After weeks of expectation, Tigo has finally sealed its first tower deal in Paraguay and sold around 1,400 towers to American Tower for a total approximate value of US$125mn. The deal could very well represent the first of a series of transactions involving not only Tigo but other players in the MNO space. In this first article, TowerXchange takes a look at its telecom market, regulatory environment and the potential for M&As and build to suit (BTS) activities.

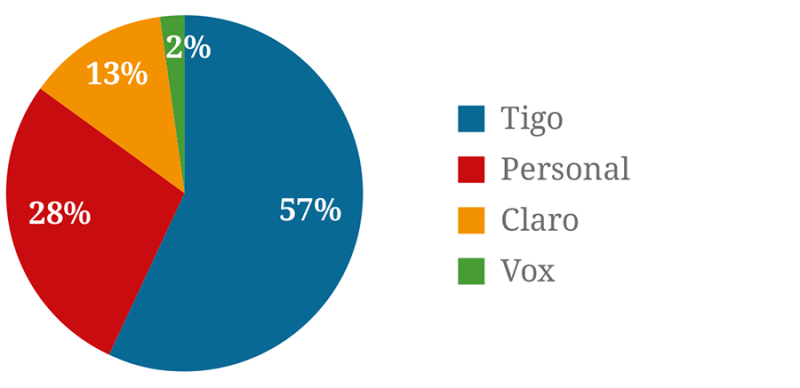

Paraguay’s mobile market is served by four MNOs: Millicom’s Tigo, Telecom Argentina’s Personal, América Móvil’s Claro, and Copaco’s Vox. The health of the mobile sector is partly attributable to the poor level of service of fixed-lines, which has made Paraguay the country with the highest number of mobile phones per fixed line (18 mobiles for every fixed line).

Paraguay: Mobile market share

In December 2015, telecom regulator Conatel completed the 1,700MHz and 2,100MHz spectrum auction which granted both Claro and Tigo 4G licenses, costing the two MNOs a combined US$90mn. Since then, Tigo has announced investments in excess of US$600mn for the quinquennium 2016-2021 and the goal to cover 66% of the population with LTE services by the end of 2020, corresponding to 250 locations throughout the country. Tigo passed the 300,000 4G subscriber threshold at the end of 2016. Part of Tigo’s capex is being financed by the Inter-American Investment Corporation (IDB Group), whose involvement in the country includes over 600 projects in a variety of industries and total loans of US$1.33bn.

Nucleo Personal has a similar number of 4G subscribers, having announced passing the 250,000 milestone in October 2016. Personal has over 1,500 base stations in Paraguay, and plans to add 600 for over the next three years.

As part of the country’s national broadband plan, Conatel has approved the Plan Nacional de Telecomunicaciones 2016-2020 (National Telecommunications Plan 2016-2020) which sets goals such as granting mobile access to 80% of the population as well as several broadband-related targets. The full text of the Plan Nacional de Telecomunicaciones can be found at this link.

Back in 1995, the government has created the Fondo de Servicios Universales or FSU (Universal Service Fund) which is administered by Conatel and whose mission includes the enhancement of infrastructure and mobile coverage, universal internet access and the creation of a national emergency network. So far, the FSU has been able to set up free wireless connectivity in fifty town centres across the country.

Conatel announced back in 2016 that it would launch a 700MHz and a 2.6GHz auction for additional 4G spectrum in Q1 2017 but for now plans haven’t been announced and local sources suggest that the auction might take place towards July.

Paraguay: Estimated telecom infrastructure

paraguay-infrastructure.png

Operations

The grid is reliable and extensive in Paraguay - the country enjoys 98.2% electrification - but remote monitoring is widely utilised. Personal’s sites were being managed by Westell in 2014, who may also be managing the Claro sites after Westell’s acquisition of their RMS partner Kentrox.

Conatel’s broadband coverage project in the sparsely-populated Alto Chaco region, structured as a PPP with Tigo, was expected to make extensive use of renewable energy.

What’s in it for towercos

Millicom’s Tigo has agreed to divest well over half of its 2,000 towers to American Tower. As expected, the valuation is lower than regional standards (US$125mn - US$89,285 per tower) due to the limitations on the length of land leases, currently capped at five years, as well as the rising real estate costs.

This is the second deal Millicom seals in the region following the 2011 Colombian sale and leaseback transaction with American Tower, where the MNO divested 2,126 towers for US$182mn. And since Tigo has been acquiring several cable companies in addition to its 4G investments in Paraguay, the divestment of some of its tower assets is a natural - and welcome - move.

Local sources suggest that the market might soon be ready for another transaction and that Personal’s ~1,100 towers might come to market soon. What’s left to see is whether American Tower can take advantage of its early move into the country and sweep that portfolio as well or if other towercos might try to enter the market.

On the other hand, the overall level of mobile infrastructure in the country is good. Local experts don’t foresee the need for significant densification in the imminent future, which might mean that inorganic rather than organic growth opportunities remain foremost in the country for the time being.

In conclusion, Paraguay represents a relatively low risk, moderate growth opportunity for a towerco seeking to consolidate their footprint in CALA. The size of the market makes the opportunity more comparable to a Central American country than to its South American neighbours, but FX has been less volatile than in much of the rest of the region, and the economy looks stable.