The substantial equity stakes retained by MNOs in many of the largest telecom tower companies in China and India means pricing and business models are calibrated to liberally share the efficiencies of infrastructure sharing.

China Tower Company (CTC) has set a pricing scheme that averages around US$325 per month, 30% lower than the ~$500 tenants pay in India. While the cost of materials and labour, and the sheer scale of the Indian and Chinese tower markets, account for some of the difference, tower markets in the rest of the world are calibrated more toward more commercial, value-creation driven objectives, yielding substantial shareholder value and attracting the participation of the private equity and debt markets – in such environments, pricing can be 2-4x the level seen in China and India.

In markets where lease prices have had previously held up above US$1,000, independent developers offering discounted lease rates and valuable concessions are attracting a significant volume of new build business, but are these disruptive new entrants adding volume and value, or are they compromising the structure and investibility of the tower industry?

Whilst the August 2016 edition of the TowerXchange Journal provides our regular updates of market structure and industry news in CALA, Europe, Asia, Africa and the Middle East, in this edition we also contrast the business models of 42 of the world’s leading towercos, examining the distinctive origins of the tower industry in each region. The contrast informs lease pricing comparisons; we examine CTC lease pricing and consider the implications for valuation; Bharti Infratel Chairman Akhil Gupta tells explains steps taken to create lease price parity in India; we examine how the entry of discount independent developers has resulted in a two tiered tower market in Myanmar; and SBA Communications’ David Porte challenges whether the pricing and contractual concessions granted by independent developers in CALA may come at the expense of investibility.

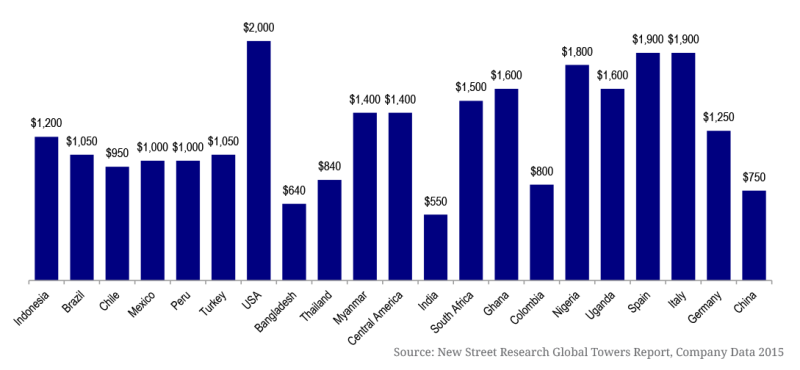

New Street Research offers an interesting comparison of lease rates worldwide, albeit the bar chart shown on this page was compiled prior to CTC pricing leading to a substantial downward adjustment of the anchor tenant rate in China. Spencer Kurn of New Street Research shares the first of what we hope will become a regular guest column, combining co-location growth with lease pricing and other components of tower economics to compare return on investment in towers worldwide.

New Street Research comparison of anchor tenant rents across regions (USD per month, exc pass-through revenue)

TowerXchange wish to emphasise that differences in lease rates aren’t a product of towerco greed or weakness; they are usually the rational output of market conditions such as the site acquisition and capital cost of building a new tower, and the operational costs. The most important inputs determining anchor tenant rates are the priorities of the MNO selling the towers: a focus on maximising cash released leads to a high lease rate, a focus on reducing opex at the expense of upfront cash leads to a low lease rate.

The pricing of additional co-locations, and any discounting thereof, is at least as important as the anchor tenant rate in determining value. Another critical factor are escalators, sometimes fixed but often linked to CPI (inflation). New Street Research highlights escalators between 0.9% and 7.2% per annum.