With the reduction in uncertainty in the Myanmar tower market comes a reduction in risk, and a commensurate increase in investibility. Towerco consolidation has only recently begun, but the structure of the Myanmar tower market is increasingly clear, and TowerXchange expect three towercos of scale to emerge. Likewise, the structure of the mobile market is becoming clear; MPT has stood its ground; Telenor has grabbed impressive market share; Ooredoo has continued to differentiate as a first mover in next generation technologies; and now Viettel has been selected as the joint venture partner for the fourth operator.

Estimates suggested 17,300 towers would be needed to achieve the Myanmar MCIT’s coverage targets by the end of 2017. Myanmar’s tower stock had grown to ~10,750 towers at time of press. There is organic growth for Myanmar’s towercos, but there is also tenancy ratio growth; the tenancy ratio of mature portfolios ranges from 1.35 to 1.9, suggesting a healthy culture of infrastructure sharing and a growing need for capacity as subscriber numbers continue to grow impressively. The Myanmar tower rollout seems broadly on track, but let’s take a closer look at the structure of that market.

Who are Myanmar’s operators and what has been their tower strategy?

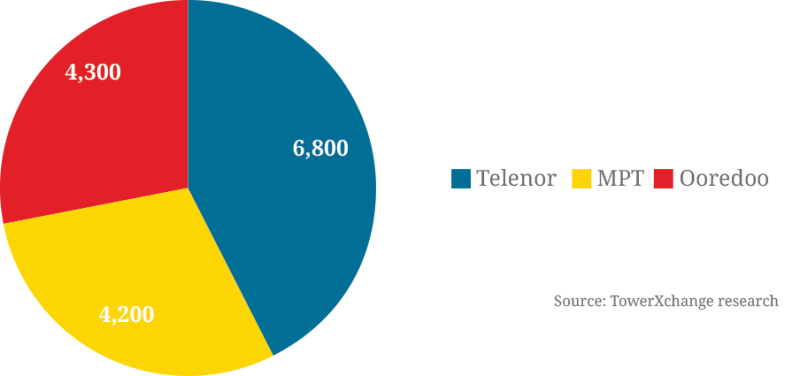

Few commentators would have predicted that State-backed incumbent MPT (Myanmar Post and Telecommunications) would have retained their market leadership two years after the licensing of two international competitors but, backed by KDDI and Sumitomo, MPT has a 45% share of subscribers with over 20mn.

Investors KDDI and Sumitomo intend to invest a total of US$2bn in their Myanmar joint venture partner MPT, with a US$1.6bn network infrastructure investment announced this time last year, which was to drive their base transceiver station count from 2,000 to 5,000. While MPT are not believed to have dramatically increased their captive tower count, which continues to be rolled out by Huawei, most of the Myanmar towercos report healthy lease up, which we estimate totals over 1,500 co-locations from MPT, suggesting MPT is closing in on their target.

Of the two international license holders, Telenor has achieved the fastest subscriber growth in Myanmar, racing to just under 17mn subscribers in two years. Telenor has maintained their reputation as a tough, disciplined and single-minded negotiator with towercos, playing off Apollo and IGT as their go-to towercos of scale, while driving deep discounts with Eco Friendly Towers and recent entrants OCK. Telenor remains broadly on track with their rollout plan, having lit 5,831 towers by the end of Q216 – all independently owned – with a target to reach 7,000 by year end 2016, and as many as 13,000 sites to achieve solid nationwide voice and data coverage.

Having launched a month ahead of Telenor in August 2014, Ooredoo has fared less well in the battle for subscribers, achieving 8.2mn subscribers by the end of Q216. While it initially appeared that Ooredoo was courting the higher value customer with Myanmar’s first 3G then first 4G service, ARPU fell 35% between Q215 and Q216, while management changes and a slow down in new tower build in the first half of 2016 suggest the operator is changing strategic direction. Ooredoo currently has ~3,800 sites. Like Telenor, Ooredoo has used third party towercos for their rollout, but changed strategy in 2015, reverting from an initial preference to retain power assets to now requiring that towercos provide tower+power.

While they have yet to break ground, soon-to-be licensed fourth MNO Viettel has pledged to invest US$1.5bn in the construction of a 3G network, with the aim of achieving 95% population coverage within three years. Viettel has a creative approach to making more marginal locations economically viable for the provision of mobile coverage. Viettel successfully and rapidly deployed low cost networks focusing on underserved rural areas in Mozambique, Cameroon and more recently Tanzania. The Vietnamese military-backed operator has formed successively deeper partnerships with towercos, and has already been using the test sites of Myanmar’s towercos, who will be hopeful that Viettel accelerate their rollout and achieve volume and capacity at launch by substantially leveraging co-location.

Myanmar mobile subscriber growth by MNO over the last year

Viettel owns a 49% controlling stake in Myanmar’s fourth MNO, with the balance shared among a consortium of local stakeholders which includes Star High Public Company, itself owned by Myanmar Economic Corporation (MEC), which also owns MECtel. Viettel will reportedly have access to assets including 1,000 towers and 13,000km of fibre, as well as whatever remains of a reported subscriber base of 3.8mn before MECtel’s MNO play was discontinued.

Estimated total number of sites in each MNOs network (inclusive of co-locations)

Who are Myanmar’s towercos and how are they financed?

We would divide Myanmar’s seven towercos into three groups; towercos of scale (IGT, Apollo and edotco), towercos competing on price (EFT and OCK), and towercos seeking an exit (PAMEL and MIG – with Digicel MTC already departed).

Between them, these seven towercos have built over 7,000 towers to date, with only MPT building their own sites through Huawei.

Currently Myanmar’s largest towerco with around 2,400 towers, Irrawaddy Green Towers (IGT) has the distinction of being Myanmar’s only towerco to date to have secured substantial build contracts from both Ooredoo and Telenor. Ayad Chammas serves as CEO. IGT has declared intent to build 5,000 towers in Myanmar, spending ~US$490mn. IGT is part of ASEAN Towers, which also owns Golden Towers with 350 sites in Vietnam. IGT has investment from by Alcazar Capital, EPC Investors, M1 Group and local Myanmar company Barons Telelink. In December 2015, Dutch DFI FMO arranged a US$122mn syndicated loan for IGT.

Apollo Towers Myanmar, which has around 1,800 completed towers, also recently raised development finance, having started to draw down a US$250mn loan from OPIC. Apollo’s Chairman is former Eaton Towers Founder and Orange CEO Sanjiv Ahuja, and is a joint venture between Ahuja’s Tillman Global Holdings, TPG and MIL (Myanmar Investments International Limited). Philippe Luxcey is CEO.

edotco is the third of three Myanmar towercos of scale, having spent US$221mn acquiring Myanmar Tower Company (MTC) from Digicel. MTC built 1,250 towers for Ooredoo in phases one and two of the rollout. While MTC did not own the power assets at the sites, which were retained by Ooredoo, edotco will provide a full tower+power service. Digicel MTC CEO Oliver Coughlan stayed on to become edotco’s Country Managing Director for Myanmar, although he is currently transitioning to a Group COO role with Vijendran Watson taking the helm in Myanmar.

edotco has a footprint of 16,450 towers across six Asian countries, and is currently 100% owned by Axiata, although their stake may be diluted by third party investors or IPO in the medium term. edotco CEO Suresh Sidhu has stated intent to build or buy 5,000 towers in Myanmar, and the company’s balance sheet makes them a strong contender to acquire further tower portfolios that match their investment thesis.

edotco’s next acquisition target may be Pan Asia Majestic Eagle Limited (PAMEL, sometimes referred to as Pan Asia Towers or PAT), whose 1,250 towers were built for Ooredoo in phases one and two. The portfolio is almost a mirror image of the Digicel MTC towers. PAMEL has management DNA in common with Indonesia’s Protelindo, but remains a distinct entity. In 2014 PAMEL secured US$85mn in financing from a consortium of five banks: DBS, ING, OCBC, Standard Chartered and Sumitomo Mitsui. PAMEL remains the last towerco in Myanmar operating the ‘steel and grass’ business model, but that may change with the change in ownership.

Breakdown of ownership of the 10,750 towers TowerXchange estimates have been built to date in Myanmar

Vendor finance was critical in the early days when international investors were cautious to invest in Myanmar, but climbing tenancy ratios, healthier cash flow, and an influx of capital means Myanmar’s towercos of scale are now less dependent on vendor finance.

A subsidiary of diversified Myanmar conglomerate Young Investment Group, Eco-Friendly Towers (EFT) has built over 300 towers, most in the Northern States, from a contract for 700 from Telenor. Young Investment Group Chairman Thiha Aung has represented EFT at a past TowerXchange Meetup Asia, while his wife is believed to be responsible for day to day management of EFT.

Myanmar Infrastructure Group (MIG) is backed by Singapore Windsor Holdings. MIG has been hard-hit by Ooredoo’s slow down in build, having built around 100 of an originally contracted 500 towers. With the Group exploring opportunities in rental cars and other markets in Myanmar, they are believed to be open to offers for their tower portfolio. Mark Bedingham is CEO of MIG.

OCK is the newest entrant to the Myanmar tower market. The company boasts impressive credentials as a listed telecom turnkey solution provider in Malaysia, and has ambitious plans to form a pan-Asian towerco, including targeting 3,000 towers in Myanmar. Telenor downwardly negotiated OCK’s lease rate, believed to be sub-US$1,000, and awarded a contract for 920 towers, of which around 50 are believed to be complete at time of press. OCK’s Myanmar subsidiary raised a syndicated loan of US$40mn from OCBC Bank, Malayan Banking, United Overseas Bank and Bangkok Bank’s Yangon branches. Terence Lee runs OCK’s operation in Myanmar, while Sam Ooi is Group Managing Director.

Pressure on prices

There has been little uniformity in lease rates in Myanmar since the outset. Whilst there was significant variation in pricing initially, the country’s original four towercos have coalesced within a fairly narrow range of lease rates. However, the aggressive price negotiations of Telenor has created a tier of discount towercos.

OCK say they will invest US$75mn to build the 920 towers Telenor has contracted; that works out a little over US$80,000 per tower. That’s a little below the current average build cost of a tower in Myanmar (around US$100,000), but build cost is gradually coming down as a function of volume, and much depends on the cost of energy equipment. With OCK reportedly charging a lease rate as little as US$900 or US$920pcm, inclusive of power, some competitors had suggested OCK would have to deploy low cost DGs and batteries to minimise capex. However, OCK’s recent order for 80 premium, integrated DG+battery hybrid eSites from Flexenclosure suggests OCK intend to deploy equipment of a similar standard to other towercos on at least some sites. There are already over 1,200 eSites deployed in Myanmar.

In an exclusive interview featured within this Journal, TowerXchange asked OCK Group Managing Director Sam Ooi how they planned to sustain their competitive price point. “OCK is a full turnkey solutions provider,” said the MD, “and we are able to leverage our expertise from other countries into Myanmar, resulting in a lower cost to build and maintain towers. These benefits are passed on to our valued customers.”

Whether it’s OCK, EFT or any other towerco offering towers at a discounted lease rate, their greatest challenge will be creating a scalable tower business in Myanmar. Coming in 30%+ cheaper than the competition might drive volume, but in order to meet Telenor and Ooredoo’s exacting quality standards and SLAs, the cost of a tower is the cost of a tower. At such a low lease rate, discount towercos will have to drive to a healthy tenancy ratio quickly to create the necessary cashflow. Will the entry of Viettel, and resultant urgency generated among incumbent operators, drive tenancy ratios close to two within the next 12-18 months?

The reducing risks of investing in Myanmar towercos

What are Myanmar’s towers worth?

With the PAMEL and MIG portfolios reportedly coming to market, it should be noted that not all towers and towercos are created equal in Myanmar; just because edotco paid US$176,800 per tower for Digicel MTC’s 1,250 towers does not mean all Myanmar towers will change hands for a premium of that magnitude.

The usual valuation rules apply: the value of a tower is as much to do with the paperwork (particularly the permits and the commercial terms defined in the MLA - Master Lease Agreement) as it is to do with the attractiveness of the location and the quality / capacity of the structure. The value of a tower is not just about Tower Cash Flow (TCF) today, itself a product of lease rate, tenancy ratio and opex costs; it’s more about potential future TCF.

The first and much of the second phase of the Myanmar tower rollout were naturally concentrated in the country’s three most densely populated cities: Yangon, Naypyidaw and Mandalay, as well as the transport routes between them. For example, PAMEL have built 1,250 robust, phase one towers and leased them up to a tenancy ratio reported to be around 1.8, with a healthy lease rate in excess of US$1,700pcm. These towers are likely to be sought-after by Viettel when they begin their rollout. Expect PAMEL’s towers to attract a healthy premium when they come to market.

As the rollout extends deeper into rural areas, often beyond the reach of Myanmar’s finite paved road network, search rings call for towers to be built in less accessible locations, often well beyond the reach of the grid. Mature towercos will sometimes reject sites in such remote areas, wary of the cost of site acquisition, the complexity of the build, elevated opex costs as a function of energy logistics, and reduced co-location potential. However, towercos coming later to market may be under more pressure to accept such locations as they seek scale. The near-term and potential future TCF from those sites may not match that of Myanmar’s phase one and two towers, indeed if the MLA is not drafted smartly and the location is undesirable, some towers may barely be worth the capital deployed to build them. As we said at the outset; not every tower in Myanmar is worth the US$176,800 per tower edotco paid for a portfolio which now has a tenancy ratio of 1.9; towercos and their investors must be wary of building towers with a much lower glass ceiling on tenancy ratio, which may be worth less than US$100,000.

Forecasting the future of Myanmar’s tower market

By the end of 2017, Myanmar will have the targeted 17,300 towers, around 4,000 of which will remain MNO-captive on MPT and Viettel’s balance sheets. The remainder will be concentrated primarily in three large towerco portfolios – around 5,000 towers built and rolled up by edotco, plus a further 8,000 towers built by OCK, IGT and Apollo, at least one of which will have received an offer they can’t refuse by then and exited. Who are potential buyers? edotco of course, while American Tower are known to have considered entering the Myanmar market in 2015, but the level of risk may now be more attractive to their investment palette.

Newest entrants OCK have been bullish about their plans to rollup a pan-Asian portfolio of towers – indeed they recently announced the acquisition of 1,938 towers in Vietnam for US$50mn. OCK are the wildcard in our forecast; if they can build at speed and drive to their targeted 3,000 Myanmar towers at their discount price point, they are going to prove popular with all four Myanmar MNOs.

TowerXchange think there is room for two to three towercos of scale in Myanmar in the long term, perhaps fed by one or two localised or discount towercos that may ultimately become “build to flip” plays.

The Myanmar tower market today looks dramatically different from a year ago. Many risks have receded and, while there remains some pressure on lease prices from aggressive buyers and discounters, Myanmar’s three towercos of scale are holding firm at a price point that enables them to attract international investment, and to build quality assets in a timely manner, fulfilling the ambitious visions of Myanmar’s three-going-on-four operators, and meeting the insatiable appetite of Myanmar’s citizens for mobile services.