In April 2015, Eaton Towers announced the first tower transaction in MENA, striking a deal with Mobinil (now Orange) for the sale and leaseback of over 2,000 Mobinil towers. Fast forward to July 2016 and the deal is off, with Orange failing to extend the longstop date for completion of the transaction. TowerXchange take a look at the Egyptian market and details surrounding the cancelled transaction to examine how the independent tower industry may now evolve in Egypt.

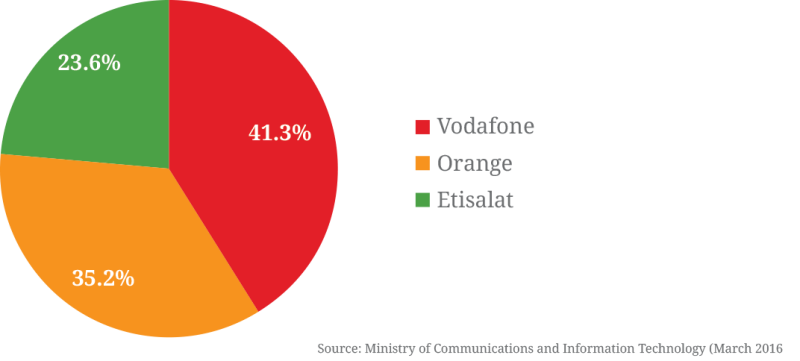

Egypt is one of MENA’s largest mobile markets with 93.7mn mobile connections and mobile broadband penetration standing at 42%, up 28% on 2014 figures (GSMA intelligence). There are currently three tier one operators active in the market; Orange, Etisalat and Vodafone. Vodafone leads the market with 41.3% of total mobile subscribers, Orange has 35.2% and Etisalat 23.6% (figure one).

Population coverage stands at 99% and 3G deployment commenced in 2007. Mobile broadband penetration stands at 42% as of Q4 2015, up 28% on 2014 figures (GSMA intelligence).

Figure one: MNO market share in Egypt

4G licenses

The Egyptian regulator, NTRA, is in the process of auctioning 4G licenses, having offered licenses to the three MNOs as well a fixed line incumbent, Telecom Egypt. Kuwaiti based Zain has also reportedly expressed an interest in obtaining a 4G license in the country. The three MNOs and Telecom Egypt had been given until the first week of August to respond to the offers and whether they wish to proceed with obtaining a license.

On Sunday 7 August, the board of Telecom Egypt gave its final approval for plans to buy a 4G license and as such, the fixed line player becomes Egypt’s newest mobile network operator. Orange, Etisalat and Vodafone had expressed concerns regarding the amount of spectrum being made available in the auctions, as well as the regulator’s stipulation that a portion of the 4G license fees be paid in US dollars. The regulator had previously refused to back down on the two issues, however as the deadline approached, the NRTA announced that it had opened talks to make available further frequencies in a bid to alleviate the MNOs’ concerns. At the time of going to press we await feedback from each of the MNOs as to whether the offers of 4G licenses have been accepted.

Egypt’s tower industry and infrastructure sharing

There are 19,000 - 20,000 towers in Egypt with a roughly even split between each of the MNOs. Tower builders, HOI-MEA also possess a portfolio of 60 towers in the country, (targeting 500 by the end of 2017) whilst their competitors, Mobiserve, Alkan and EEC also possess licenses to provide passive infrastructure sharing services in country, although have to date, not chosen to retain assets.

There has been some bilateral infrastructure sharing between MNOs in the Egyptian market, however tenancy ratios reportedly sit much closer to 1 than 1.5. Most of the towers built in Egypt are thought to be relatively robust structures and so capable of carrying two or three tenants and so additional co-locations are thought to require only minor structural modifications. Whilst the co-locating on existing infrastructure is an option to densify 3G (and commence 4G) deployment, Egypt has more SIMs per tower than any other country in MENA (4,690 versus the regional average of around 2,500) and so there is significant potential for new build in the market.

Rooftop sites are prevalent in the major cities, with over 90% of Cairo’s sites being rooftop structures. These structures are inherently less suited for co-location and so the much of the opportunity for increasing tenancy ratios is outside of the major metropolises.

Whilst the grid infrastructure in Egypt is extensive, grid interconnection processes are extremely slow. With such long timelines to get a license to secure power from the authorities, a surprisingly high proportion of sites in Egypt are off-grid. Many sites in the country are reliant on diesel generators, with the high load on some sites resulting in as many as three generators being required per site. Due to generous fuel subsidies in Egypt, diesel prices are significantly lower than in other markets and as such the business case for alternative energy at sites is reduced. Some solar-hybrid trials have been completed in the country, particularly in the Delta region, and with a programme being introduced to reduce fuel subsidies, it is likely that renewables will start to play a bigger role.

April 2015: Orange announce the sale and leaseback of 2,000 towers to Eaton Towers

In April of 2015, Orange (then trading as Mobinil) announced the sale of their stake in the company’s tower subsidiary, Egyptian Company for Mobile Tower Services (ECMTS) to Eaton Towers for 1 billion Egyptian pounds (US$131.15 million). The agreement encompassed the purchase of approximately 2,000 towers (around one third of Orange’s total tower count in the country) with a 15-year leaseback contract for the operation and maintenance and also for the additional build-out of new sites. The towers purchased by Eaton were in three geographic areas: Delta, Upper Egypt and Red Sea and excluded Orange’s rooftop sites in Cairo.

Eaton subsequently entered negotiations to acquire a second tranche of Orange towers, although no deal was announced.

Eaton shore up their technical capabilities; the Egyptian Pound devalues

Following the agreement, Eaton Towers and Orange worked on the technical handover of the towers, with Eaton beginning to shadow operations from January 2016. 13 staff were recruited from Orange into Eaton’ Egyptian team whilst Karim El Azzawy (formerly of Egyptian managed service provider, Mobiserve) was appointed as the country manager.

In March 2016, the Central Bank of Egypt devalued the Egyptian Pound by almost 13% as they shifted their exchange rate policy in a bid to boost foreign reserves and increase competitiveness. As per the signed agreement between Orange and Eaton, the devaluation meant a revision to the commercial terms of the deal, with further devaluation and revisions expected.

July 2016: An absence of regulatory approvals and termination of the transaction

On the 21 July, the longstop date laid out for completion of the transaction, Orange Egypt was still awaiting certain regulatory approvals relating to the change of control of ECMTS, the separate company into which they had transferred the 2,000 towers for Eaton to acquire.

With the prerequisites and conditions necessary for completion of the deal not met, the Orange Egypt board made the decision to not extend the deadline and as such terminated the agreement

Influencing factors and potential motivations behind the cancelled deal

Discussions surrounding a potential sale of Orange Egypt’s towers began back in 2013 and since then there have been significant changes in management at both the opco and Orange group level. Key architects of the deal have left Orange Egypt (Kais Ben Hamida, then CFO), or will leave this month (Yves Gauthier, CEO); and in Paris a new Group CFO and CEO of EMEA have been appointed. Such changes in management are likely to have caused certain delays in the finalisation of all the terms and conditions of the agreement.

Secondly, the National Telecom Regulatory Authority is in the process of awarding 4G licenses with a deadline of the first week of August being laid out for MNOs to respond to the offers from the regulators. Orange Egypt announced that it had been asked to pay EGP3.54bn for a 4G license but, by the 21 July deadline laid out for the Eaton Towers deal, had yet to reach a decision on whether it would accept the offer. The regulator may well have felt that no approvals be given to Orange until discussions around the 4G license were resolved.

Thirdly, it may be that Orange are using this as a negotiating tactic to improve the commercial terms of the deal. It wouldn’t be the first time that an operator has followed such a strategy, with Airtel having revived some of its cancelled tower deals with better terms. At an average cost per tower of US$65,575 (versus the sub-Saharan African average of US$133,438), the deal value looked very low, however TowerXchange understood that Orange Egypt had structured the deal to focus more on reducing opex than raising maximum capital which would account, for the difference.

So what’s next?

Eaton Towers have confirmed that they are still committed to the Egyptian market. “Eaton Towers still regards Egypt as a market ready for independent tower companies” says CEO, Terry Rhodes in discussion with TowerXchange. “The imminent rollout of 4G, together with the economic and political changes which have made US dollars very scarce mean the operators will be under financial and operational pressure to expand their networks. It would be enormously beneficial for this expansion to share infrastructure”

“Eaton Towers shareholders believe in Egypt” continued Rhodes, “Indeed DPI, Eaton’s original institutional shareholder closed its first deal in Egypt only last month, with a US$35m investment in appliance retailer B.Tech. Therefore we will continue our endeavours to enter the Egyptian market.”

Orange’s strategy regarding the outsourcing of towers is mixed (table one), having agreed the sale and leaseback of 300 towers in Uganda to Eaton and entered into a MLL arrangement with IHS in Cameroon and Cote d’Ivoire. Prior to the sale of Telkom Kenya to Helios Investment Partners, Orange had also entered into a MLL arrangement with Eaton in Kenya, a deal which was subsequently cancelled, and talks of Sonatel’s towers (Orange’s opco in Senegal) coming to market have now been discontinued.

Orange has acquired a towerco relationship in the DRC following the acquisition of Millicom’s opco (which had previously sold towers to Helios) and so further experience of managing an outsourced network will be gained from the unit. The company is believed to have a preference towards keeping an active role in the management of their towers and has also embarked on significant projects to reduce energy costs across their networks, exploring alternative mechanisms beyond the outsourcing of towers to reduce network TCO. With a new group CFO and a new CEO of EMEA in place it will be interesting to see how Orange’s attitudes to tower outsourcing evolve and whether the transaction in Egypt could be revived.

Table one: A history of Orange’s tower transactions in sub-Saharan Africa

Both Eaton Towers and Orange will be attending the 4th Annual TowerXchange Meetup Africa & Middle East alongside other key stakeholders in the Egyptian tower industry. The Meetup will be held on 19-20 October 2016 at the Sandton Convention Centre.