This article introduces the history, business models and details the scale and growth of the telecom tower industry worldwide, drawing on TowerXchange’s unique proprietary research and data. TowerXchange is a research firm and community host focusing on the telecom tower industry. The renowned TowerXchange Journal is circulated to 35,000 decision makers, while TowerXchange also hosts Meetups for the top 250 tower decision makers in the European, African, Asian and Latin American markets. Read 2.5mn words of tower industry research at www.towerxchange.com.

Introduction to the telecom tower industry

TowerXchange see the tower industry as a parallel yet distinct segment of the telecom industry. Independent tower companies (“towercos”) separate infrastructure components of telecommunications from the more volatile retail components – towercos have no subscribers, no spectrum, and have reduced exposure to technology evolution. Towercos leverage long term contracts with credit worthy tenants to generate a predictable and highly investible cash flow.

Inaugurated in the mid 1990s in the USA and Canada, where towercos now own 73% of sites, the independent towerco model has evolved for different local market structures and cultures. Towercos now own 68% of India’s cell sites, 50% of the sites in CALA, 40% of Europe’s sites, 39% of the sites in SSA, and 100% of China’s towers.

Penetration of the towerco business model by region

Towerco growth worldwide

TowerXchange tracks 264 towercos that between them now own 2,936,086 of the world’s 4.3mn towers (68.2%).

Towercos’ reported EBITDA, based on the results of the top 15 listed towercos, grew at a CAGR of 10.75% between FY14-16, while aggregate site counts across the entire tower industry grew at a 14.61% CAGR over the last two years, driven by a combination of organic and inorganic growth.

Top 15 listed towercos’ EBITDA growing at 10.75% CAGR FY14-16 (US$mns)

Towercos are building a significant majority of the world’s new cell sites, including ground based towers, rooftops and, increasingly, small cells and DAS. Towercos are also acquiring an increasing proportion of existing cell sites, both through sale and leaseback transactions with MNOs, and through MNOs carving out the towers from their balance sheets to create their own ‘operator-led’ towercos. MNOs are motivated to monetise their towers to release capital to focus on their core business, to reduce debt, to unlock the efficiencies of shared infrastructure, to accelerate rollouts, and to exploit the difference in trading multiples: MNOs typically trade at 4-7x, while towercos trade at 10-21x.

Despite being created only 22 years ago, TowerXchange estimates that the telecom towerco ‘asset class’ should currently be valued at US$278.8bn.

Most valuable towercos by market cap in the US$278.8bn global tower industry

Market cap of listed entities taken at 27 May 2017, estimates for unlisted entities based on most recent refinancing plus industry sources

Contrasting towerco business models

Only 15% of the world’s towers and rooftops are owned and operated by ‘pureplay independent towercos’, yet those towercos represent over 60% of the capital value in the asset class. These valuations recognise the absolute independence of third party-owned, pureplay independed towercos as the optimum business model for shareholder value creation.

More than half the world’s towers are held by operator-led towercos, which TowerXchange defines as towercos that are majority owned by one or more MNOs, but which lease their sites to third parties on a non-discriminatory basis. One often finds that the business model for such towercos shares value creation more equitably with MNOs. For example, both of the world’s largest operator-led towercos, China Tower Corporation (1.7mn towers) and Indus Towers (122,730 towers) discount lease rates when additional tenants are added.

58,600 of the world’s towers are owned or operated by joint venture ‘infracos’, wherein two or three MNOs pool their towers but share only with each another. Joint venture infracos are currently only found in Europe, but the model is being replicated in Iraq and also potentially Saudi Arabia.

Just under a third of the world’s towers and rooftop sites, 1.36mn, are still owned by MNOs, but relatively few of these remaining captive sites are acquirable through conventional sale and leaseback transactions – at least, not if towercos comply with the investment thesis they’ve used to date.

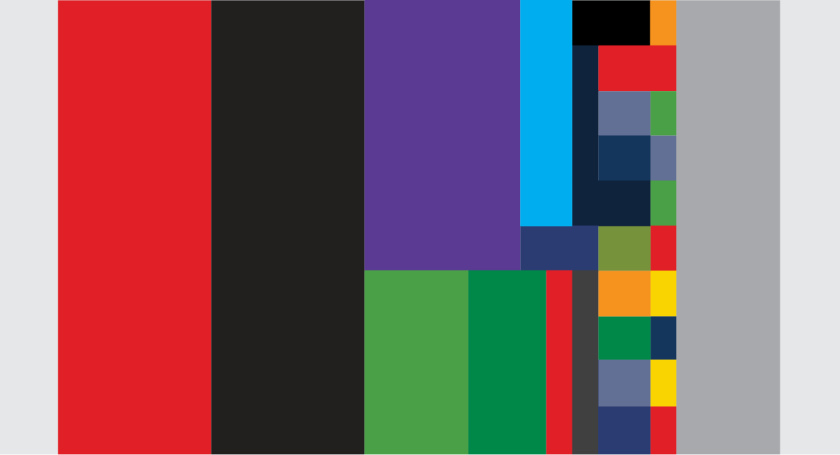

Global tower and rooftop ownership by business model

Tower and rooftop ownership by business model, by region

Diversification of business model

The business of building, buying and leasing up macro towers is a proven, investible proposition which has created companies that are among the largest in both the telecom infrastructure and the Real Estate Investment Trust (REIT) asset classes. And some towercos have little appetite to diversify beyond that proven business model. Other towercos embrace innovation to evolve the business model, positioning themselves as neutral hosts of a shared Future Network.

TowerXchange sees three clusters of business model diversification open to towercos. Firstly, in emerging markets towercos can expand their service proposition beyond vertical real estate to include provisioning primary and backup power. This innovation is well established by the ‘powerco’ towercos of SSA and Southern Asia, but in many instances such towercos are only harvesting the ‘low hanging fruit’ in energy efficiency, such as upgrading CDC batteries – unlocking the maximum energy efficiencies would require substantial investment in more capitally intensive renewables, which could be facilitated by partnerships with ESCOs, an option hitherto largely unexplored by towercos.

The second innovation cluster involves adding alternate site typologies to towerco catalogues. Towercos already offer the most familiar alternate site typologies by building new city poles or acquiring and leveraging existing street furniture. Many towercos already offer in building solutions, most frequently DAS – indeed in the US and UK towercos own many more DAS than MNOs. Early adopter towercos are already adding small cells to their inventory of site typologies – some functioning as site acquirers, with the small cells themselves owned by MNOs, while other towercos acquire and own their small cells – a segment which will be boosted as the first bona fide multi-operator small cells come to market. TowerXchange recently forecast that the towerco segment would deploy their millionth small cell or DAS by 2019.

The third cluster of innovations TowerXchange track are towercos exploring diversification into provision of fibre for shared backhaul. Crown Castle has acquired over 26,500 miles of fibre, Protelindo and STP in Indonesia have both acquired fibrecos, while IHS has acquired a license to rollout fibre in one region of Nigeria. TowerXchange are aware of several towercos with as much appetite to acquire data centre as tower portfolios. Data centres are not a significant departure – complex hub sites have similar operational requirements to data centres. Nonetheless, exploration of both fibre and data centres remains confined to early adopter towercos at this time.

Towerco business model diversification

The evolution of site design

The era of the single tenant tower is drawing to a close. Even MNOs with no plans to divest their towers frequently build new sites with the structural capacity to accommodate multiple tenants to facilitate bi-lateral swaps, or commercial leasing of excess capacity.

While structures need to be more robust to accommodate multiple tenants, the wind load, and power load, on sites is generally declining as successive generations of radio technology are lighter and as indoor sites are ‘outdoorised’. Cell sites in The Future Network must be modular and scalable.

30m+ ground based towers make up a declining proportion of new sites deployed by towercos. Lower, lighter infill sites make up the majority of orders for many towercos, and an increasing number of these infill ‘city poles’ are smart towers, with a variety of applications, from EV charging to advertising and information screens. Don’t assume that all new telecom structures will be made from steel - the leading pan-Asian towerco edotco have been pioneers in exploring carbon fibre towers and even a rooftop structure built from bamboo! Many new cell sites don’t look like cell sites at all – JCDecaux Link aims to leverage over a million bus stops and billboards as potential connectivity sites.

The innovations in site design have only just begun. If 5G is going to need 10x as many sites as 4G, then wireless sites must be delivered for a tenth of today’s capital outlay. An era of mass production, or mass installation at least, of cell sites is approaching. An urban cell site needs to be installed in hours not days. And maintenance visits must be kept to an absolute minimum to address the challenge of spiralling opex costs.

When is a tower not a tower? Alphabet’s X (sister company to Google) Project Loon proposes a network of balloons over 100km apart, which effectively function as a tower in the sky, capable of providing coverage to up to 5,000km². X reportedly has a queue of prospective MNO partners keen to deploy the innovation, and will soon have a viable commercial product. Meanwhile Facebook’s Project Acquila, which uses solar-powered drones, has also been piloted (without pilots!), while SpaceX are pushing a solution to provide high speed Internet from over 4,000 satellites. Will these innovations displace ground based sites as the de facto means of provisioning mobile coverage? Only time will tell, but innovators and incumbents alike are more inclined to label such innovations complimentary rather than competitive to the existing tower network, perhaps functioning to fix the economics of rural coverage.