Towercos have varying appetites to expand their footprint into new international markets, and as we look at the evolution and localisation of the towerco business model to meet the specific needs of those international markets, there is one inescapable conclusion: all towercos are not created equal. There is a world of difference between the U.S. blue print and the schematics of towercos in Central and Latin America, Africa, Asia and Europe. In this article we highlight the commonalities and focus on the differences to put some context around investments in this $192bn asset class.

Why are towercos so important?

A business model first conceived in the U.S. in the mid to late 1990s, independent towercos now own and operate 68% of the world’s 4.04mn telecom towers and investible rooftop structures.

The model is elegant in its simplicity. On an MNO’s balance sheet a tower is a depreciating asset built to serve one internal customer. On a towerco’s balance sheet a tower is a potential source of long term recurring revenue from multiple investment grade customers. Investors buy in to this now proven proposition and, recognising the separation of relatively safe haven infrastructure from retail risk, reward towercos with valuations in the 11-22x range – 3-6x typical MNO valuations, creating an incentive to re-engineer balance sheets, transfer towers from MNOs to towercos, and transform towers from cost centres into profit centres.

I’m going to steal a story from an advisor to an investor in one of the first tower sale and leaseback deals in the late 90’s. The CEO of the investor, who had arrived a little late for a meeting to discuss the deal, was reading the documentation to catch up on the detail of the transaction. As the towerco and MNO thrashed out the detail, the CEO flipped to the towerco revenue model, leaned in to his Associate and whispered: “This is how much money we make with one tenant on the tower?”

“Yes,” replied the Associate.

The investor’s CEO turned the page.

“And this is how much money we make with two?”

“Yes,” replied the Associate.

“Buy as many of these as you can!” Concluded the CEO of the investor.

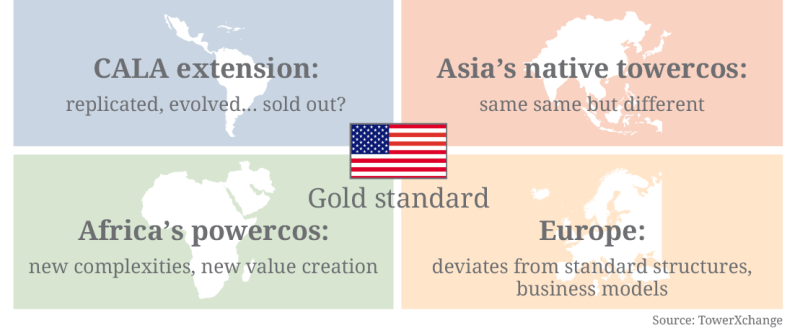

Figure one: global towerco business model variation summary

Variations from the U.S. “gold standard”

The independent towerco market in the U.S. is unlike any anywhere else in the world, creating a gold standard in terms of investibility which may be impossible to replicate in international markets.

Towercos played a central role in the U.S. catching up and surpassing the capacity and quality of mobile networks in much of the rest of the world. Towercos built much of the U.S. network, and North American MNOs are almost uniquely dependent on towercos. U.S. towerco contracts, lease rates and escalators capture tremendous value on towerco balance sheets – but it has not always been possible to follow the same roadmap in international markets.

The closest resemblences to the U.S. model are to be found South of the border in Latin and particularly Central America, where the Master Lease Agreements which underpin towerco business models were copied from the U.S. However, there are finite remaining opportunities for large scale growth in the CALA tower markets, with the exception of Argentina.

Indonesia is another tower market where the towerco business model is relatively similar to the U.S. Michael Gearon, one of the forefathers of American Tower’s CALA business, brought the U.S. blue print with him as one of the founders of Indonesia’s largest towerco, Protelindo. Again most of the towers which can be bought by towercos, have been bought by towercos in Indonesia.

Most emerging market towercos, in Sub Saharan Africa and Southern and Southeast Asia, provide power as a service as well as telecom structures, exposing this formerly real estate-centric business model to the complexities of challenging energy logistics.

Meanwhile in the new European tower market, we see a lot more variety in both site typology and in towerco business model, particularly in over-built markets where as much value may be created through decommissioning parallel infrastructure as through building new sites.

Figure two: Who owns the ~150,000 towers in the U.S.?

A closer look at the U.S. tower market

Figure two illustrates what investors in the mature U.S. tower market are used to seeing: a big red, independent towerco-led ecosystem. North American telecom infrastructure is dominated by three publicly listed towerco giants; American Tower, SBA Communications and Crown Castle, with a couple of rollup plays consolidating a few thousand further towers, and a long tail of almost 100 independent developers.

AT&T, T-Mobile and Sprint have sold the majority of their towers, but retain a total of 7,524 towers within captive, operator-led towercos. Together U.S. independent and operator-led towercos own 82% of the investible towers and rooftops in the country.

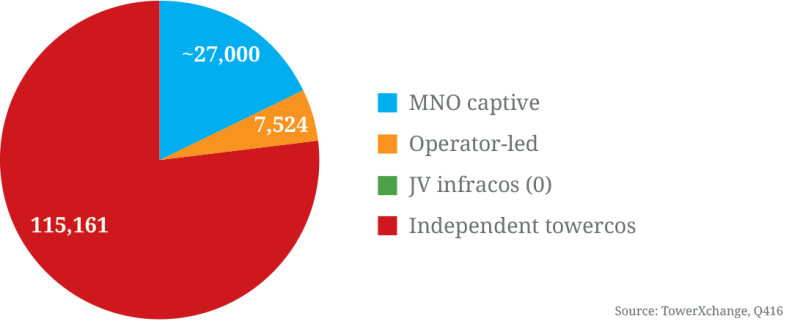

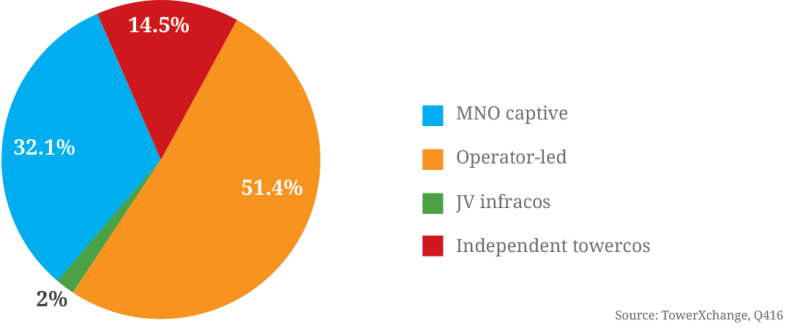

Figure three: Breakdown of ownership of the world’s 4,041,062 investible towers and rooftops

The fragmentation and localisation of the towerco model

The picture is quite different globally though, with pure play independent towercos, again shown in red in figure three, owning only 14.5% of the towers. More than half the world’s towers are held by operator-led towercos; towercos that are themselves majority owned by MNOs. Admittedly the figures are someone distorted by the sheer scale of China Tower Company and Indus Towers with over 1.7mn and 120,000 towers respectively.

Just under a third of the towers and investible rooftops, almost 1.3mn, are still owned by MNOs, but relatively few of these remaining captive towers are acquirable through conventional sale and leaseback transactions – at least, not if towercos comply with the international investment thesis they’ve used to date.

So how does tower ownership break down regionally?

India has twice as many towers held by operator-led towercos, such as Indus Towers and Bharti Infratel, as pureplay independent towers. The dominance of operator-led towercos has created a business model where the value created by infrastructure sharing is shared more liberally between MNOs and towercos in India – we’ll explain the detail later.

71.5% of towers remain on MNO balance sheets in the relatively immature tower markets of Southern and Southeast Asia (excluding India), although TowerXchange foresee more tower transactions here than any other region in the coming 12-18 months.

There’s also deal flow to come in Europe, where 62% of towers remain operator captive, but where a number of tower portfolios retained on MNO balance sheets, and operator-led carve out towercos, could be monetised. M&A is in part driven by the acquisitiveness of Cellnex and the renewed European appetite of American Tower after the restructuring of ATC Europe as a joint venture with Dutch pension fund PGGM.

There is a nascent tower market in the Middle East, where almost all towers remain on the balance sheets of MNOs who have less imperative to raise cash. However, opportunities to create efficiencies through decommissioning of parallel infrastructure have resulted in the creation of entities like Fanasia in Iraq and the potential STC-Mobily joint venture infraco in Saudi Arabia.

But what really distorts the global map is China, where the transfer of all 1.7mn MNO towers to China Tower Company, which remains 94% owned by those carriers and thus itself represents 82% of the world’s operator-led towers.

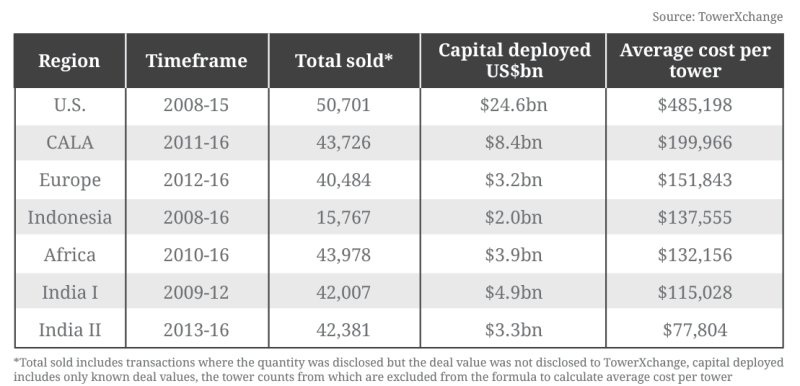

Figure four: Average cost per tower comparison

Average cost per tower comparison

Before I dig into the detail of the structural differences between tower markets, let me preface by calling attention to an important fact: the differences in towerco business models are reflected in valuations.

Cost per tower (see figure four) is a pretty savage valuation, not taking into account lease rate, term or escalators, but with the opacity of most tower transactions it’s difficult to elicit a superior and consistent set of metrics.

You’re unlikely to get change from half a million bucks for a decent U.S. tower these days – a premium driven by scarcity, zoning restrictions creating barriers for entry, and high capex costs.

We think valuations are peaking in CALA at around 40% of U.S. levels, while European towers have been changing hands for an average of around US$150,000 each.

Fierce competition for sale and leasebacks in Indonesia is keeping valuations at a little over US$130,000, around double replacement cost, which in turn fuels healthy organic growth. Average cost per tower is similar in Africa, where the tower transaction deal pipeline is slowing, with just a handful of Airtel towers left to sell, and some mid-level operators’ towers coming to market in Kenya, Senegal and Mozambique.

Meanwhile India demonstrates the impact of market restructuring: before 122 MNO licenses were cancelled in 2012, towers were changing hands for around US$115,000. With deal flow resuming in India after a nearly four year hiatus, valuations have fallen by more than 30%, albeit in a more rational MNO market: towers in India are settling into valuations around US$75-80,000 each, and the consistency of terms, including lease pricing, means we are unlikely to see significant variation from that number as 4G continues to drive consolidation in the Indian tower market.

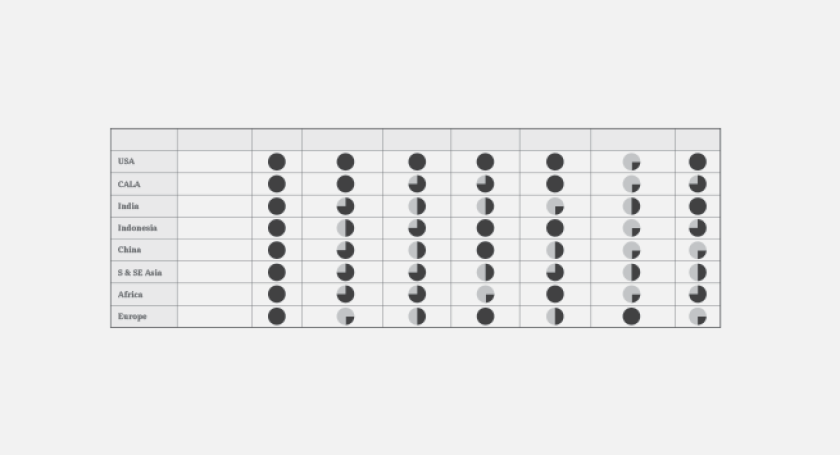

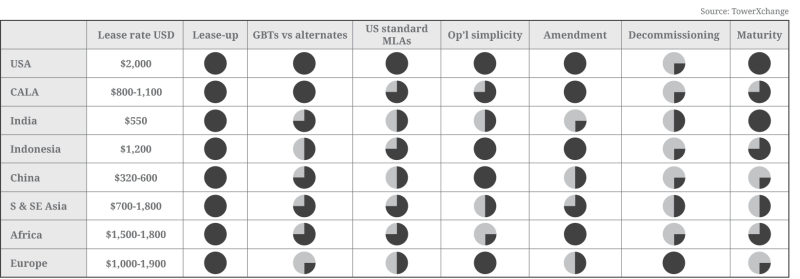

Figure five: At a glance business model comparisons

At a glance business model comparisons

Figure five provides a simplified comparison of different facets of the towerco business model.

Lease rate: presents an estimated average lease rate for the region, or range where there is wide variance within the region.

Lease up: the one factor in common with every regional variation on the towerco business model is a focus on creating value by leasing up towers to multiple tenants.

GBTs (ground based towers) vs alternates: compares the mix of site typologies within typical towerco portfolios, ranging from 4/4 quadrants, reflecting that a significant majority of sites are GBTs, 3/4 a smaller majority of sites are GBTs, 2/4 about half and half, 1/4 indicates that the majority of sites are non-GBTs, such as in Europe where the majority of cell sites are rooftops and alternate site typologies (water towers, church spires, billboards and other street furniture).

U.S. standard MLAs: simplified comparison of typical MLA structure with the MLA structure found in the oldest tower market, the U.S.

Op’l (operational) simplicity: the more quadrants, the simpler the business model. 4/4 quadrants indicates a pure ‘steel and grass’, real estate oriented model. Complexity typically originates from energy logistics or particularly challenging operational circumstances.

Amendment: indicates whether towercos derive ‘amendment’ revenue when an existing tenant pays another tenancy fee for overlaying a new technology. For example, amendment revenue is a significant value driver in the Americas, whereas in India amendment (there known as “loading”) derives only a modest one-off execution fee.

Decommissioning: indicates the degree of value creation potential through the decommissioning of parallel infrastructure. Decommissioning is where towercos acquire two towers in overlapping locations, break the lease and dismantle or ‘moth ball’ one tower, and consolidate tenancies onto the other. 4/4 quadrants indicates the highest level of opportunity for decommissioning, down to 1/4 representing the lowest.

Maturity: sums up the maturity of the tower market in terms of longevity and how established and consistent contract structures and business models are.

Reviewing figure five, the first row illustrates the gold standard: everything in the U.S. is how tower investors might want it to be. Telecom infrastructure consists primarily of high structural capacity, ground based towers, and towercos operate a low operational complexity, “steel and grass” model providing just the structure and the real estate. A strong Master Lease Agreement defines a healthy lease rate, averaging around US$2,000, often with fixed escalators that have been running for as many as 20+ years in what has been a low inflation environment. Amendment revenue has been another significant value driver for U.S. towercos, while zoning regulations mean there is minimal parallel infrastructure, so minimal need for decommissioning. The downside? The U.S. tower industry is mature, so there are finite remaining growth opportunities. Hence American Tower and SBA pursuing international opportunities, while Crown Castle diversifies into fibre and small cells.

So if you can only invest so much in the U.S., how do international markets compare?

Let’s look at the CALA region. Since shortly after the turn of the millennium, U.S. towercos have extended their footprints into Central and Latin America, initially using the same contract templates as in the U.S. in Central America, but gradually evolving – for example ground rent was a pass through in much of South America, which meant towercos had less direct relationships with landlords, although this is changing. Pricing is often pre-agreed in South America, with escalators CPI linked, which again differs from the U.S.

The CALA tower market really took off in the last eight years, with a wave of sale and leasebacks, and an independent developer segment evolving in parallel.

Recently lease rates in CALA have come under downward pressure, with the impact on margins compounded by forex devaluations and rising land costs. Independent developers are often undercutting the U.S. publics, slowing their organic growth prospects. Lease rate discounting and deviation from standard MLA terms has been so dramatic on the part of some independent developers that some may be uninvestible by the U.S. publics.

With half of CALA’s towers on towerco books, but with América Móvil and Telefónica launching their own operator-led towercos in the last 18 months, the continent is almost sold out, notwithstanding a few virgin markets (Argentina, Cuba) and the prospective rollup of the aforementioned independent developers, who own 12,216 of the region’s 164,207 towers.

Meanwhile in Asia a native tower industry with an entirely different genetic code was evolving. There are a handful of towercos evolving to broadly replicate the U.S. blue print – especially those in Indonesia. And there is some commonality in India among the many entities now rolled up into American Tower India, but even these independent towercos tend to conform to the lease pricing and contractual terms set out by the majority of operator-led towercos – and it is these operator-led towercos that largely define the unique Asian tower market structure.

Vodafone, Idea Cellular and Bharti Airtel’s joint venture Indus Towers, and their close cousins Bharti Infratel, remain majority owned by MNOs. While 28% of Bharti Infratel is already owned by public shareholders, both they and Indus Towers may see investment by third parties in 2017. The genetic code of operator-led towercos generally leaves them predisposed toward a more equitable share of value creation across balance sheets; lease prices are generally lower, “amendment revenue” or “loading” is sometimes treated very differently. In India, when a new tenant is added to a tower, the original tenant enjoys a 20% discount on their lease rate, with a 30% discount for a third tenant, and India has even introduced parity in lease price escalation to ensure anchor tenants pay the same as new tenants.

When reviewing Asia, edotco merits special mention. While the carve-out towerco remains majority owned by Axiata, and thus is classified by TowerXchange as operator-led, edotco recently raised US$600mn by selling undisclosed stakes to INCJ and to Axiata’s majority investor Khazanah. edotco seeks to draw from the ‘best of both worlds’ – driving value and efficiency under independent towerco-like commercial terms, yet with a deep appreciation of their clients’ perspective, drawing upon edotco’s own heritage as a carve out from an MNO.

China stands apart from our analysis of Asia as a unique market with huge volumes of new build. With lease prices reportedly as low as US$320-600 the question remains whether, in the run up to IPO anticipated in late 2017, China Tower Company can transform itself into a highly investible profit centre, like its Western counterparts, or whether the indebted towerco is destined to be a cost centre, enhancing the value of its parents China Mobile, China Unicom and China Telecom, who between them own 94% equity.

The operator-led towercos of Asia generally have a symbiotic relationship with their parent and tenant MNOs which enables them, among other things, to position themselves to take a leadership position in the creation of Smart Cities and the implementation of heterogeneous networks.

As the ‘Big Four’ towercos who dominate the SSA tower market mature toward consolidation or IPO, the investment community needs to be cognizant of the unique hybrid towerco-powerco business model in Africa. Outside of South Africa, which more closely resembles the U.S. ‘steel and grass’ business model, towercos in Africa are as much energy logistics businesses as they are real estate companies. This has implications both bad and good: one, they are more complex, more exposed to the vagaries of fluctuating oil prices and forex; but two they have another means of creating and capturing value – in fact the towercos in both Africa and Asia are smartly deploying capex to reduce energy opex and improve their margins.

And finally to the new European tower market, effectively kick-started by Cellnex and their insatiable appetite to rollup European towers – Cellnex entered three new countries in the second half of 2016! The European towerco business model deviates significantly from the U.S. blueprint because the network topology differs so significantly. While the majority of U.S. sites on American Tower, SBA and Crown Castle’s balance sheets are ground based towers, in Europe almost all urban and many suburban sites are rooftops – as much as 60% of Europe’s 600,000 cell sites are rooftops and other alternate site typologies. This brings the landlords into play as greater stakeholders, and European landlords are savvy, often demanding supplementary rent with the addition of a second tenant, which significantly recalibrates the model.

Contract structures vary across Europe. In some markets amendment revenue can be generated much like the U.S., while in other markets an anchor tenant has retained substantial reserve space effectively nullifying potential amendment revenue.

Europe is simply a much more mature, built-out – in fact over-built – network, and investors are always keen to seek evidence that larger scale decommissioning plays can generate returns within an optimal two to three year timescale.

Seeking to extend the global tower industry growth narrative

With 68% of the world’s towers on the books of one type of towerco or another, there are obviously reducing inorganic growth opportunities, and one must remember that towercos do no want all the towers. Parallel infrastructure may have limited value as any need for infill sites may be offset by the cost of decommissioning duplicate sites – so in some markets only one or two of the three-plus tower portfolios may be investible. The attractiveness of buy and leasebacks with so-called tier two MNOs is further reduced as no-one wants to do a tower deal with an anchor tenant who can’t pay their bills.

With the USA effectively sold out, just a handful of portfolios left up for grabs in India, with the majority of tier one MNO towers in Africa sold, and with Telesites and Telxius reducing the chance of acquiring América Móvil or Telefónica towers in CALA, how can listed and other acquisitive towercos extend their growth narrative?

With the USA effectively sold out, just a handful of portfolios left up for grabs in India, with the majority of tier one MNO towers in Africa sold, and with Telesites and Telxius reducing the chance of acquiring América Móvil or Telefónica towers in CALA, how can listed and other acquisitive towercos extend their growth narrative?

Private towercos can sometimes be more flexible and agile than the U.S. publics, who have been very disciplined buyers to date: they have their investment thesis and they stick to it. The publics have the discipline to walk away from a deal if they don’t like the terms or valuation, giving rise to the growth of private towercos like IHS, Helios Towers Africa and Eaton Towers in Africa; Phoenix Tower International, Group TorreSur and Digital Bridge in the Americas, and a host of private towercos in Myanmar. Some of these private towercos can achieve scale rolling up tower portfolios that are lesser priorities for listed towerco giants, a strategy often predicated upon an eventual sale to one of those listed giants once the assets have been ‘cleaned up’ (structures or permitting improved et cetera).

Further sale and leaseback opportunities may require that bidders move outside their comfort zone, whether it be by allowing an MNO to retain a significant stake in a joint venture (as IHS did in Nigeria, where MTN retained a non-controlling 51% equity stake, a stake since restructured to additional shareholding at the group level), or requiring bidders to entertain opportunities in markets with foreign direct investment limits, like Algeria and Bangladesh.

TowerXchange see an increasing proportion of future transactions being towerco-on-towerco consolidations, which has driven valuations in Europe and Africa for example, but it has been precisely the listed towercos’ refusal to pay a premium for independent developer towers that has effectively stalled deal flow in CALA.

Diversification: how do the economics compare?

If towercos are running out of ground based towers to buy, they can always diversify into the provision of other assets and services.

The economics of alternate site typologies varies as a function of the contractual relationship with the asset owner. For example, a towerco can make a small margin from aggregating privately owned rooftops for MNOs, or they can acquire rights very similar to an owner and derive a similar margin as they do from a macro tower. For example, American Tower recently announced a deal to acquire innovative French towerco FPS, which had acquired rooftop management firm LOXEL with access to 20,000 rooftops, and which had struck deals with highway infrastructure provider APRR and the electricity transmission tower operation subsidiary of EDF for 300 and 76,000 sites respectively.

In the U.S. we’ve seen Crown Castle, American Tower and Digital Bridge bet big on small cells and DAS, a strategy replicated by Cellnex, INWIT, Wireless Infrastructure Group and Arqiva in Europe, and by the Indonesian towercos. Small cells, and their larger cousins microcells, lamp posts and DAS, provide infill solutions that will be particularly important to realise the LTE experience, to enable Smart Cities and the IoT, and for 5G. TowerXchange are increasingly convinced that the majority of such sites will be provisioned to multiple operators by towercos and specialist independent distributed network operators, rather than being self-deployed for the usage of a single MNO.

While there’s enough DNA in common with the tower business for small cells to be a natural diversification for towercos, new skills in active network management are required, the business can be more SG&A heavy, and the ecosystem is more fragmented than for macro cells. To drive a small cells business to scale, one has to build relationships one municipality and one landlord at a time.

We have also seen towercos diversify into fibre; it’s a big part of Crown Castle’s current strategy in the U.S.; Protelindo, STP and Balitower own significant fibre assets in Indonesia; and fibre may be a big part of IHS’s future in Nigeria. Even the private towercos are looking at fibre: for example, Brazil’s third largest independent developer Brazil Tower Company has spun off a subsidiary Arqueiro Telecom.

Ultimately, small cells and fibre are yet to be explored by the majority of towercos, and there may be merit in focusing on core competencies. TowerXchange offer one simple conclusion: we like to see towercos committing to diversify into small cells, or committing to focus on their core business of macro sites. Any towerco that dabbles half-heartedly may quickly find themselves overtaken by competitors in the land-grab for the heterogeneous network layer.

What’s next?

There are 18 listed towercos worldwide (American Tower, Balitower, Bharti Infratel, Cellnex, Crown Castle, DIF, EI Towers, GTL, IBS, INWIT, Miteno, OCK, Protelindo, RAIWAY, SBA, STP, Telesites and Tower Bersama). With the cancellation of Telxius and Global Tower IPOs, and with U.S. towercos taking a valuation hit with the country’s surprise election result, 2016 hasn’t been the best year for towerco equities, although it certainly hasn’t seen the carnage witnessed in 2002 when the technology bubble burst and investors misdiagnosed towercos as tech rather than infrastructure plays, taking American Tower, Crown Castle and SBA down to penny stocks and taking some of their competitors out of business.

2017-18 should be better years for listed towercos and for towerco IPOs. China Tower Company are driving toward an IPO at the end of 2017, edotco may follow in 2018. IHS increasingly looks too big for a U.S. public to digest – they may follow their US$800mn bond with an IPO in the next couple of years. Arqiva could utilise the public markets to restructure their balance sheet, although a strategic sale seems equally likely. Deustche Telekom continue to consider whether to list, sell or retain the 31,000+ sites they own within Deutsche Funkturm. And Telefónica and Turkcell could reconsider listing their operator-led towercos (Telxius and Global Tower respectively) in a more receptive market. Meanwhile, the need to raise capital for 4G could see further major transactions in the Indian Tower market.

Conclusion

After spending five years of contrasting international tower markets to the U.S. for investors more familiar with the ‘oldest growth’ North American tower market, it has become increasingly clear to me that we may never see tower investment opportunities to match the ‘gold standard’ seen in the U.S. North America’s tower networks were largely built by towercos, U.S. carriers are uniquely dependent on towercos, and the calibration of lease rates and escalators in the country has created highly investible infrastructure asset class.

The often-subtle differences between international tower markets and towerco business models create new value drivers, but that doesn’t mean we think international tower markets are less investible; valuations both of equities and in private transactions reflect the premium value of U.S. towers, and the relative value of international assets.

All towercos, and all international tower markets, are not created equal.