? Delmec’s CTO, Spencer Crawford-White, who has been studying the market for the last five years, commented: “The market has massively expanded. We are seeing plenty of new infrastructure and less conditional issues but we still identify some limitations. Mostly, there is some redundant, old equipment not being removed from sites and that could have a negative impact on capacity for and speed of rollout of 5G. We are now working with OEMs on the implications and requirements of 5G. Structures are going to be heavier and bigger, so you need to plan ahead and start preparing your sites for future adoption.”

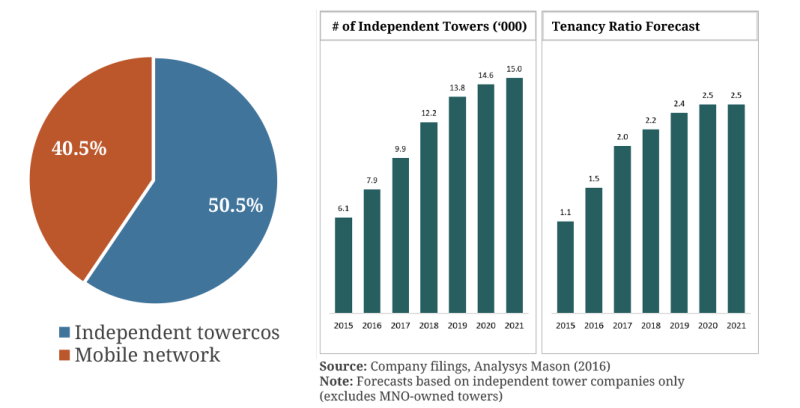

Myanmar telecom towers sector – the results so far

New entrant towercos: competitors or acquisition targets?

The emergence of a number of new, small tower companies and their potential consolidation are critical themes in Myanmar. MPC is one of those emerging players that will also play an important role in the industry. MPC’s new CEO Kieran Rabbitt came along and commented on the role they are playing in Myanmar’s tower industry: “We are playing our part and disrupting the industry in a very positive way. We obviously work with lower volumes but we can partner with established companies, while we also aim to collaborate with MNOs to cover hard-to-reach areas. We focus on opportunities that might be tough or too niche for traditional players such as remote, conflictive areas where you need to work closely with local communities,” he said. In the case of MPC, they feel they can achieve sustainable margins at a lower rate, ableit not pricing as aggressively as some competitors, and hoping to innovate and compete in urban scenarios.

What are the new entrant tower companies in eyes of the most established players? All panellist agreed that the market is big enough to support everybody’s existence – at least for now. Myanmar is a competitive, but also friendly environment with considerable growth potential. Both Mandalay and Yangon regions still face capacity issues and are in need of new sites, so there are plenty of new build opportunities ahead.

Unquestionably, the market will consolidate and big fish are very likely to absorb all many of the new small towercos in the next two to three years. edotco and Apollo are committed to Myanmar for the long-term and both companies are eyeing organic and inorganic growth opportunities: “When you merge, as we are just doing at the moment with PAMEL, you learn a lot from the other company and strengthen your team, which helps you in improving your service to customers. Colocations are indeed fundamental but we still see strong BTS opportunities here,” Monnier commented.

TPG, edotco and MPC highlighted urban solutions, IBS, street furniture and small cells as the future alternative site typologies that will fuel continued impressive organic growth. Delmer’s Spencer Crawford-White added “Smart solutions and lamp post designs are evolving to fit into urban enviornments. We’re exploring leveraging AI to identify potential locations that offer the necessary elevation, with access to power and fibre. Densification via macro sites will be prohibitively expensive in Myanmar (and beyond) – we need to work together to accelerate dimensioning, planning and deploying infill sites and co-hosted solutions like BTS hotels.”

Data will keep booming and towercos will need to explore how to better integrate new technologies and solutions to increase coverage and capacity. The industry needs to continue educating the country on the benefits of infrastructure sharing, and investing time and resources in boosting social licenses is fundamental. Power will continue to be an operational headache and the use of renewable energy will increase to help the industry in reducing diesel consumption and energy expenditures. Consolidation is guaranteed and TowerXchange forecast a bustling 2019 in Myanmar. Stay tuned!