Infrastructure sharing in Bangladesh started back in the early 2000s, when the first barter arrangements took place between two MNOs CityCell and Aktel (now Robi). Commercial tower sharing then kicked in following the introduction of tower sharing guidelines by the BTRC. Grameenphone was the pioneer, establishing its wholesale business division back in 2010, followed by others in 2013 and 2015. The industry however is at an inflection, as the BTRC seeks to finalise its towerco licensing regime, with potential implications for the current model.

TowerXchange: Please introduce yourself and your role.

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

My name is Md Mainur Rahman Bhuiyan and I am the Director and Head of Infrastructure Business at Grameenphone. I am responsible for developing and maintaining profitable growth of the Infrastructure sharing business in order to achieve both short- and long-term strategic objectives and sustain market leadership as a provider in site sharing.

TowerXchange: Please tell us about Grameenphone’s operations and tower portfolio.

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Grameenphone Ltd. (GP) is the largest mobile telecommunications operator in Bangladesh in terms of revenue, coverage, and subscriber base of 55mn. Among Telenor Norway’s operations in 13 countries, Grameephone is fifth in position in terms of revenue. The company was incorporated on 10 October, 1996 as a private limited company and later became a publicly limited company (Telenor Norway 55.80%, Grameen Telecom Bangladesh 34.20%, and the rest 10.00% are public).

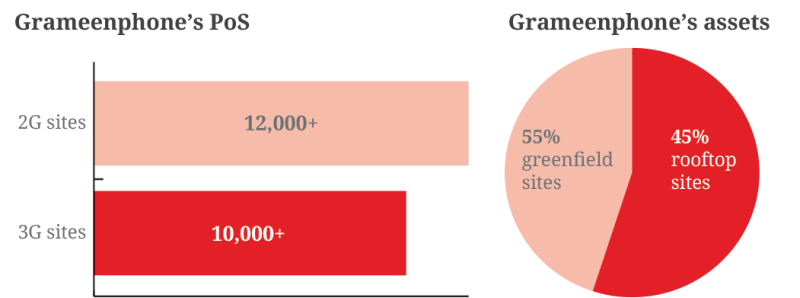

In terms of our tower portfolio, we have a robust network covering 99%+ of the population, with 12,000+ 2G sites and 10,000+ 3G sites. The split for greenfield sites versus rooftop is 55% to 45%. Our coverage ranges from metro city to deep rural areas.

TowerXchange: What can you tell us about the degree of infrastructure sharing within your portfolio? Who are your clients?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Infrastructure sharing by the MNOs can be divided into two major categories in Bangladesh. One is site sharing and the other one is transmission capacity sharing. There are currently 35,000+ towers in Bangladesh, of which 6,500+ towers have been shared among the operators to date.

Grameenphone’s major customers in infrastructure sharing are MNOs (Banglalink, Robi-Airtel, and Teletalk), WiMax operators, NTTN operators, and ISPs.

Revenue market share of MNOs in infra-sharing

TowerXchange: Can you give us a bit of background on the evolution of infrastructure sharing in Bangladesh?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

The first arrangements took place back in 2003, as barter between CityCell and Aktel (now Robi), then CityCell and Warid (later becoming Airtel and who has recently merged with Robi). Around 2008 the BTRC (Bangladesh Telecommunication Regulatory Commission) came out with the first set of guidelines for infrastructure sharing in the country, with amendments in 2011. Formal infrasharing under the BTRC guidelines was kicked off by Grameenphone in 2010, followed by edotco (subsidiary of Axiata’s Robi) in 2013, and Banglalink in 2015.

TowerXchange: The BTRC recently sought consultation from the industry on the tower license framework. What does the framework propose, and what was the focus of your feedback?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

The draft towerco guideline proposes a number of changes to the current model in practice by the industry. To highlight a few:

1) MNOs will have to roll back the current tower leasing agreements as the towercos will be rolling out following the licensing condition.

2) Towercos may source towers from the existing operators through sale/rent.

3) MNOs will not be allowed to build their own towers, and instead have to source from the towercos.

So the framework proposes that no other entity other than the licensee will be eligible to build, own, and operate towers, and the existing sharing modality will be rolled back after implementing this guideline.

In our feedback to BTRC, we proposed the co-existence of the current model so that as an MNO we are allowed to build, own, and operate towers for our own use.

In general, we believe that in order to nurture a competitive business environment within a towerco regime, licenses should not be limited to two towercos, which is what the current proposal stipulates. Secondly, MNOs should have the option to either source towers from towercos or build their own. The decision should not be imposed upon the MNOs but rather be driven by commercial negotiations.

The biggest challenge will be meeting the rollout targets of the MNOs. In the future, new sites will be rolled out more in the rural areas and operators will have different location preferences. Some of the MNO requirements for tower construction may not be profitable for a towerco as the desired number of tenants may not be available.

There are other operational challenges, including the redundancy of around 4,000 technology employees who are currently working at the different MNOs.

TowerXchange: Looking ahead then, how will your grow the network? What will be some of the key drivers to growth? Does the country have enough coverage?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Currently more than 32,000 towers are in operation in the country. Grameenphone being the largest network provider covers 99% plus population of the country. Robi, after merger with Airtel, owns the largest tower base. However, the merged entity will decommission a handful of towers in 2017.

Currently all the operators in Bangladesh are providing 3G services. Internet penetration in the country is rising at a fast pace. The regulator has also recently announced its intention to issue 4G licenses in 2017 to all existing operators. As the operators will be serving more and more data hungry customers, the need for data coverage sites, indoor solutions, and transmission backhaul will be more prominent initially mostly in the urban areas.

Some of the drivers that will push for infrastructure growth in the country:

- Highly dense population

- Intense competition in the industry

- High economic growth in the country

- Exponential data requirement by mobile users

- Accelerating penetration of smartphones

- Operational excellence in managing costs and quality

- Operators’ pressure on fixed power and fuel costs

- Customised solutions e.g. in-building and cell sites solution

- Towers overlapping

- Public and regulatory pressure to reduce energy consumption and pollution

- Infra-sharing guidelines by the BTRC

TowerXchange: How does typical time to market for a greenfield tower build (including site acquisition, permitting and construction) compare to time-to-market for a co-location?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

For our own build, ideally 130 days for a ground based tower and 110 days for rooftop.

Whereas for co-location the best case of delivery is 15 days. After technical acceptance by both seeker and provider, the killer item is the NOC (no objection certificate) from HO/LO (house owner/land owner). Usually, rooftop sites will take longer.

TowerXchange: When it comes to operational efficiency, what are some best practices you are using and what would you like to see from managed service providers and towercos?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Some of the current practices in the industry right now include having fuel as a pass-through, periodic preventive maintenance at sites, and on-call support as and when required.

Moving forward, we would like to see managed service providers and towercos shifting to power and fuel as a fixed cost instead of the pass-through model. On the operational side of things, better control on site uptime and site-level performance, enhanced estate management and security, as well as monitoring of individual cell performance can help take things to the next level. More accuracy in consumables would also be nice.

TowerXchange: At this point in time, how can infrastructure providers/towercos better respond to customer needs and add value to its services?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Ultimately, the fundamental business model is focused on driving co-locations, however, we believe towercos can still focus on some of the following areas:

- Customer centricity

- Post operational support with high accuracy

- Introduce innovative power solutions with high back-up time

- Standardising tower height based pricing benchmark

- Aggressive SLA to win customers

- Reliability

- Reduce co-location timeline (feasibility analysis to site delivery)

- Minimise timeline for NOC collection fromHO/LO

TowerXchange: What do you see as some of the upcoming technologies and products that towercos may soon adopt? Why?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Going back to some of the drivers for growth, operators and towercos alike could be looking at solutions that are smaller, faster to deploy, easier to manage, and more cost-effective. Growing data demand from consumers combined with the need to optimise business performance will likely require some changes to the existing modus operandi.

We could be seeing more:

- In-building DAS

- Low cost solutions

- Cell-on-wheels (COW)

- Monopole

- Camouflage solutions

- Tower operating centre

- Green energy solutions

- 24x7 network availability

- Significantly less time-to-market

- Relationship building with landlords

- Active sharing

TowerXchange: Lastly, how do you see Grameenphone evolving its business to better adapt to market realities?

Md Mainur Rahman Bhuiyan, Director and Head of Infrastructure Business, Grameenphone:

Grameenphone has undertaken a strategic ambition to become a digital service provider by 2020. It aims to become the favourite partner in a customer’s digital life by digitalising the customer journey and core operations. In a bid to bring efficiency and reduce overall network operational costs in the industry, Grameenphone, the market leader in providing co-location sites, is working on setting new trends in passive infrastructure sharing by bringing flexibility in product modality and pricing. This is being done as part of the preparation to operate within a towerco regime.

Timeline of infrastructure sharing in Bangladesh

2003: Barter sharing started between CityCell & Aktel (now Robi)

2008: Barter sharing between CityCell & Warid (now Airtel that merged recently with Robi)

2008: Infra-sharing guideline issued by BTRC

2010: Grameenphone started formal infra-sharing under BTRC guideline

2013: edotco (towerco subsidiary of Robi Axiata) with NOC from BTRC started formal infra-sharing

2015: Banglalink started formal infra-sharing