Whilst a small market, Lebanon’s population has grown dramatically in recent years due to an influx of refugees. The state owned telecommunications sector, known for having some of the highest mobile tariffs in the world, has recently kicked off major investment in fibre, with significant tower rollout being mooted for the next couple of years. TowerXchange examine the recent developments and dynamics at play in Lebanon.

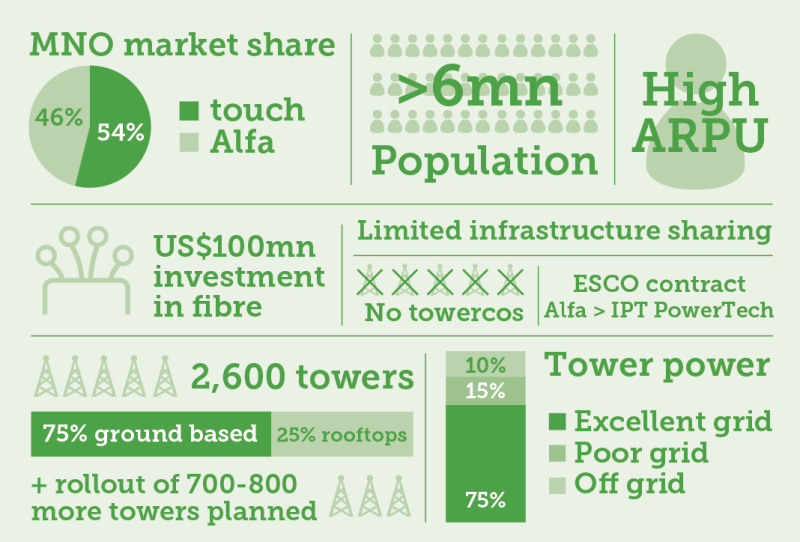

Lebanon, in Western Asia is bordered by Syria to the north and east, Israel to the south and the Mediterranean to the west. The country has a landmass of just over 10,000sq km and a population of 4.5mn which has swelled to over 6mn in recent years, primarily due to an influx of refugees from neighbouring Syria. Close to 90% of the population lives in urban areas, with the capital, Beirut, being the largest city with a population of around 2.4mn (CIA World Factbook).

Lebanon’s GDP was US$51.8bn at the end of 2017, with GDP per capita sitting at just under US$7200 (World Bank). The country scores highly on the UN’s Human Development Index and education standards and literacy rates are similarly high.

The history of Lebanon’s mobile sector

Mobile telecommunications first came to Lebanon back in 1994, when BOT contracts were awarded to two private GSM companies; Libancell and Cellis. The contracts were awarded for an initial 10-year period, after which time, the networks were scheduled to be returned to the government. The two operators were required to pay a percentage of their annual revenues to the government and obliged to charge identical tariffs for postpaid customers whilst a ceiling was set for prepaid charges. Cellis was 67% owned by Orange (then France Telecom) with the remaining shares held by Lebanese InvestCom, whilst Libancell was owned by various Lebanese investors including the Dalloul family and the Lebanese Telecommunications Company (with Finland’s Sonera having originally owned a 14% share).

In the mid-2000s, a bitter dispute ensued between the government and the mobile network operators, with the government claiming that the MNOs had not delivered the agreed proportion of revenues and had broken stipulations on the maximum number of subscribers each network was permitted. The government announced fines of US$1bn per operator and the World Bank was forced to intervene. The operators offered US$1.35bn to convert their BOT contracts into 20 year operating licenses but the government refused, subsequently cancelling the BOT contracts. The control of the networks and revenue returned to the state, with Cellis and Libancell being paid management fees to manage the networks until a new management tender was issued and contracts awarded in 2004. Zain, (formerly known as Mobile Telecommunications Company of Kuwait) assumed control of the Libancell network, operating under the brand “touch”, and a consortium led by Detecon International (part of Deutsche Telekom) took over management of the Cellis network, operating under the brand “Alfa”. Zain still retains the management contract for touch, whilst Orascom took over management of Alfa in 2009, with the management contracts having been extended regularly ever since.

The telecoms sector remains a major contributor to the country’s GDP, providing the second largest source of state revenue after taxation. The country has some of the highest mobile tariffs in the world, a fact which has led to protests from the general population. Whilst talks have occurred regarding re-privatisation of the sector, it looks unlikely that the government would want to cede ownership of the two profitable businesses.

touch and Alfa have a roughly equal market share, with touch’s Q2 2018 results reporting the operator to have a 54% share and Alfa to have a 46% market share. 3G mobile services were launched in the country in 2011, with 4G services launched in 2013

The growing fibre market

In addition to the two state owned by mobile network operators, Lebanon has a state owned, fixed line fibre operator called OGERO which owns all of the country’s fibre. A major fibre rollout plan has been recently announced to bring fibre to the cabinet, with contracts awarded to three partners for the rollout; Serta Channels in partnership with Huawei, a joint venture involving BMB Group and Calix, and IPT PowerTech in partnership with Nokia. US$100mn was approved by the Cabinet for the project in October 2017 with the overall project cost expected to total US$283mn. OGERO plans for the project to be completed in a 40-month time period, with contracts having been awarded in February 2018. Companies are required to ensure a minimum transmission speed of 50Mb/s. Three local operators - Connect, Globalcom Data Services and TriSat, have been licensed to provide FTTH broadband services using OGERO’s fibre network. OGERO will remain the sole owner of the fibre network, with the three additional operators only allowed to deploy fibre where cabling is not available (expected to be less than 5% of the overall network). Revenues from fibre are expected to contribute significantly to state coffers, alongside existing revenues from the telecoms sector.

The tower industry

There are 2,600 towers in Lebanon, evenly split between the two mobile network operators, touch and Alfa. Around 75% of sites are understood to be ground based towers with the remaining rooftops. In spite of the two operators having a common owner in the government, there is little to no infrastructure between the two players. There are currently no independent towercos operating in the country.

In order to improve coverage and capacity, plans have been laid out for each operator to add 300-400 new towers starting in 2019, an almost 30% increase in the country’s total tower stock. The budget still requires approval from the government (with both operators being state owned) and so whilst the proposals have drawn interest and excitement, observers remain cautious as to what timeframe this will be realised in.

The power situation

Of the 2,600 towers in Lebanon, 15% enjoy excellent grid with 24 hours of availability. Such sites are located on or around key government buildings and hospitals. Between 10-12% of sites are completely off-grid with the remaining 73-75% on poor grid. The definition of poor grid ranges anything from 6-18 hours, with better grid the closer the sites are to the capital city, Beirut. Whilst power availability is low in some regions, the introduction of a schedule of when power will be on or off makes for more refined management of poor-grid sites, creating less complexity than in poor-grid African countries for example.

Alfa recently signed an ESCO contract with IPT PowerTech in the country, whereby IPT PowerTech has taken over the power management across the operator’s full portfolio of sites. Speaking on the ESCO project, Khaled Habbal, COO, IPT PowerTech said

“Recognised as Leading T-ESCO globally”, with the largest number of ESCO sites worldwide, IPT Powertech Group decided to initiate the T-ESCO model in Lebanon by signing long term contracts with Alfa. We are a Telecom Energy Service Company (T-ESCO) company that invests, and provides comprehensive energy, and site infrastructure solutions and services to its customers, from auditing, to redesigning, procuring, and implementing innovative site solutions, all the way to managing networks, on a full OPEX model while guaranteeing savings and efficiencies. IPT’s T-ESCO model will serve MNOs and the Lebanese Government in a way to reflect the appetite for capex spending or capex leasing, all the way up to optimal TCO.

By introducing this model, the the Lebanese telecommunications sector will greatly benefit from IPT Powertech’s advanced expertise and knowledge gained from international experience in Africa, Middle East and South East Asia. The T-ESCO model will ensure guaranteed savings to MNOs and contribute significantly to the Lebanese government.”

Operating conditions

Whilst power remains a challenge in Lebanon, those active in the market report that operating conditions in Lebanon are relatively straight-forward. The country is compact and safe to work in, albeit with a few more challenges closer to the borders.