Telecom operators need to develop larger, denser and more efficient networks to better handle the rising demand for mobile services. Their customers continue to gain access to advanced handsets and high bandwidth applications. This has led to a growing number of independent companies owning telecom tower infrastructure, as they can offer shared networks that can cut costs for the large mobile operators.

Typically, operators pay the tower owners rents under long-term, typically non-cancellable, contracts with annual escalators. Owning a mast has become an increasingly attractive investment for private and public investors keen to put capital to work in infrastructure-based assets with consistently compounding cashflows.

So, what are some of the key advantages of independently-owned tower companies?

Shared Infrastructure: Owning towers is not strategic for the carriers. They are non-performing, cost-centre assets with a carrier that can be readily monetized and turned into significant cash-generating assets in the hands of an independent tower company with no change in functionality for the carrier selling the towers. In addition, the present value economics of owning versus leasing favours leasing. Plus, zoning laws make it impractical for carriers to each have separate towers for every one of their sites. Shared infrastructure remains as the clear-cut most efficient way to deploy today’s networks, from both a cost and technological perspective.

Importance of scale:

- Negotiating with customers who are large, sophisticated multinationals with a history of putting pressure on their vendors. Scale enables tower operators to offer nationwide portfolios to facilitate the density requirements of modern wireless networks.

- It is a relatively capital-intensive business initially, so having significant financial assets is important as portfolios are constructed and acquired.

- Basic selling, general and administrative is not insignificant, but scalable with revenue growth given minimal incremental SG&A requirements associated with adding towers to an existing operation.

Mission-critical: Telecom tower companies are mission-critical as a high percentage of mobile traffic goes through their masts. Network quality is a major factor driving customer churn for wireless carriers and consequently, it remains a key factor in carrier marketing and will continue to be extremely important in an environment where delivering bandwidth-intensive content is a necessity to attract and retain customers.

ESG & sustainability: Simply put, fewer towers equals less visual pollution. Tower sharing is inherently green, more efficient and reduces the environmental impact of having redundant infrastructure.

The global market

TowerXchange tracks 275 tower infrastructure companies who collectively are estimated to own just fewer than 70% of the world’s 4.3 million investible towers and rooftops.

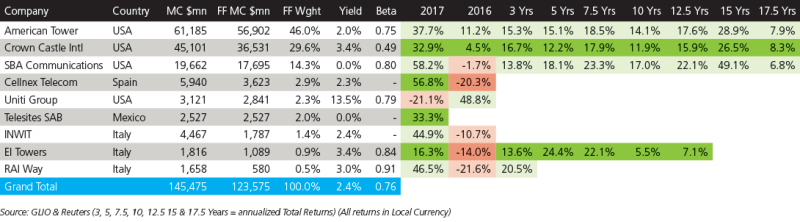

Table 1. shows the top 20 independent companies who account for approximately 2.2 million towers themselves. State-run China Tower is the largest owner with 1.9 million towers in China. It is a joint venture between network operators China Mobile, China Unicorn and China Telecom, and at the time of writing is expected to IPO in the 2018. Current valuations are upwards of $40bn. Listed companies are heavily represented in the table, with US-listed American Tower, Crown Castle and SBA Communications holding ranks 2, 4 and 9 respectively. Other listed companies come from Europe, India and Central America.

Table 1: Top independent global telecom tower companies (by number of towers)

Representation and developments

The tower business is very much a global affair, and there are a number of different regions with active independent tower companies.

For example, American Tower, Crown Castle and SBA Communications have been around for 20 years or more in the USA. These three tower specialists qualify under US REIT legislation, SBA the latest to convert in 2017. The US market is very well established, with independent tower companies owning close to 85% of collatable towers in the country according to EY.

Meanwhile, the UK market has three main independent players, Arqiva (whose IPO was scrapped in November 2017), Wireless Infrastructure Group and Cellnex, who own approximately 13,400 towers between them. According to EY, only 30% of UK towers are independently owned, which could lead to potential growth in the future. For this to happen, however, industry structure and the regulatory environment would likely need to improve.

In Continental Europe, the sector is slowly forming, with the IPOs of Cellnex, INWIT and Raiway in recent years. Mobile operators are looking to cut costs and raise cash. EI Towers has been around since 2004. However, independently-owned towers still only account for less than 20% of the European total according to EY, including Cellnex’ recent expansion into Switzerland with its purchase of approximately 2,200 towers from Swiss Towers.

Michele Vitale, Head of Investor Relations at INWIT gives a sense of the market: “The low teens EBITDA Growth INWIT is experiencing today is sustained by the growing demand coming from existing mobile network operators (MNO), new MNOs and other radio operators. Looking forward, the MNOs’ need for new infrastructure will accelerate due to increasing mobile data consumption trends, and this will translate into additional demands for shared infrastructure like DAS and Small Cells. In addition, the nature of 5G will reshape MNOs’ attitudes, increasing their wiliness to share a bigger part of the network: antennas, backhauling, tower data centres and more.”

Vitale continues; “Finally in Europe, due to the emerging nature of the market, we are in the phase of network optimisation. This means that the MNOs can help the market to become more efficient, by selling or merging their tower portfolios with specialist tower infrastructure companies.“

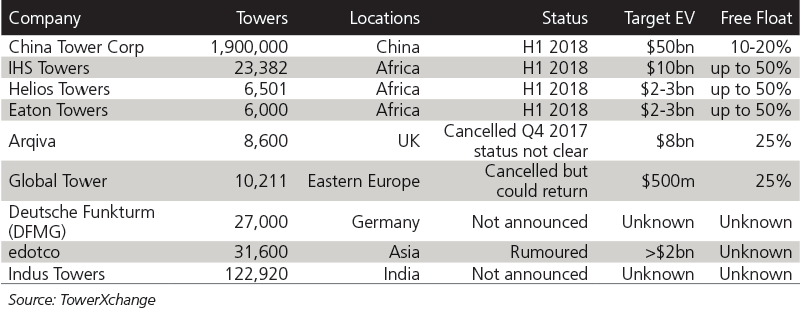

In Asia, China, India and Indonesia are all well represented in the league table, with multiple private independent tower companies operating in the region. IHS Towers ensures Africa is on list. In fact, the ownership structure of these companies could change in 2018 as Laura Graves, Managing Director at TowerXchange, explains: “Given the robust performance of the asset class across the board, there is a growing appetite among global investors for telecom infrastructure companies. With such favorable market conditions, a number of towercos have initiated the IPO processes, with a target listing date in 2018 [see Table 4]. Such listings combined equal an estimated USA$12-18bn of free float market capitalisation.”

Global growth and demand for mobile data

Understanding the strong secular backdrop of growth in global mobile data is the first step to understanding the sector and why it should be seriously considered by global institutional investors. This growth (to 2021), as highlighted in Table 2, is huge across all regions in the world. In virtually every industry, mobility is an emerging and potentially disruptive trend. The number of connected devices per capita, the average connection speed growth, growing video usage and mobile traffic per end user (per month) are all estimated to grow at startling rates.

Just looking at global connection speed growth of 24% CAGR and mobile traffic per month from 977MB to 5.7GB (42% CAGR) will offer vast potential for telecom tower companies going forward. Just scratching the surface on potential ‘next generation’ mobile network applications – the Internet of things, augmented reality, self-driving cars (and with them you really don’t want buffering issues) – provides some idea of the potential demands on capacity.

Table 2: Mobile user estimates 2021

To help address the massive network demand growth, wireless carriers and other customers within the mobile ecosystem are expected to utilize incremental space on telecom towers while also growing the number of sites they have within their respective networks. Part of this entails the deployment of new spectrums and the optimization (refarming) of existing spectrum bands with the associated equipment required to deploy them.

Empirical data shows carriers can most efficiently, both in terms of time and capital, achieve this by layering this on top of their existing locations (masts), leading to incremental revenue and cashflow for the tower companies. Existing sites are designed around these spectrum bands, serve the existing customer base, include fiber/microwave backhaul investments and have requisite power and security in place. Further, as mobile data usage grows, networks must become denser, so carriers are also expected to place equipment on additional masts over time where they may not already have equipment installed.

Importantly, the physics of signal propagation underlies the demand case for towers, both today and in the future, given the need for a high point to propagate signal over various spectrum bands in the vast majority of topographies. Unless these properties of physics are fundamentally altered (currently there are no indications of this), more equipment must be located on towers in the future to meet growing network usage, over and above the available incremental spectrum, and spectral efficiency improvements. The bottom line is that by 2021, industry projections suggest that there will be nearly 12 billion mobile connected devices globally, which is approximately 1.5 device per capita - an immense statistic.

Listed telecom towers investment case

Telecom towers represent the fifth largest sector in the GLIO infrastructure coverage and are fundamental to any infrastructure allocation. Manoj Patel, Managing Director at Deutsche Asset Management, indicates the importance of the sector in his infrastructure strategy: “We believe telecom towers play a primary role in a broader allocation to global infrastructure. Wireless communications have developed into integral part of the essential framework of the global economy. This will become even more vital going forward as future technologies emerge and the listed tower companies are ideally placed to take advantage of this.”

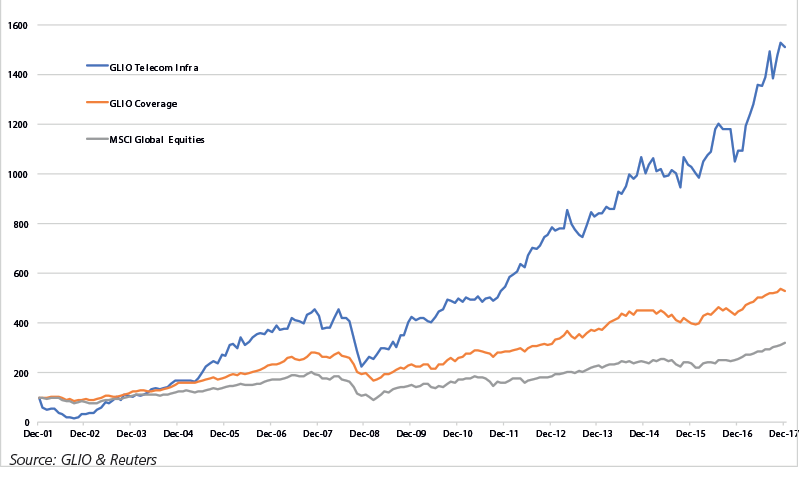

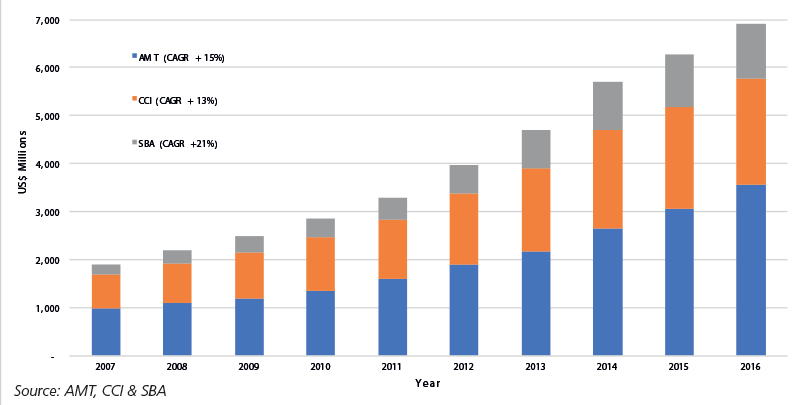

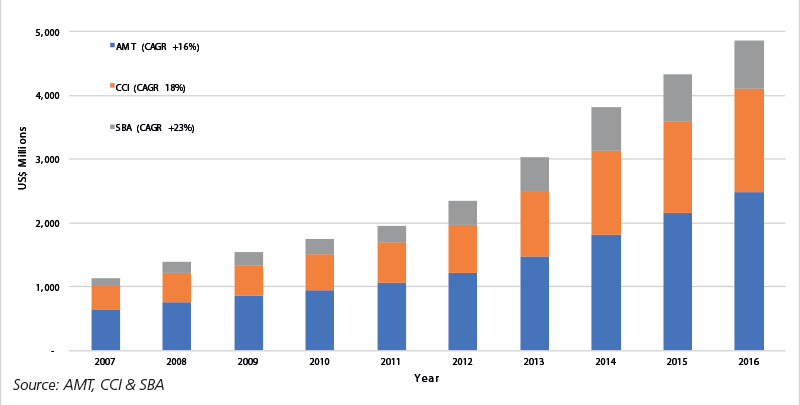

The long-term track-record of the large US-based tower companies has been more than impressive, as seen in Chart 1. and Table 3. Even ten-year annualised total returns of the large caps, which include the time periods around the global financial crisis, range between 12%- 17%. The periods around the GFC are truly phenomenal, as tower companies tended to materially outperform most other sectors as seen in Chart 1. Underpinning the growth of share prices are the underlying performance metrics of Adjusted EBITDA and Adjusted Funds from Operations (AFFO). Charts 2. and 3. show a consistent, stable and steady growth across these two metrics for the three major US tower companies.

When building a sensible allocation to the sector, investors will also look for a proven track-record in terms of shareholder return performance and management expertise. The access to the size, expertise, diversification and global network exposure offered by the listed telecom companies is unparalleled. In simple terms, it would take decades and $100s billions to replicate the network that they currently offer investors. Transparency, liquidity, yield and cost efficiency bolster the case.

Chart 1: Telecom towers vs. listed infrastructure & general equities

Table 3: Annualised total returns of global listed telecom infrastructure, as at December 29, 2017

Chart 2: Consistent Y-O-Y adjusted EBITDA growth

Chart 3: Consistent Y-O-Y adjusted AFFO growth

Conclusion

Telecom Infrastructure is a fundamental part of any global infrastructure allocation. It offers exposure to essential economic assets and services, and it leverages the exponential secular growth in global wireless usage as a key driver of demand. Looking forward, it seems likely that the percentage of independent tower companies will grow both in the listed and unlisted markets along similar lines as we’ve seen in the USA over the past 15-20 years.

Looking at the performance of listed telecom infrastructure, it has provided sustainable, long-term growth fundamentals which have subsequently generated impressive total shareholder returns for an extended period. Tom Bartlett, Executive Vice President and CFO of American Tower, sums up: “We are excited about the long-term growth prospects for our global tower assets and are focused on continuing to translate the secular growth in wireless communications into compelling, consistent total returns for shareholders. Whether in Delhi, Sao Paulo or Boston, our communications infrastructure is optimally positioned to serve as the backbone of today’s advanced wireless networks.”

Table 4: Global telecom infrastructure – potential IPOs

GLIO sector breakdown as at December 29, 2017

Industry comment

Dan Schlanger, Crown Castle’s CFO

“We see a tremendous opportunity to capitalise on the continued rapid growth in mobile data in the USA, which in turn drives demand for our unique portfolio of shared communications infrastructure. Carriers continue to leverage tower and small-cell infrastructure to add critical capacity to their networks as they keep pace with mobile data growth, which is doubling every couple of years. We are excited about the long-term opportunity to continue to deliver compelling total returns for our shareholders by generating significant growth and returning meaningful capital through dividends.”

About GLIO

The Global Listed Infrastructure Organisation (GLIO) is the representative body for the $2 trillion market capitalisation listed infrastructure asset class. GLIO raises awareness through education and promotion, targeting the global investment community. GLIO was established in June 2016.