During the recent edition of the TowerXchange Meetup Americas, we engaged the audience through a live poll to find out what executives in the room thought about the CALA market, its future expansion and upcoming trends. Between 55 and 75 respondents voted in the poll and, given that the majority of people in the room were senior management at towercos and MNOs, the results are based on a valid and substantial sample. In this article, TowerXchange offers its readers insights into the poll results.

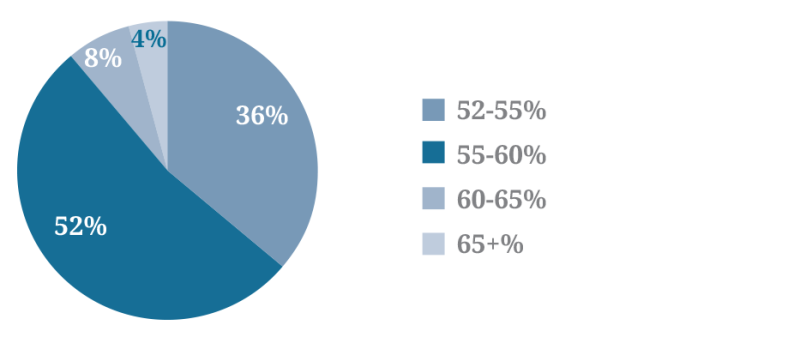

Q1 - Towercos currently own 51.9% of CALA’s towers. What proportion of the region’s towers do you think towercos will own by next year’s event?

Over 52% of the audience agreed that by June 2019 towercos will own 55-60% of CALA towers. This suggests towercos will build or buy a further 9,100-17,900 towers in the next year. If Tigo and Digicel continue to divest towers in markets such as the Caribbean and Central America (but maybe also in virgin ones such as Uruguay), this could definitely be an achievable number!

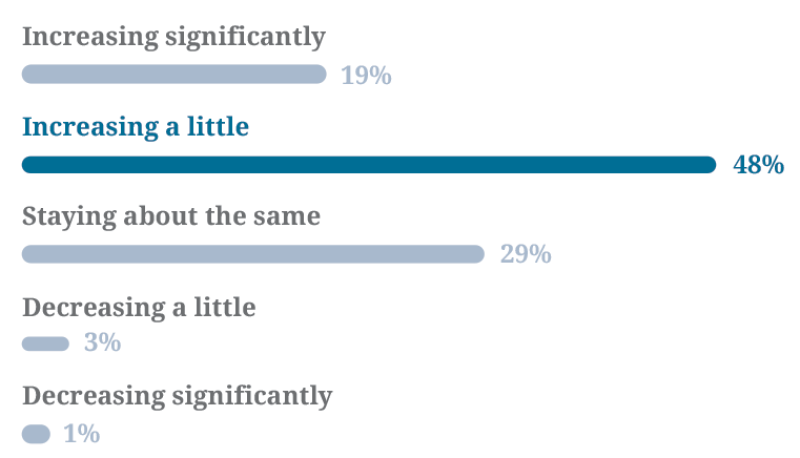

Q2 - Do you anticipate the volume of new build towers increasing, decreasing or staying about the same in the markets in which you operate?

While projections for inorganic growth are optimistic, organic growth (build-to-suit) is expected to increase just a little across the region by 48% of the voting audience. An average of 6,510 new towers have been built per year in CALA between 2015-18, and it seems our audience expects a third consecutive year of slow but steady organic growth across the region, contributing to a continuing widening infrastructure gap as data demand growth outstrips network investment. The continuing cautious pessimism about the volume of search rings forthcoming from CALA’s MNOs suggests a need to redesign the relationship between operators and towercos to ensure the needs and expectations of the two match.

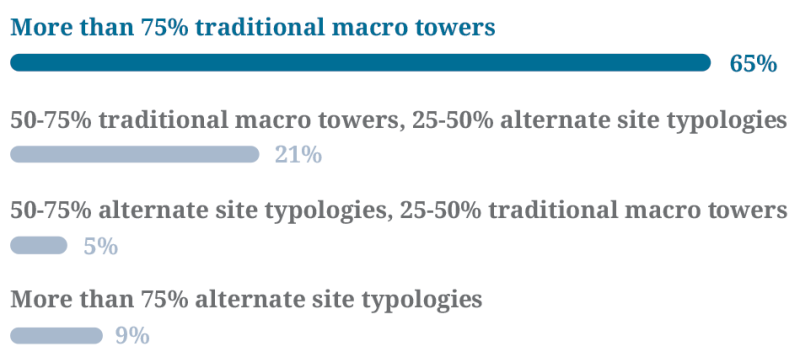

Q3 - What has been the % of macro towers versus other types of sites (e.g. urban poles, rooftops, billboards) in your new build over the last two years?

The TowerXchange Meetup Americas saw a definite increase in interest in new site typologies, alternative designs, small cells and beyond. But at the end of the day, 65% of the voters agreed that over the past two years more than 75% of the sites they built were indeed macro towers. So while there is a growing interest - and demand - for more design alternatives, the region is still in dire need of macro towers.

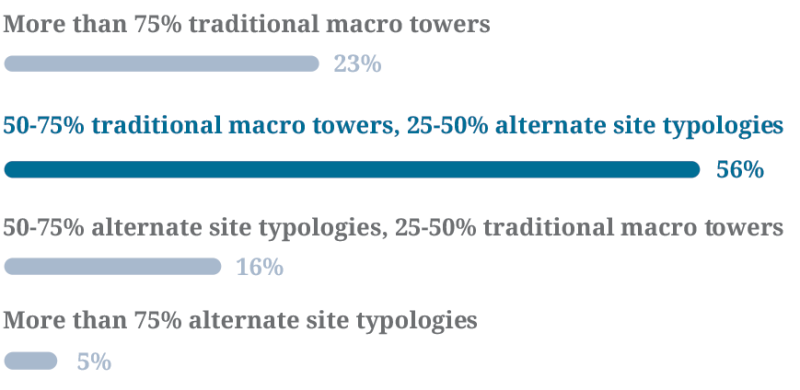

Q4 - Similar question but this time what is the % of macro towers versus other types of sites (e.g. urban poles, rooftops, billboards) you anticipate building in the next two years?

The aforementioned trend is due to change over the next couple of years according to 56% of voters. In fact, the large majority of the audience agreed that the pendulum of macro towers versus alternate site typologies will shift to, respectively, 50-75% for traditional sites and 25-50% for new types of sites. A change indicative of the growing demand for infill solutions and capacity in high density urban locations and a focus on completing 4G coverage across CALA.

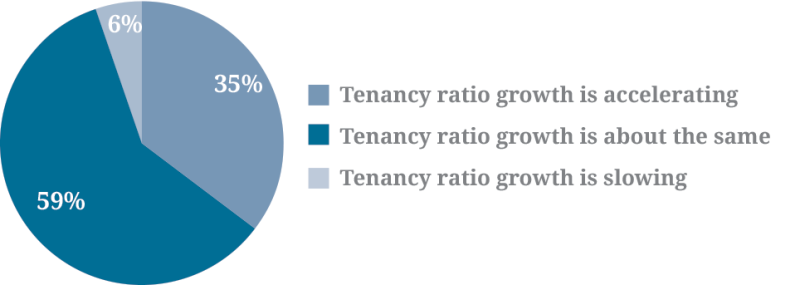

Q5 - Is tenancy ratio growth accelerating or slowing in the markets in which you operate?

59% of voters agreed that tenancy ratio isn’t really changing in the markets where they operate, perhaps indicative that the volume of new build is offsetting lease-up to keep tenancy ratios constant. However, it’s interesting to highlight that 35% are seeing tenancy ratio accelerating. A positive sign indicative of exciting dynamics across certain markets such as Mexico, the Caribbean, Central America.

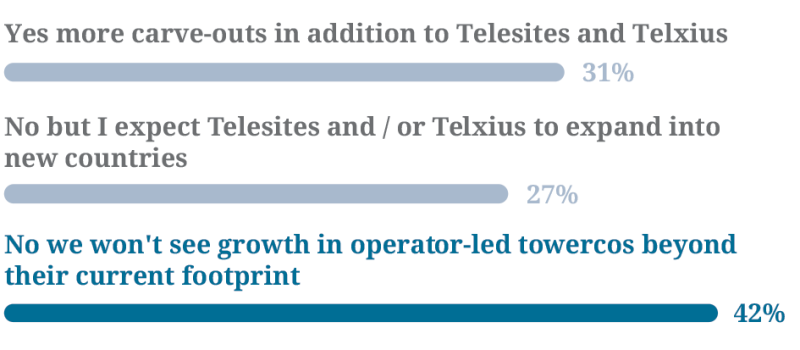

Q6 - Do you think we’ll see more operator-led carve-outs in CALA in the next year?

This question didn’t reach a strong majority possibly also due to the fact that operator-led towercos are still an unpredictable type of entities. In fact, while 42% of voters don’t think that Telesites and Telxius will expand beyond their current footprint, 27% expect exactly the opposite. And while I am uncertain with regards to Telxius’ next move and actually inclined to think that they will focus more on their cable division rather than on expanding their tower portfolio’s footprint. Telesites still has the potential and capability to go beyond Mexico and Costa Rica and expand across multiple CALA markets.

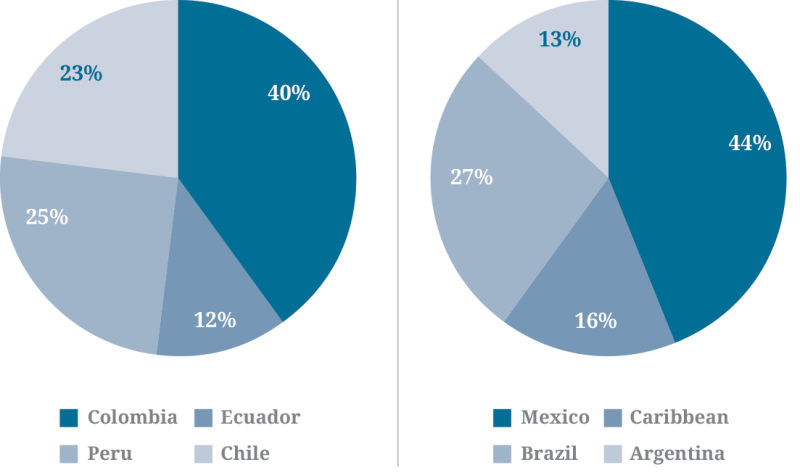

Q7 - If you had US$500mn to invest in any CALA market today, where would you invest it?

Results of this question were slightly skewed as we asked which were the most investible tower market in each of two groups. Mexico and Colombia came out winners with the majority of voters opting to invest in them, followed by Brazil, Peru and Chile. Mexico is experiencing an exciting phase thanks to ALTÁN Redes and its aggressive rollout targets while Colombia is re-emerging as a stronger and more rational after a few years of instability caused by a high volume of new entrants offering disruptive terms. So it comes as no surprise that these two markets are judged as highly investible by the audience. Additionally, both the Mexican and Colombian peso have considerably dropped in value; a factor that represents a further driver for U.S. investors eyeing opportunities in CALA.

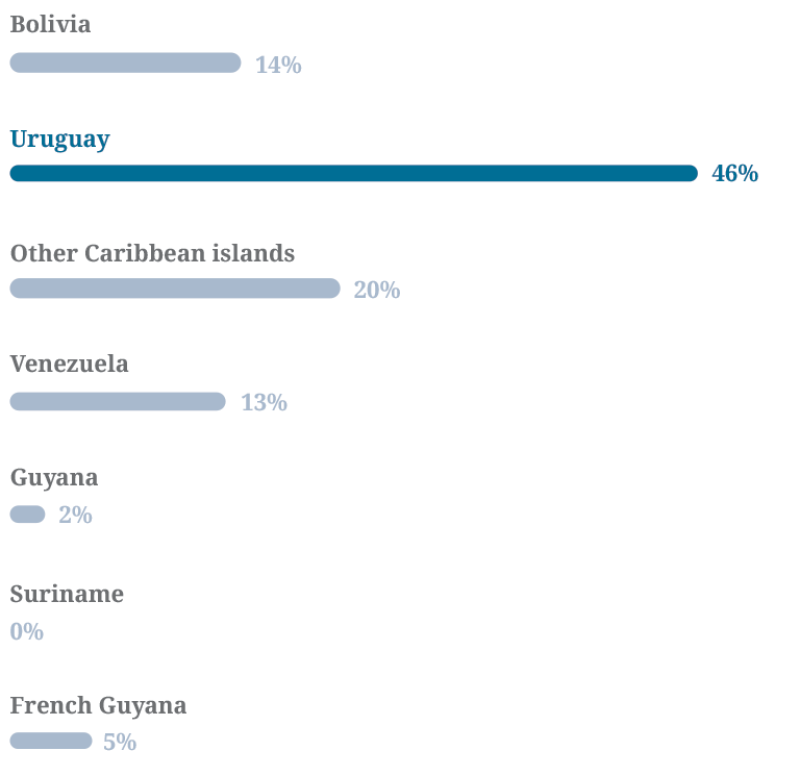

Q8 - Which virgin tower market do you anticipate opening up next?

A strong portion of voters (46%) agreed that Uruguay will be the next CALA market to open up to towercos. The country is home to three MNOs (State-owned Antel, Movistar and Claro).

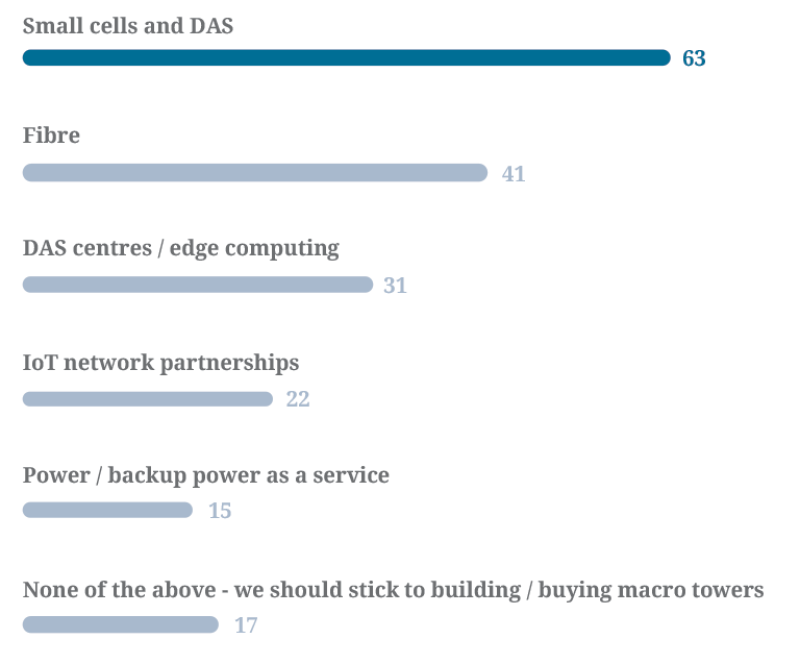

Q9 - Which segments do you think makes more sense for towercos to get involved in in CALA?

Shifting from towers to additional products and services, we allowed voters to multiple answers and small cells and DAS scored the highest with 63 votes. And while this comes as no surprise, it is interesting to note that fibre achieved 41 votes and data centres 31, hinting at the fact that some players are definitely looking beyond their comfort zone and assessing opportunities that we thought were far from the scope of towercos just a couple of years back!

Please note: in the below bar below the numbers refer to votes and not percentage

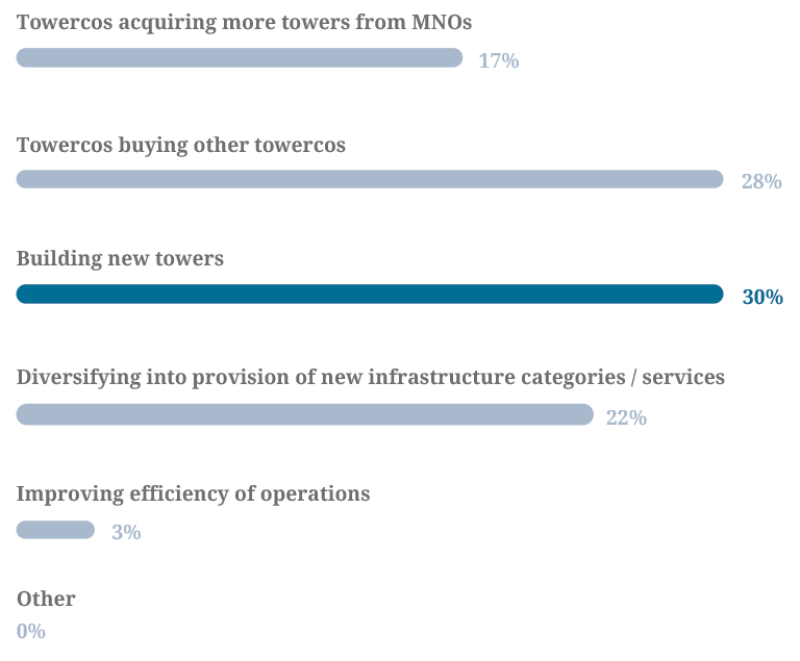

Q10 - What is the greatest opportunity in CALA towers in the coming year?

This question brought us back to the core of the tower industry and reminded us that the strongest revenue stream and growth factor for towercos is still building new towers, followed closely by consolidation. The CALA tower industry is quickly changing, but the bulk of its opportunities, at least for the year to come, are still expected to be in “pure towers”.

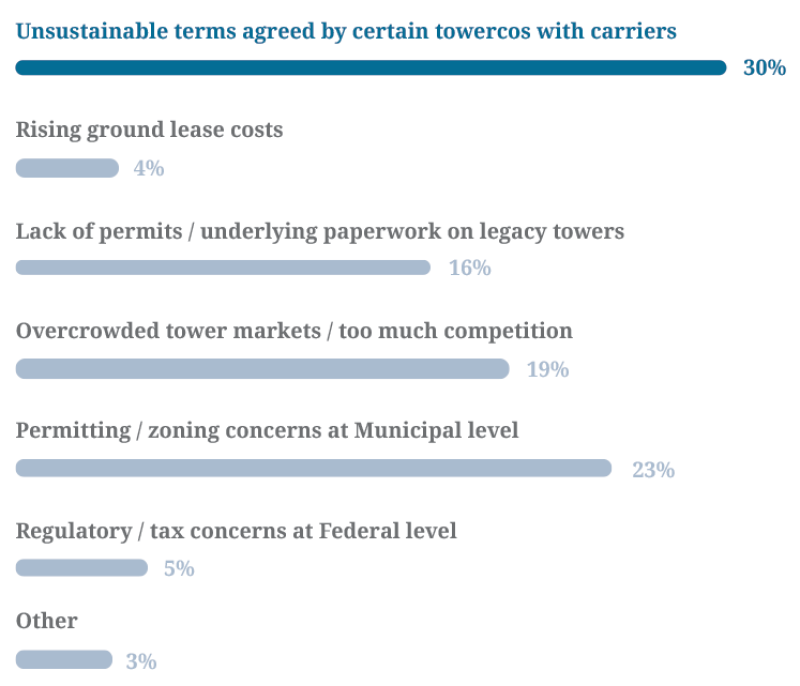

Q11 - What are the greatest threats to the CALA tower market and its growth?

This was a controversial question that delivered fragmented results. In fact, while the behaviour of some towercos who have set a precedent for irrational contractual terms and are putting at risk the solidity of the entire sector is the most voted threatening factor in CALA, a couple of other aspects follow closely. Among them, the tough permitting regime and the overcrowded towerco landscape of certain countries.

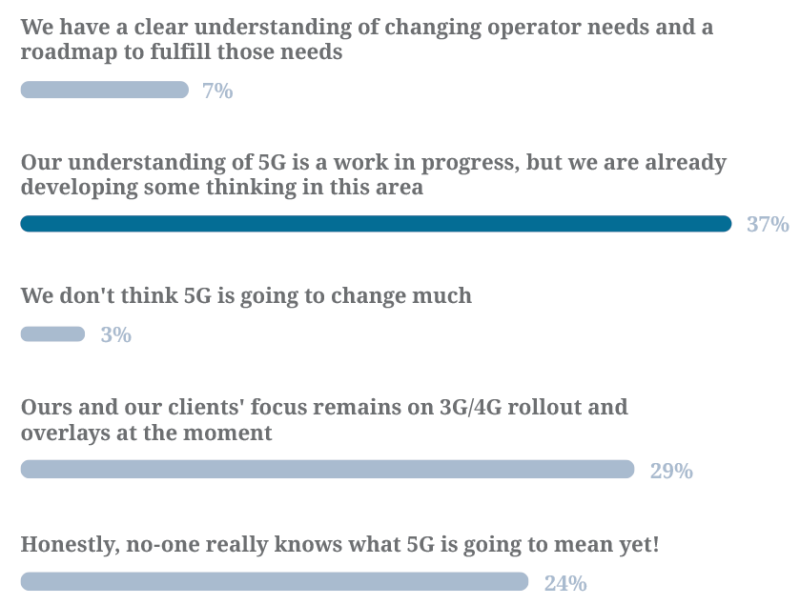

Q12 - Which of the following statements most closely represents the readiness of the CALA tower industry for 5G?

Lastly, we asked the audience about 5G and their understanding of what it means for the industry. Just as we thought, while many voters agreed that 5G is a work in progress or - even more candidly - a yet-to-be-grasped change, 29% of them agreed that the focus across CALA is still very much on 4G and even on 3G. This is hardly a surprise in a region where 4G is still being deployed and barely achieving 40% penetration across many markets.

Conclusion

TowerXchange launched its live polls to get even closer to its readers and live events’ audience. Our understanding of the CALA tower ecosystem has improved enormously over the past four years and we believe that the region has still much to offer in terms of growth, consolidation and opportunities for new markets to open up.

The CALA market has proven a fertile market for investment with those able to build sustainable tower businesses but to date, it’s also becoming a test-bed for opportunities beyond towers and this could be particularly appealing to the large pool of independent developers looking at reinforcing their competitive edge.

While adjacent segments of the infrastructure world such as fibre and data centres are starting to offer more immediate opportunities for diversification, towercos remain focused on their core business of building and buying towers. And for now, macro towers are driving the majority of growth although this is set to change in the near future, with the need for infill solutions becoming a more crucial necessity in urban areas.

Overall, CALA is a highly investible region and home to some virgin markets that could become towerco-friendly in the near future. TowerXchange cannot wait to see what’s next!

A thank you to everyone to engaged and participated in the live poll. See you next year for the sixth edition of the TowerXchange Meetup Americas, taking place in Boca Raton, 9-10 July 2019.

Download the PDF of the TowerXchange Meetup Americas 2018 poll results