China is home to the world’s largest towerco China Tower Corporation (CTC), as well as a fragmented but substantial ecosystem of 200+ independent towercos. CTC’s much anticipated IPO on the Hong Kong Stock Exchange has been delayed to 2018 (Q2 or Q3) from its original target of 2017 year-end, with a goal to raise US$10bn. Meanwhile, independent towercos have continued to grow organically, with plans for acquisitions, expanded business models, domestic IPOs and international footprint.

Market context

What are the number of 4G customers in China?

As of February 2018, China Mobile reported 661.83mn 4G customers, while China Unicom had 187.13mn 4G subscribers, and China Telecom indicated 193.33mn 4G “terminal users.”

How many new towers were built in China in 2016?

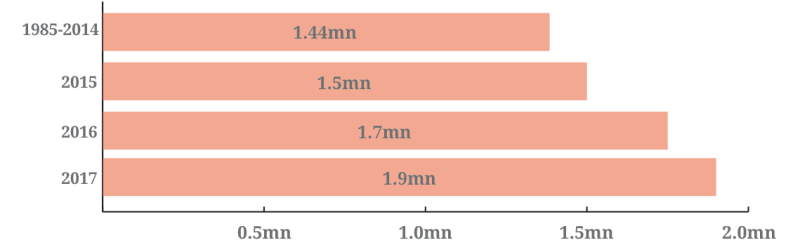

For context, prior to CTC, there were approximately 1.38mn towers built by the three operators over 30 years between 1985 to 2014.

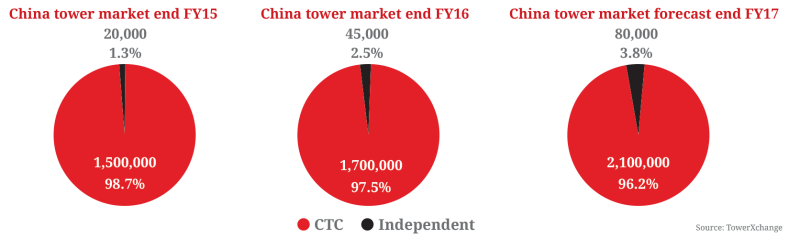

It was reported that asset transfers of roughly 1.5mn towers happened around the end of 2015 and beginning of 2016.

By September 2016, CTC was quoting roughly 1.63mn towers, and by year end around 1.7mn towers.

Overall, CTC build volume for 2017 is ~200,000 towers. In terms of independent towerco output for

the time period, estimates would be in the range of 20,000 to 30,000.

How many towers are in China and who owns them?

China Tower Corporation owns ~1.9mn towers as of 2017 year-end.

The 200+ third-party towercos will own approximately 40-50,000 towers. Guodong Networks (headquartered in Shanghai) has the largest cross-country portfolio, with presence in virtually all provinces now and an estimated tower count of 15,500 for 2017E. Beijing-based Miteno is the second largest independent towerco, with an estimated 6,000 towers in its portfolio for the same time period. There are a further handful of towercos who own assets in the 1,000 to 2,000 range, including Sino Netstone, Hangzhou Wanxing, Jilin Shenghao and Beijing RLZY.

It should be noted that the definition of a tower in China is inclusive of monopoles, rooftop structures and lamppost sites.

What is the future growth of in Chinese towers?

CTC still has a lot of building to do, including plans to provide coverage on the 56 subway lines and 59 of the high-speed train lines within the next three years.

CTC has also developed strategic partnerships with 22 provinces and autonomous regions to better integrate network planning and construction into local planning, as many are keen to drive economic development through enhanced mobile and broadband coverage. Reportedly the new arrangements have been better compared to what operators were dealing with in the past. This theoretically paves the way for faster and more build out.

There is some speculation that within three year’s time tower construction could slow down in China. The standards for 5G are yet to be defined and many commentators have indicated that 4G is more than enough for the general mobile consumer. Generally 5G would mean higher site density and smaller equipment mounted at lower heights.

On the independent side, one source estimates that there could still be 50,000 to 100,000 towers available to build given the size of the country.

The need for macro towers will decrease over time as major coverage projects get completed. Ultimately, tower growth will be dependent upon the operators’ demands.

Major cities will need more infill sites to provide the density needed for heavy data need. More light-pole integrated tower designs that are sleeker, smaller, and faster to deploy will likely play a role, as well as microcell and small cell.

Approximate tower ownership in China by operator 2014E

What is the vision behind creating China Tower Corporation?

With the approval of the General Office of the State Council and led by State-owned Assets Supervision and Administration Commission of the State Council (SASAC) and the Ministry of Industry and Information Technology (MIIT), the joint venture was formed to promote a culture of infrastructure sharing in China. Also referred to as “co-build, co-share.”

CTC was formally created on 15 July, 2014 to consolidate and share existing towers, to construct shared additional towers, and to save land and tower resources.

In 2015 alone, compared to MNOs own build, CTC was able to realise savings of 265,000 sites, 13,000 acres of land and CNY ¥50bn of investment.

One of the goals of CTC is to improve the customer experience from, in some cases, a few hundred KB per second, to as much as 20MB per second once 4G is fully deployed.

CTC is also seen as a mechanism for reducing the gap between competing MNOs by providing China Unicom and China Telecom with access to China Mobile’s vast tower network, enabling them to accelerate and catch up their 4G rollout. If 4G coverage were complete, using VoLTE could enable refarming of valuable spectrum.

The formation of CTC not only allows China to accelerate 4G rollout, but also enable the implementation of the country’s mobile broadband network strategy.

The creation of CTC is also a reform of sorts, to drive efficiency and inject new energy into the industry.

Opportunities to diversify CTC into other shared infrastructure, and the sheer scale of the business, means the vision is less to create the world’s largest and most valuable towerco, but to create one of the world’s largest and most valuable infrastructure companies.

China Tower Corporation tower counts by year

Does CTC also own assets beyond the macro network, such as rooftops, IBS, DAS and transmission infrastructure?

CTC has absorbed most, if not all, China’s legacy towers, monopoles, and rooftops. There is an appreciation at CTC that the co-construction and sharing model can extend beyond towers to transmission infrastructure, but that does not seem to have been incorporated yet.

China Tower Corporation coverage of subway and high speed lines

IBS are widely deployed in China, but there are not many DAS.

We did hear of one towerco with a substantial streetlamp project in one of China’s major cities – they called them “information poles” and spoke of how they were supporting the Smart City vision.

Does China Tower Corporation only own and lease up the towers, or do they undertake O&M too?

CTC is responsible for the construction, operation, and maintenance of towers. Having said this, given engineering design, construction, and the likes are also included as service categories on the online procurement platform, it would be reasonable to expect a certain level of sub-contracting of O&M.

TowerXchange’s calculation of CTC revenue per tower from each MNO in 2016

Who are the principal stakeholders in China Tower Corporation – who are they answerable to?

China Mobile is the largest stakeholder of CTC at 38%, while China Unicom and China Telecom own 28.1% and 27.9% respectively. China Reform Corporation, likened to a sovereign wealth fund with a particular focus on reforming State-owned Enterprises, owns the remaining 6%.

While the Ministry of Industry and Information Technology (MIIT) defines policy, CTC is effectively answerable to SASAC, the State-owned Assets Supervision and Administration Commission.

Shareholders in China Tower Company

What is the governance structure of CTC?

There are currently nine members total on the board.

Mr. Liu Aili is the Chairman of the board. He is also the Executive Director and Vice President of China Mobile, principally in charge of planning and construction, network operation, and business support.

Mr. Tong Jilu is the General Manager of CTC and the only board member formally employed within the organisation.

We’ve been able to identify one other board member Sun Kanmin who is an executive with China Telecom. CTC does not wish to disclose the identities of the rest of its board members at this time.

This governance structure is unlike the past, where more company members would also be part of the board, and was created specifically to avoid inefficiency and abuse of power.

What is the organisational structure of CTC?

There are 15 business units/departments within CTC, including management, construction and maintenance, finance, human resources, business partnerships, operations and development, audit, telecommunications technology research institute, information technology research institute, and more. There are three levels of CTC management: Headquarters in Beijing, provincial branches, and city/municipal offices. In total, there are 377 branch offices across the country.

China Tower Corporation helps MNOs accelerate 4G rollout

4G base stations in 2016

How is the financial performance of CTC?

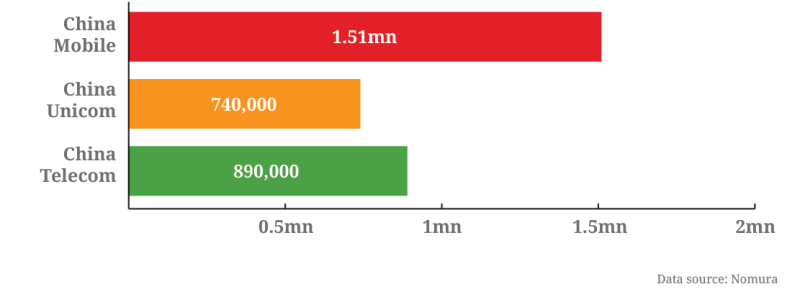

China Mobile’s networking leasing costs to CTC for 2016 was CNY¥28.1bn, with 1.11mn towers rented, while China Unicom paid CNY¥19.5bn to access 690,000 towers, and China Telecom spent CNY¥14.0bn for the rental of 610,000 towers, according to a Nomura March 2017 report.

CTC chairman and general manager Liu Aili also reported CTC breaking even last year, with a net profit of CNY¥80mn. Goldman Sachs noted CTC becoming profitable in Q42016, with EBITDA at 59%. Moving forward, CTC is expected to enjoy operating leverage from tenancy ratio growth as the three MNOs continue to rapidly deploy their 4G networks.

How and what does CTC buy?

The Tower Online Platform officially launched in the summer of 2015, one year after the creation of CTC. As of 5 September, 2016, there are 723 suppliers officially registered in the system, with 74% having been shortlisted and 58% having successfully received purchase orders; spending also reached CNY ¥26bn.

The platform was created to increase supply chain transparency and efficiency, allowing CTC staff to see who made a purchase, from which manufacturer, at what costs, plus comments and ratings on product quality, delivery, service, et cetera.

It hosts 27 major supplier and five service categories, including the likes of tower, air conditioning, shelter, battery, iDAS, engineering design, construction, and more.

Suppliers can register on the platform for free, as long as they hold a valid manufacturing license in China (for product providers), are registered with the State Administration for Industry and Commerce of the People’s Republic of China (SAIC), and pass a third-party audit.

A lot of smaller players are not on the platform for one reason or another, but instead work through those that are and act as sub-contractors; this type of partnership arrangement could provide a point of access into CTC as well for international vendors.

For further details, please refer to our article “What and how China Tower Corporate buys.”

CTC balance sheet comparison

Does CTC have some kind of right of first refusal to build new towers for the three State-owned MNOs?

Some sources told us that all build to suit (BTS) processes were supposed to be open. Other sources told us that the official structure of the Chinese tower market is that the MNOs are no longer building their own towers, and all the work is being undertaken by CTC. While MNO builds have more or less halted, the reality is that CTC currently lacks the capacity to meet 100% of MNO demand, which in a practical sense means in some cases third parties are contracted to build sites which are then are transferred to CTC’s balance sheet.

In other instances it seems that the independent towerco steps in as a fallback option if CTC lacks the capacity, or gets too bogged down in process, to meet MNO demands on time. “China’s private tower companies are often more energised and faster to market,” said one interviewee.

In other instances it seems the independent towercos simply undercut CTC, as a function of lower management costs. On still other occasions it seems that independent tower companies might have better local site hunters, and are able to leverage relationships with MNO network planners at provincial or municipality level to secure direct orders.

“CTC has a scale advantage from the legacy towers, but no significant advantage when competing for new BTS contracts,” said one interviewee.

“In some provinces the carriers are more open to new entrants as they don’t feel it’s in their interests to have a monopolistic towerco, whereas in other provinces CTC are more entrenched,” said another interviewee.

A Right of First Refusal type arrangement isn’t necessarily the primary risk to the independent sector’s organic growth potential. Rather it’s the relationships and economics that may affect a towerco’s ability to survive and thrive. Towercos with good connections to local government and/or operators will continue to secure projects and tenants. From there it’s having the cash flow to maintain day-to-day operations and financing to continue building. New builds are now subject to the lease rate benchmarks set out by CTC, resulting in a more challenging environment compared to the past.

Is it easy to get a new tower built?

While China’s citizens once welcomed towers and coverage, radiophobia and NIMBYism (not in my back yard) now exist in China. To combat the former, CTC has relied on a more concerted and integrated effort from the government, operators, and media to propagate educational messaging around radiation, comparing tower emissions to common household appliances. One supplier has also mentioned having to move fast in getting a tower up and/or disguising the tower as some other unrelated light pole or billboard. Towercos who have good local government relations can often circumvent the issue also, as they are building with their approval and support.

In general though the environment in China is conducive and favourable to tower building: there is a mature steel and metal processing industry; the grid is reliable and stable so downtime is insignificant, reducing opex; and the vendor network is strong having supplied 1mn+ base stations already. Fibre is also used for backhaul so there is seldom need to accommodate microwave dishes.

What is the mix of GBTs versus rooftops in China, and how has CTC affected tower design?

CTC has standardised tower designs, reportedly from 1,000 down to 155 (each design at different heights would represent one). CTC also made an effort to introduce designs of different aesthetics, functions, and heights to suit various environments. For example, the “Urban Flower” sits at 25m, can be integrated with lighting for the city and incorporate CTC’s logo and branding. It also has a 40m tower suited for stadiums, large public spaces, et cetera, that can be a landmark structure with LED lights at the top. There is also a more simple and sleek multi-purpose tower meant to be integrated with street lighting, sensors, data, and analysis.

Around two thirds of China’s sites are GBTs (Ground Based Towers – mostly monopoles), the other third are rooftops.

Approximately how many of China’s towers are currently shared? What are the tenancy ratios?

Prior to the establishment of CTC, tower sharing was around 20% in the country. By the end of 2016, total tower sharing reached 40%, with the new towers at 70% based on stats shared by CTC chairman and general manager, Liu Aili. In some regions, tower sharing amongst the three operators were supposedly as high as 91%, and at 100% along high speed and subway lines.

One local media reported 68.1% sharing rate for all sites completed in 2016 by CTC, with a tenancy ratio of 1.39 across the portfolio by the end of the year.

In an exclusive interview with the People’s Post and Telegraph (?????) in August 2017, Liu Aili noted tower sharing has rapidly increased from 14.3% to 73% over the three years of CTC’s existence. More specifically, sharing between new builds for China Mobile, China Telecom and China Unicom have grown from 3.6% to 48.6%, 36.6% to 90.1%, and 20.9% to 92.4% respectively.

What is the typical capital outlay for a new tower in China?

Of course much depends on the nature of the structure, but the average seems to be in a CNY ¥250-350,000 (US$37-51,800) range.

What would be the impact of consolidation from three to two MNOs?

Consolidation from three MNOs to two would certainly lower the glass ceiling on prospective tenancy ratios in China, and would be value destructive to both CTC and independent towercos.

While there has been rumor of MNO consolidation, the government’s current strategy appears to be to accelerate China Unicom and China Telecom’s 4G rollout by providing access to China Mobile’s towers, and in doing so start to even out the competitive imbalance.

If the creation of CTC does not have the desired effect in terms of competitive rebalancing, only then would the issue of MNO consolidation return to the agenda.

The scope of a China Unicom-China Telecom merger would likely be limited to their wireless businesses, given that a combined entity would have 80-90% share of the wireline market.

Are there any significant “non-traditional tenants” on China’s telecom towers?

The usual mix of MVNO, enterprise industrial communications equipment, traffic monitoring, first responder networks and Wi-Fi equipment are all prospective additional tenants. CTC has made repeated mentions of business diversification and innovation to include the likes of billboard ads, sensors, weather monitoring, et cetera, so the opportunities are there given the size of its network.

Is there any prospect of active infrastructure sharing in China?

The only infrastructure sharing agreement of scale in China before CTC was China Telecom and China Unicom’s deep collaboration to improve economics in low utilisation, remote areas. To date, the two operators are said to be actively sharing 600,000 4G base stations and 14,500km of fibre transmission network.

Regulation

Are China’s independent towercos licensed?

No, there is no licensing regime for towercos in China, and no immediate prospect of a licensing regime being introduced. One towerco recently confirmed this again based on notification from and communications with MIIT.

Does the Ministry of Industry and Information Technology (MIIT), regulator or “National Telecommunications Infrastructure Co-construction and Sharing Office” have the right to define the pricing of lease rates?

No. In July 2016 CTC finalised its leasing and pricing agreements with China Mobile, China Telecom, and China Unicom, which essentially set the marketplace benchmark. The formula offers discounts for co-location and covers acquired towers, newly constructed towers, indoor distribution systems, transmission products, and service products.

This has put pressure on the independent towercos who can’t charge more than what CTC is charging, especially for new towers, unless they are in highly coveted locations. All pricing on previously signed contracts are still being honoured.

So while no government body or agency per se has defined lease rates, CTC has markedly influenced industry pricing.

What is the pricing formula used by CTC?

The formula to be used for “newly-added telecommunications towers” is:

Product price = base price × (1 – co-sharing discount rate 1) + (site cost + electricity input cost) × (1 – co-sharing discount rate 2)

Base price = (standardised construction cost × (1 + impairment rate) + maintenance expense) × (1 + cost markup rate) useful lives of depreciation

It was also confirmed there is an escalator, “an inflation adjustment factor” which is common in tower agreement contracts.

What type of co-sharing discounts are available for operators through CTC?

On new towers, a 20% discount will be applied for sites shared by two lessees and a 30% discount for those shared among three lessees, with the first sole occupier (“anchor tenant”) benefitting from a further 5% discount. When it comes to site cost and electricity, a co-sharing discount of 40% will be applied for two lessees and 50% for three lessees. Again, the anchor tenant would enjoy an additional 5% discount.

For further details, please see our article “The implications of China Tower Corporation pricing.”

What is the status of rural coverage in China?

Despite the huge land area, rural coverage in China may be better even than the US; even in low population density areas of Tibet you will see coverage signs.

How are tower companies taxed?

There was no reported special tax status for tower companies in China.

China fully implemented its VAT reform on 1 May 2016 and replaced all business tax with the value-added tax (VAT).

The construction services sector’s new applicable VAT is 11% (general) and 3% (small-scale).

In terms of the sale and importation of goods, logistic services, modern services, transportation, repair and processing services, asset leasing, the standard applicable rate is 17%, and 13% for some products.

State-owned enterprises have sometimes been affording special tax treatment, enabling them to consolidate. There was no clear indication yet whether this might apply to CTC.

Is document number 586 (2014) the latest regulation governing co-construction and sharing? Is it now fully enforced?

This is the most recent document, and it has been fully implemented. But document 586 is an agreement not a regulation. It was proposed by the MIIT and agreed with China’s three MNOs to improve resource utilisation; reducing occupation of land and improving the appearance of the landscape.

A couple of excerpts from document 586 (please forgive any translation imperfections):

“From January 1, 2015, in principle, the three basic telecom carriers shall no longer build towers and other base facilities themselves, as well as IBS in subways, railways, highways, airports, railway stations and other public transportation key sites and large venues and multi-owner commercial buildings, government office buildings and other key sites.”

“The MIIT, SASAC or the province telecommunication authorities will severely punish the three basic telecom carriers, if the following behaviors were found. Basing on severity such punishment could be recommended to upper level unit to fire the related management. Such dismissed staff shall not be engaged within three years.

i. Without the approval of the provincial coordination agencies, construct towers and other ancillary facilities, as well as IBS in public transport and construction of buildings and other key areas

ii. Without the consent of the provincial coordination agencies, refuse to open sharing when the existing telecommunications infrastructure is suitable for sharing

iii. Without the approval of the provincial coordination agencies, build parallel infrastructure

iv. Independently build new infrastructure when joint construction should be carried out

v. Violation of requirement of infrastructure sharing in key areas (key areas including key public transportation sites, key buildings, scenic parks and other places identified by local communications administration, and inter-province key fiber cable construction, and the domestic extension of international transmission)

vi. Violate national standards on optical fiber “To-Home” construction

vii. Sign exclusivity agreement with the third parties in the construction of telecommunications infrastructure (including leasing)”

Clause vii. above calls attention to the fact that MNOs would appear to not have permission to sign exclusive agreements with third parties (towercos), suggesting a degree of limitation on deep build to suit partnerships.

Who owns the land under Chinese towers and on what basis is tenure granted to infrastructure firms to build towers on that land?

All land in China belongs to the government, but “Land Use Rights” can be secured for a 15-year term for industrial use, usually at a reasonable cost. As renewal fees cannot be defined up front, there is some exposure to risk of lease escalations when renewing after 15 years, but in general it was felt that escalations would be fair in a market where a State-owned Entity was dominant.

Above ground level, the telecom structures themselves belonged to China’s MNOs and now belong to CTC, or they belong to the independent towerco.

Land lease fees could also differ from region to region, project by project. One towerco mentioned not having to pay land fees in one city but paying by usage square footage in another. But this could be more the case for street/highway projects, where lighting is incorporated into the tower.

How complete is the paperwork on China’s towers?

It was widely acknowledged that not all the towers in China, whether CTC or independently owned, had a complete set of licensing, permitting and leasing paperwork. It appears to vary depending on the local government and project.

We know of one region where the towerco has a full set of papers stamped by the authorities, from meeting minutes with city planning officials outlining project requirements, to construction permit, construction plan, et cetera. This was described as “a tower’s most complete legal process and best protection.” This also means should the government for whatever reason takes down a tower, the towerco would be compensated. In this particular case, the land belongs to the government, for public use.

The permit follows, No. 40 of the Urban and Rural Planning Act, which grants construction rights.

Independent tower market

Who are the independent tower companies in China? How much market share do they have? How fast are they growing and what is the top end for their potential market share?

With the exception of four or five towercos with quadruple digit tower counts, China’s independent towerco market is highly fragmented and localised, with five to ten towercos in each of China’s 31 Provinces. There are currently 200+ towercos in China.

A lot of the independent towercos thrive on having strong local government and/or operator relations, enabling them to build quicker than State-owned CTC.

At the end of 2014, China may have had as few as 10-20 independent towercos owning ~5,000 towers. By the end of 2015, those numbers had increased to ~20,000 towers among as many as 200 towercos. Independent towercos built ~10% of China’s new towers in 2015, a proportion which bullish commentators feel could reach 30% within a year.

It is axiomatic to say, but readers must be reminded of the sheer scale of China; an independent tower sector can still thrive even with less than 2% market share. At the beginning of 2016 TowerXchange have spoken to a few bullish tower industry leaders who feel the glass ceiling on the scale of the independent tower sector in China could be as high as 20% within five years – that could represent 400,000 towers, the equivalent scale of the entire tower market in the European Union!

While there are independent towercos active in China’s largest cities, Shanghai, Beijing, Tianjin, Guangzhou and Shenzhen, perhaps the highest penetration of independent towers can be found in Provincial capitals, tier two and tier three cities in some of which TowerXchange has heard unconfirmed reports that independent towercos have a market share significantly in excess of 50%.

However, a reality check is required now that CTC is in the full swing of tower building and leasing (it’s only really been operational since 2015), and perhaps flexing its muscle a bit. There are some reports of negative consequences for MNO staff that gave contracts to independent towercos, and reports of delays in payments to towercos. But there are still opportunities for smart and strategic towercos. While major coverage projects will likely be concluded in the next three to five years and less new macro towers will be needed, difficult sites will always exist and the independents have the flexibility to get the job done.

Are there any valuation benchmarks set by towerco financing or tower sales?

One source suggested that Chinese towers with an average tenancy ratio of 1.5 were changing hands for an average of CNY ¥450-500,000 each (US$65-70,000 each). Another source put the figure at CNY ¥700,000 (US$100,000) with a tenancy ratio of 2.0. A third source suggested a 51% stake in a portfolio of several hundred towers with a tenancy ratio above 2.0 had been acquired at a valuation again of CNY ¥700,000 (US$100,000) per tower.

Guodong, which TowerXchange believe is China’s largest independent tower company, secured a CNY ¥700mn (US$100mn) investment reportedly at a high teens valuation they were very proud of.

The transfer of China Mobile, China Unicom and China Telecom’s towers to CTC reportedly yielded an average of just US$22,000 per site, significantly below replacement cost. But an asset transfer between entities all fundamentally State-owned (and owned by each other) is a poor valuation benchmark. The low acquisition cost reflects the depreciation of an inventory of ten plus year old towers, towers which were built to gain market share and with less of a view toward longevity and structural capacity, so significant improvement capex will be required. The low price point also reflects the mixed bag of assets being transferred, inclusive of everything from substantial ground based towers, a great many monopoles, rooftops, and even small Wi-Fi offload sites.

Around October 2015, China Daily had reported the transfer of CNY¥203.5bn (~US$31.5bn) worth of telecommunication tower assets, while the Wall Street Journal noted analysts valuing the venture at CNY¥214bn (~US$33.1bn). An article from the Mobile World Live cited yet another estimate at CNY¥230bn (~US$35.6bn). More specifics emerged out of a March article this year in Chinese media Caixin, which noted actual asset transfers taking place on 14 October, 2015, whereby 1.52mn towers changed hands, for a value of CNY¥231.4bn. This would translate to ~CNY¥152,000/tower or US$23,500/tower, roughly in line with TowerXchange’s previous reporting.

As part of the carve out, China Telecom (which had the least number of towers out of the three MNOs) received only equity as part of the deal (29.9%), while China Mobile and China Unicom received both equity (40% and 30.1% respectively) and a combined CNY¥91.9bn (~US$14.2bn) in cash. The Caixin article also noted that the original agreements required CTC to pay all outstanding payments and interests to China Mobile and China Unicom by the end of 2017.

To learn more, read “China Tower Corporation’s valuations from inception to future IPO” which appears later in the Journal.

Is China Tower Corporation a potential buyer of independent tower companies’ towers?

At one point CTC were believed to have made an offer to acquire Chinese towers at ~US$80,000 each. Whether that valuation is still current remains unclear, and whether such a valuation may be attractive to current owners depends on tenancy ratio, TCF, and uniqueness of location.

At this point however, multiple sources have confirmed CTC has not acquired any independent towercos or their assets.

There has been much talk of monopoly since the creation of CTC, though our sources believe the Party is keen to encourage competition, and currently CTC and the independent sector co-exist to serve the market place.

Chairman of the Board at CTC, and China Mobile executive, Liu Aili has also publicly acknowledged the presence of independent towercos. “CTC is not the exclusive provider of towers in China, there are 200+ third-party companies building and operating towers. Therefore CTC will be rejected by the market if it doesn’t deliver on low costs, good service, and competitive rental prices,” he said.

While tower acquisitions are not completely out of the picture, at this time, CTC is wholly focused on integrating assets and new builds to meet the operator’s demands and prepare itself for an IPO in 2017.

Do China’s tower companies have much appetite for International opportunities?

China’s tower sector seems largely pre-occupied with their huge and changing domestic market. However, for the handful of Chinese towercos with appetite for opportunities overseas, capital may be accessed for opportunities within the ‘One Belt, One Road’ footprint through associated investment firms such as the Silk Road Fund and the Asian Infrastructure Investment Bank.

What are typical lease rates and terms in China?

Lease rates are a complicated formula based on height and weight of equipment, desirability of location et cetera. At the beginning of year, most interviewees agreed that a range of CNY ¥4,500-6,000 pcm was common (US$665-885). The lowest we heard was CNY ¥3,500 pcm (US$515) in less developed cities, rising to CNY ¥11,000 pcm in (US$1,625) on high rental cost sites in major cities.

However, the creation of CTC and the finalisation of the pricing formula in July 2016 have put downward pressing pressure on the market.

On the independent side, rates are now between CNY ¥2,300 pcm (US$340) to CNY ¥5,400 pcm (US$800). Again, desirable and highly coveted sites can still yield good rates. We were also told that the rate could also sometimes be higher if no one responds to an RFP.

CTC lease rates are significantly lower than anywhere else in the world, with estimates around CNY ¥26,000 per tower on an annual basis or CNY ¥2,166 pcm (US$320). This figure is surprisingly low and suggests a business model calibrated in favour of the MNOs. Since the summer, another industry report came out suggesting per tower leasing fee of around CNY ¥3,900 pcm (US$575) for CTC in 2015, and CNY ¥3,000 pcm (US$445) for 2016.

Like India, when additional tenants are added to Chinese towers, existing tenants’ leases are discounted.

Lease terms are typically 10+10 years.

Down payments for new sites have been reduced to a single year since the advent of CTC, adversely affecting independent towerco cash flows.

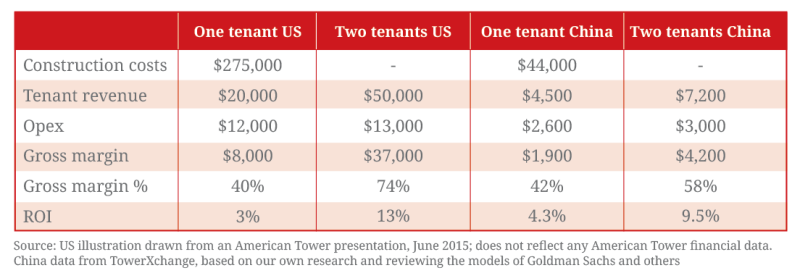

How do the economics of a single tower in China compare to the USA?

See “U.S. versus China macro tower build economics.” Note that when an additional tenant is added, lease rates are discounted for both the new and original tenant in China. This is not the case in the US.

We must emphasise that you must treat this table with a pinch of sale – China data is averaged based on multiple sources but all sources are subjective.

Who owns China’s broadcast towers are MNOs co-locating on them too?

China Broadcasting and Media Group has the 700 MHz license and owns most of China’s broadcast towers. TowerXchange have not yet been able to ascertain if these towers are offered for co-location by China’s MNOs.

Investment

How can early stage towercos in China access capital?

China offers a challenging path to scale for local tower entrepreneurs. Raising debt from Provincial financial institutions is complex, time consuming, and expensive. While private, domestic investment is gradually becoming more available to debt-funded infrastructure firms with contracted long term cash flows, like towercos, Chinese capital markets have historically been predisposed to invest only in profitable companies, at the expense of business models like telecom towers that naturally lend themselves to a degree of leverage. Small tower companies in particular struggle with the fact that towers are not securable.

State and provincial level investment funds may not be inclined to invest in entities which compete with State-owned CTC.

Please explain the latest rules regarding foreign ownership of, or investment in, communications infrastructure?

TowerXchange understand, but have been unable to confirm, that passive infrastructure is not considered a sensitive asset class, so FDI may be possible into Chinese joint ventures, particularly those in free trade areas, or through VIEs. We have heard unconfirmed reports of one foreign investor acquiring a 51% stake in a towerco.

An interested investor called attention to the VIE (Variable Interest Equity) structure, which enables foreign investors to invest in sensitive infrastructure, do investors still need to use this or is more direct investment now permitted given the recognition that passive infrastructure is less sensitive?

One TowerXchange source defined VIE as a mechanism for foreign direct investment in China via an international holding company, a WOFE (Wholly Owned Foreign Enterprise), in which USD, EUR or other currency could be invested, which could be registered in the Caymans, Delaware et cetera, and which could be listed on the NASDAQ or other international stock exchange.

The VIE structure was apparently first used in this sector over 20 years ago to facilitate investment in China Unicom, with subsequent VIE investments in Alibaba, Tencent and Baidu.

A critical question when leveraging a WOFE to invest in China is where the IP sits, at holding company or local subsidiary level? If the latter, international investors could be exposed to risk.

“A VIE would be a viable but suboptimal route to investing in a Chinese tower company,” said one interviewee. “Yes you can do it, but it may adversely affect valuation.”

What would foreign investors options be to repatriate capital?

In the event a foreign investor was seeking exit from a listing entity, they might seek to sell their equity to the domestically listed entity, releasing capital at an agreed exchange rate.

What are the potential exit strategies for investors in Chinese towers?

As in any market, exit strategies tend to focus on potential IPO or trade sale.

CTC may be a prospective trade sale counterpart, although management is very much focused on new builds and improving operations in its bid to IPO in Q42017. At least one of the Indonesian tower companies is believed to have an appetite to invest in China, while TowerXchange has learned of two domestic rollup plays.

Could a major international strategic investor be interested in acquiring Chinese towers? Probably not at the current scale of the independent market, where the largest independent towerco just hit five-digits tower count. But if an independent towerco could build or rollup 30-50,000 towers, they may attract interest from some of the more acquisitive international towercos.

When considering exit through IPO, the perception remains that Chinese companies need three years of profitable trading history to list as an A-share on the Shanghai Stock Exchange. There was some suggestion that unprofitable companies might soon be allowed to list, but apparently that potential reform will not take place imminently.

Some sources suggested that entities listed on that stock exchange can only accept investment in CNY, meaning foreign investors would have to exit at the time of listing, or setup a new entity. More recently it seems that qualified international investors can invest in companies listed on the Shanghai Stock Exchange.

There is one listed tower company on the Shenzhen Stock Exchange, Beijing Miteno Communication Technology Company Limited (300038), with at least one planning to list in Shanghai. It should be noted that there is approximately a two-year wait to list on the Shanghai Stock Exchange.

While the Shanghai Stock Exchange opens access primarily to domestic investors, a listing, or dual listing, on the Hong Kong Stock Exchange offers more exposure to international liquidity and an increased level of transparency with which international investors are more comfortable. Most of China’s large infrastructure entities are listed in Hong Kong.

Most stakeholders TowerXchange spoke to assumed a better valuation would be achieved on the Shanghai Stock Exchange (“the P/E multiple in Shanghai might be 30-50x compared to 10x in Hong Kong”), but there are precedents where higher valuations were realised in Hong Kong (e.g. in the insurance industry), while the current appetite of international investors for towers as an asset class, and the valuation of natural comps, may also contribute to a potential healthy valuation of a tower company on the Hong Kong stock.

Will it be possible to invest in CTC? Is there a plan to list China Tower Corporation on the stock market in future?

It’s been made clear that CTC is driving towards an IPO by the end of 2017 as a means of repaying China’s three MNOs the full value of injected legacy assets.

It seems increasingly likely that CTC will list on the Hong Kong stock, making it easier for international investors to buy equity.

U.S. versus China macro tower build economics

Who owns China’s broadcast towers are MNOs co-locating on them too?

China Broadcasting and Media Group has the 700 MHz license and owns most of China’s broadcast towers. TowerXchange have not yet been able to ascertain if these towers are offered for co-location by China’s MNOs.

Investment

How can early stage towercos in China access capital?

China offers a challenging path to scale for local tower entrepreneurs. Raising debt from Provincial financial institutions is complex, time consuming, and expensive. While private, domestic investment is gradually becoming more available to debt-funded infrastructure firms with contracted long term cash flows, like towercos, Chinese capital markets have historically been predisposed to invest only in profitable companies, at the expense of business models like telecom towers that naturally lend themselves to a degree of leverage. Small tower companies in particular struggle with the fact that towers are not securable.

State and provincial level investment funds may not be inclined to invest in entities which compete with State-owned CTC.

Please explain the latest rules regarding foreign ownership of, or investment in, communications infrastructure?

TowerXchange understand, but have been unable to confirm, that passive infrastructure is not considered a sensitive asset class, so FDI may be possible into Chinese joint ventures, particularly those in free trade areas, or through VIEs. We have heard unconfirmed reports of one foreign investor acquiring a 51% stake in a towerco.

An interested investor called attention to the VIE (Variable Interest Equity) structure, which enables foreign investors to invest in sensitive infrastructure, do investors still need to use this or is more direct investment now permitted given the recognition that passive infrastructure is less sensitive?

One TowerXchange source defined VIE as a mechanism for foreign direct investment in China via an international holding company, a WOFE (Wholly Owned Foreign Enterprise), in which USD, EUR or other currency could be invested, which could be registered in the Caymans, Delaware et cetera, and which could be listed on the NASDAQ or other international stock exchange.

The VIE structure was apparently first used in this sector over 20 years ago to facilitate investment in China Unicom, with subsequent VIE investments in Alibaba, Tencent and Baidu.

A critical question when leveraging a WOFE to invest in China is where the IP sits, at holding company or local subsidiary level? If the latter, international investors could be exposed to risk.

“A VIE would be a viable but suboptimal route to investing in a Chinese tower company,” said one interviewee. “Yes you can do it, but it may adversely affect valuation.”

What would foreign investors options be to repatriate capital?

In the event a foreign investor was seeking exit from a listing entity, they might seek to sell their equity to the domestically listed entity, releasing capital at an agreed exchange rate.

What are the potential exit strategies for investors in Chinese towers?

As in any market, exit strategies tend to focus on potential IPO or trade sale.

CTC may be a prospective trade sale counterpart, although management is very much focused on new builds and improving operations in its bid to IPO in Q42017. At least one of the Indonesian tower companies is believed to have an appetite to invest in China, while TowerXchange has learned of two domestic rollup plays.

Could a major international strategic investor be interested in acquiring Chinese towers? Probably not at the current scale of the independent market, where the largest independent towerco just hit five-digits tower count this year. But if an independent towerco could build or rollup 30-50,000 towers, they may attract interest from some of the more acquisitive international towercos.

When considering exit through IPO, the perception remains that Chinese companies need three years of profitable trading history to list as an A-share on the Shanghai Stock Exchange. There was some suggestion that unprofitable companies might soon be allowed to list, but apparently that potential reform will not take place imminently.

Some sources suggested that entities listed on that stock exchange can only accept investment in CNY, meaning foreign investors would have to exit at the time of listing, or setup a new entity. More recently it seems that qualified international investors can invest in companies listed on the Shanghai Stock Exchange.

There is one listed tower company on the Shenzhen Stock Exchange, Beijing Miteno Communication Technology Company Limited (300038), with at least one planning to list in Shanghai in 2016. It should be noted that there is approximately a two-year wait to list on the Shanghai Stock Exchange.

While the Shanghai Stock Exchange opens access primarily to domestic investors, a listing, or dual listing, on the Hong Kong Stock Exchange offers more exposure to international liquidity and an increased level of transparency with which international investors are more comfortable. Most of China’s large infrastructure entities are listed in Hong Kong.

Most stakeholders TowerXchange spoke to assumed a better valuation would be achieved on the Shanghai Stock Exchange (“the P/E multiple in Shanghai might be 30-50x compared to 10x in Hong Kong”), but there are precedents where higher valuations were realised in Hong Kong (e.g. in the insurance industry), while the current appetite of international investors for towers as an asset class, and the valuation of natural comps, may also contribute to a potential healthy valuation of a tower company on the Hong Kong stock.

Will it be possible to invest in CTC? Is there a plan to list China Tower Corporation on the stock market in future?

It’s been made clear that CTC is driving towards an IPO by the end of 2017 as a means of repaying China’s three MNOs the full value of injected legacy assets.

It seems increasingly likely that CTC will list on the Hong Kong stock, making it easier for international investors to buy equity.

Power

Are power costs passed through from China Tower Corporation to the MNOs?

According to the finalised pricing formula in July 2016, electricity input cost is part of the “product price,” aka lease rate to the operators. It is to be priced on a lump sum or itemised basis.

What proportion of the cell sites are on-grid, on unreliable grids or off grid?

Almost all sites are on-grid. Multiple sources confirm China has one of the world’s most reliable electicity grids. Unlike most countries, its supply exceeds demand.

What backup power solutions are typically on cell sites? Are towercos or MNOs responsible for them?

Towercos provide backup battery banks, typically with 4-8 hours float. Most batteries are lead-acid. There are very few backup DGs.

CTC is also recycling the battery from electric vehicles for site usage. Compared to lead-acid batteries, they are described as withstanding up to 60 degrees Celsius versus 35 degrees, is half the size and weight, and rechargeable up to no less than 500 times versus 300 times.

Are remote monitoring systems typically deployed on cell sites?

RMS is deployed on some, not all cell sites. CTC is considering making RMS a National standard.

Who is responsible for site modernisation and air conditioning, towercos or MNOs?

CTC is responsible for shelters and air conditioning.

While most new sites are built with outdoor equipment, few legacy sites have been modernised with, for example, free cooling.

Is there distributed renewal energy in China?

In September 2016 CTC reported having 10,177 solar and wind generation sites across the country, with annual capacity of 120mn kwH.

There is also news that CTC has plans to deploy solar on a large scale in line with the government’s objectives in reducing carbon emissions.

About document No. 92

Perceived as a turning point for the independent towercos in China, the document was released by MIIT and SASAC following an industry consultation meeting. This provided a much needed boost to the towercos who were facing challenging market conditions, roadblocks to securing and executing BTS, questions on the legitimacy of their presence in the market place, as well as difficulties with contracts and account receivables.

Document No. 92 spelled out some key points, among them that independent towercos, along with CTC, were to be included and part of the system supporting the country’s “co-build, co-share” vision; that should CTC lack the capacity or be unable to deliver on tower builds as agreed, it would revert the order back to the MNOs in a timely manner; that should inappropriate and anti-competitive tactics be used and thereby create a monopolistic market place, MIIT would take action to address and set forth corrective action. The document also noted other opportunities such as DAS and street poles that towercos could explore, to provide additional services within the general “co-build, co-share” framework.