There are very few countries in the Americas - and maybe globally - as complicated as Mexico, when it comes to its telecom infrastructure sector, and indeed telecom in general. Often perceived as a goldmine of opportunities by international investors, the reality of the country is far from rosy, and this is particularly true in the crowded build-to-suit sector. Here is an updated snapshot on the country’s dynamics.

ALTÁN Redes

The wholesale network project was awarded in November 2016 to ALTÁN Redes (ALTÁN) whose first target is to cover 30% of the Mexican population by March 31, 2018.

According to local sources, ALTÁN is offering a wave of opportunities for towercos with sizeable portfolios able to offer nationwide co-location opportunities. In fact, during this first phase, ALTÁN is very much focused on utilising existing infrastructure across Mexico City, Guadalajara and Monterrey.

At the moment, the major challenge ALTÁN is encountering is in the poor status of fiberisation across Mexico. So it comes as no surprise that American Tower has recently sealed the acquisition of KIO Networks, a Mexican infrastructure firm which owns more than 50,000 concrete poles and over 3,300km of fibre optic lines, primarily in Mexico’s key urban centres. The deal is valued at approximately US$500mn.

Hal Hess, American Tower’s EVP and President for EMEA and Latin America stated “We are pleased to close this transaction, which we expect not only to enhance the value of our existing tower portfolio in Mexico, but also to better position American Tower to capture a larger share of future urban 4G network densification efforts and the eventual rollout of 5G."

Various sources report that while for now ALTÁN is only working on co-locations and that build to suit (BTS) could be only sporadic throughout 2018, there are expectations for the volume of BTS to pick up in 2019. Especially since ALTÁN is working ahead of its planned 2018 goals and could start phase two of deployment (50% of the added population and 50% of the Pueblos Mágicos) as early as January 2018.

The carrier landscape

There is general consensus that the mobile market is improving both in terms of ARPU and overall financial performance, but this hasn’t led to a positive shift in their investment cycles yet. In fact, carriers are still refraining from considerable network capex and neither AT&T nor Telefónica have been announcing any large BTS assignments. On the other hand, Telesites has been working on a backlog of orders from Telcel while the operator is preparing its 2018 deployment plan.

AT&T has not announced any major BTS programme for 2018 and according to some sources, American Tower is the only towerco currently picking up small orders. And some commentators suggest that the quality of service AT&T is offering is not up to par with Telcel yet.

Telefónica has recently launched an RFQ for approximately 150 rings for new rooftops to be deployed in 2018. And local sources suggest that some aggressive bidders drove prices down considerably in what has been defined as “another punch to the BTS business model.”

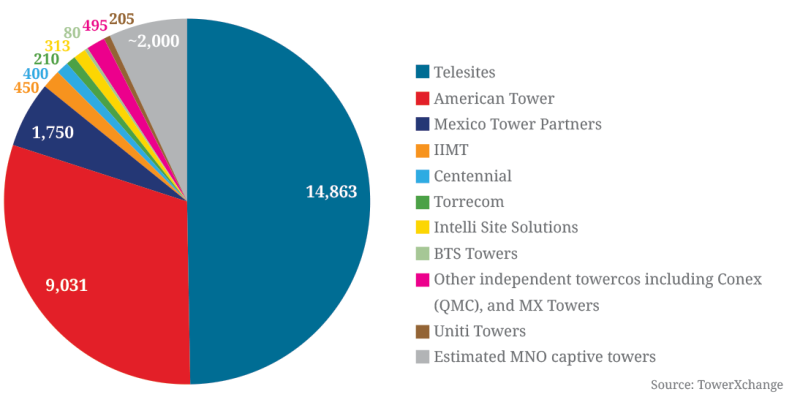

Mexico - Estimated tower count 29,797

The Zero Rate

In the meantime, the Instituto Federal de Telecomunicaciones (IFT) has withdrawn the ban imposed on Telcel not to charge fees for termination services on its network. The IFT established a MXN0.029 (US$0.002) fee per minute for calls terminating on Telcel’s network. And Telcel will pay US$0.01 as interconnection rate to terminate calls on its competitors’ networks.

The Zero Rate was one of the initiatives imposed on Telcel to improve competition among telecom players in Mexico. However, as recently noted by TeleGeography, to date Telcel still claims 65.6% of the Mexican mobile market, with Telefónica at 22.7% and AT&T at 11.7%.

Implications for the future

TowerXchange has been reporting for some time now about the possible wave of consolidation that could hit the Mexican tower market and bring some rationality to the fragmented sector. However, to date no transaction has taken place and the only rumoured deal involves Canadian towerco Tower One and an unnamed entity, although some sources suggest that the deal might actually entail the transfer of MLAs that the seller holds with AT&T, rather than exiting towers.

AT&T has been assigning small orders to a wide array of towercos in 2016 and this has resulted in pockets of assets (5-10 towers) being owned by dozens of local towercos who aren’t always able to sustain themselves while waiting for new orders. How long can these companies stay in business without new BTS orders though?

We can only wait to see what the future might hold for Mexico’s BTS sector while larger towercos are indeed starting to see the benefits of ALTÁN and reporting healthier volumes of co-location. One thing remains clear though; Mexico’s telecom network is still far from complete in terms of coverage and capacity, and ALTÁN could represent a breakthrough if they are able to attract traditional carriers and MVNOs onto their network with the transparent and non-discriminatory pricing structure it has been advertising. And while this isn’t good news for BTS towercos, it could be the change that Mexico needs and has been waiting for.

Did you enjoy what you were reading?

As of 20 November 2017, TowerXchange will be moving to a subscription model for all our of non-towerco, non-MNO readers. Moving to a subscription model will allow us to continue to provide you with the business-critical information you have come to rely on - but ensuring it is supplied more frequently, in a variety of online and offline formats, so you can access it in whichever way suits you best - and allows us to cover more of the areas that mean the most to your business.

We hope you will join us. Subscribe today to continue to receive access to the TowerXchange website and journal.