A developed market towerco which owns and operates just ‘steel and grass’ is a fundamentally different entity from an emerging market towerco that might manage towers, real estate and power. Towercos also grow in different ways; some focus on organic growth, others on inorganic growth; buying and leasing back towers from MNOs, or rolling up existing towercos. Then you have different assets on towerco balance sheets; some focus purely on macro telecom towers, others also make a significant proportion of their revenue from broadcast clients, while some are diversifying beyond macro towers into microcells, small cells, DAS and fibre. How did these business models evolve?

Whether you want to invest in a towerco, partner with a towerco, or sell to a towerco, it’s useful to know what breed of towerco you are dealing with.

Three fundamental towerco business models evolved in parallel – build, buy and carve-out – and spawned a number of variants designed to meet specific local market needs.

The US independent towerco model evolved as tower builders, media and real estate entrepreneurs anticipated the investibility of long term recurring cash flows from leasing telecom structures, and started buying, building and retaining towers. When the US model was exported to SSA the model was refined to relieve African MNOs of their principal operational headache: power. Meanwhile, in Asia a third parallel carve out model evolved where MNOs retained a significant stake in the towercos. The towerco business model has mutated once again to integrate Europe’s broadcast assets, and to incorporate the decommissioning of the continent’s parallel infrastructure. Then just last year, China implemented it’s own brand of co-construction and infrastructure sharing, with the creation of State-owned, 1.55mn site giant China Tower Company.

How it all started in the US

The tower industry as we know it started in the mid nineties in the United States when, almost simultaneously, Steve Bernstein Associates (now SBA Communications), Castle Towers (now Crown Castle) and American Radio (now American Tower) all came up with the idea of unlocking the value of towers by selling space to multiple tenants. Steve Bernstein Associates transitioned from tower builder to tower owner – you can learn more about their story in TowerXchange’s interview with SBA President and CEO Jeff Stoops.

American Radio, as the name suggests, originated in a deal to acquire a radio station that had multiple tenants on their tower: Steve Dodge and Jimmy Eisenstein recognised the tower represented an investible, scalable source of long term recurring lease revenue. By 1998 American Tower was IPO’ed and spun out of American Radio, scaling to over 15,000 towers by 2001.

Meanwhile, Ted Miller was playing golf at Castle Pines when the notion of moving from commercial real estate into telecom real estate first crystalised with the words “Castle Towers” written on the back of a napkin! Ted, later joined by David Ivey and Chuck Green among others, raised capital from the likes of Centennial Ventures and Berkshire Partners, and started buying towers in the US and UK, including a portfolio of several hundred towers from Crown Communications, from which would come the ‘Crown Castle’ moniker of today.

Crown Castle announced the first large tower transaction in December 1998 when they acquired over 1,400 towers from Bell Atlantic, the operator smartly retaining a stake in the joint venture, in a deal valued at US$650mn. Other U.S. operators figured “if it’s good enough for Verizon, it’s good enough for us,” and four further tower transactions quickly followed. Crown Castle listed in 1998 and, until the technology bubble burst, the birth of a new infrastructure asset class proceeded without undue complications.

Only the US tower market has been through a technology stock devaluation like the carnage of 2002-3. Frankly, the markets misdiagnosed towercos as a technology play rather than an infrastructure play, but many over-leveraged tower companies would not survive the downturn. Even Crown Castle, American Tower and SBA lost well over 90% of their value.

How did they survive? We’ll leave SBA CEO Jeffrey Stoops to tell the rest of the story: “We knew that because each tower is a business in its own right, we could hive off towers as necessary to raise enough money to pay off enough of our debt and avoid bankruptcy... We sold off 800 towers west of the Mississippi and used the proceedings to pay off our bank debt, which was the most troubled portion of our capital structure. Then we began a long and steady climb to reposition ourselves. We traded debt for equity, saw the market slowly improving, refinanced our business and grew our cash flow day after day. And we learned a valuable lesson! One of the reasons why this business is so attractive is that it’s very leverageable but too much debt is simply not sustainable, no matter which industry you are in… Oh, and three years later to the day we bought back all of those 800 towers!”

Few towers transacted in the US between 2002 and 2007, but fast forward to today, and the US is home to the world’s most valuable, most leased up towers. Over 80% of towers are owned by towercos, the majority consolidated into the portfolios of Crown Castle, American Tower and SBA Communications, with a handful of mid-tier consolidators led by Vertical Bridge, and a long tail of over 100 independent developers.

The American independent tower model is credited with accelerating wireless connectivity and adoption; where once the US lagged other markets, it is now a leader.

Rollup, rollup...

There’s another U.S. story which starts up a little later; Marc Ganzi at Global Tower Partners and his backers at Blackstone, led by Ben Jenkins, concentrated on what we now know as the rollup business model.

Rollup towercos concentrate on consolidating the fragmented ecosystem of privately owned towers, from “Mom and Pop” landlord driven businesses to smaller build-to-suit centric towercos. While most towercos of scale rollup opportunistically, the rollup specialists will spend countless long hours on hundreds of small transactions per year, and will often have the unenviable task of “cleaning up” these assets to build a portfolio with a consistent high standard.

Does rolling up work? GTP was certainly a success story; they rolled up 15,700 mostly North American towers and sold them to American Tower for US$4.8bn in 2013. This inspired not just one but two sequels: Ganzi and Jenkins’ latest rollup venture Digital Bridge now has over 5,000 towers across the Americas, while members of GTP’s hard grafting M&A team, led by Dagan Kasavana and Natalya Kashirina, have rolled up over 2,000 towers, also in the Americas, within Phoenix Tower International, which has attracted Blackstone to once again back the venture.

Refining and exporting the business model to Central and Latin America and Sub Saharan Africa

The US towercos crossed the border into Latin America, where in some countries they are able to use a very similar business model, using their US MSAs as a template in some countries; “because we were the first to enter in the region, we were able to shape contracts the same way we did in the U.S., which obviously was a benefit”, said SBA CEO Jeffrey Stoops in an interview later in this TowerXchange Journal.

There were some first movers, but the deal flow crescendoed between 2010 and 2014, culminating in today’s situation where around half of the towers in CALA are owned by independent towercos, including the majority of towers in Brazil and Mexico.

But when pioneers brought it to SSA, the towerco business model had to be fundamentally refined: the towerco would become a powerco. As much as 50% of MNOs’ opex in SSA is derived from energy and energy logistics – if Africa’s MNOs were to turn over their prized network assets to towercos, those towercos would have to take on the complex (and leaky!) diesel supply chain.

Led by former Crown Castle CFO Chuck Green at the helm of Helios Towers Africa; former Orange and Celtel CEOs Sanjiv Ahuja and Terry Rhodes with Eaton Towers; and a footprint extension of American Tower under the leadership of Hal Hess, Stephen Harris and Pieter Nel; the colonisation of Africa would also give rise to IHS, the most recent in a long tradition of tower build and service companies to make the successful transition to asset ownership and, in the case of IHS, market leadership. Under the guidance of Issam Darwish and his team, IHS’s portfolio now consists of more than 22,900 towers, including the majority of towers in Cameroon, Cote d’Ivoire, Rwanda, Zambia and Nigeria – Africa’s largest mobile market.

Evangelising the independent tower ownership business model to MNOs and investors was a painstaking process but, like in the US, when the first tower transactions were announced in 2010 (Helios Tower Africa in Ghana, DRC and Tanzania; HTN, IHS and SWAP in Nigeria; American Tower C in South Africa and Ghana; Eaton also in Ghana), the floodgates opened and over the subsequent six years Africa’s towercos have deployed around US$5bn rolling up almost 50,000 towers, representing 42% of the stock in SSA.

Like CALA, tower transaction deal flow is slowing in SSA as most of the investible towers have been acquired.

Meanwhile in India…

The Indian tower model evolved along two axes: a commercial, pureplay independent tower model exemplified by American Tower and Tower Vision, and an MNO-led model, exemplified by Indus Towers and a host of MNO-captive carve-outs. The strength of the latter community, and of the influence of MNOs, means many MLAs in India are structured to incentivise co-location by sharing savings. The Indian market also has remarkably consistent lease prices (~Rs 32,000, around US$500).

Tower sharing in India had been limited to limited barter arrangements until 2005-6, when Quippo SREI (which became Viom Networks) led India’s first commercial tower leaseup between Spice Telecom and Hutchison, while in parallel Ashmore Group got together with some Israeli partners to form Tower Vision.

Also in 2006, Indus Towers was conceived: a joint venture between Airtel, Hutchison (now Vodafone) and IDEA Cellular which became the world’s largest towerco at launch, with over 70,000 towers.

Reliance Communications and Tata Teleservices carved out their own towercos, Reliance Infratel and WTTL respectively, while Bharti Airtel hived off a proportion of their towers commensurate with their larger scale in the market than their partners in Indus Towers, creating Bharti Infratel. Tata would latter sell WTTL to Viom Networks, but the trend toward MNO-led towercos shifted the balance of power in India, ensuring the towerco business model evolved to optimally serve the MNO.

2008-12 was a gold rush era in Indian telecoms; operators sprung up by the dozen, and towercos added towers and tenants in their thousands. The restructuring of the MNO market, and cancellation of 122 operator licenses, in 2012 brought an abrupt end to this era of growth, and some towercos lost thousands of tenancies overnight.

While new tower builds and technology rollouts would continue to be largely funneled through the towercos, tower transaction deal flow ground to a halt in India until this year, when the landmark acquisition of Viom Networks by American Tower may be the catalyst for further transactions.

The Indian tower market today is a rational, sustainable, efficient business model, supporting the emergence of Digital India and accelerating the rollout of 3G and 4G.

The new European brand of towerco

Europe’s telecom networks matured with minimal input from independent towercos, to the point that many countries’ tower networks featured significant parallel infrastructure. In the meantime, Europe’s broadcast tower assets were increasingly being privatised and shared with the telecom sector. Thus the European brand of towerco has very different characteristics than its international parents: synergies with broadcast asset management and the decommissioning of parallel infrastructure feature large on many European towerco roadmaps.

Europe is a uniquely localised tower market, with over 60 single country towercos and just a couple of multi-country towercos of scale: Cellnex and Telefónica’s newly carved out Telxius. Cellnex is a significant catalyst of change in Europe: for years international towercos were reluctant to make “the offer MNOs couldn’t refuse” for their towers, and the valuation gap stalled the market. Embolded and enriched by a successful IPO, Cellnex is riding a healthy share price to close that valuation gap and consolidate towers across Europe. Having started in their domestic market of Spain and rapidly expanded into Italy, Cellnex is marching North with preliminary acquisitions in The Netherlands and France being just the start of their journey.

The aforementioned Telxius is an exemplar of another characteristic of the European market: the prevalence of MNO-captive towercos and joint ventures. Some of these carve outs are bona fide independent towercos, others function as operators of pooled network resources, sometimes managing active as well as passive equipment, with assets remaining on MNO balance sheets.

Europe remains an early stage tower market, with 64% of assets remaining operator captive, rising to 87% if you count the JVs and operator-captive towercos. But tower transaction deal flow is increasing, captive towercos may come to market as IPOs or for sale to a strategic, so TowerXchange forecast that independent tower ownership in Europe will rise to 49% by the end of 2020 – comparable to CALA and SSA today.

Seven prospective tower company IPOs in the next two years

Unsurprisingly, all 13 of the world’s publicly listed towercos are among the world’s top 50 tower companies by tower count, but some very substantial entities remain unlisted, pointing to the potential for some substantial IPOs in the future.

1. The world’s largest towerco China Tower Company are widely believed to be planning an IPO in late 2017, either as an A-share or on the Hong Kong Stock exchange.

2. Deutsche Telekom could seek a listing of Deutsche Funkturm, which owns just under 40% of the towers and rooftops in Germany.

3. Turkcell have recently disclosed plans to IPO Global Tower, which has ~7,500 towers and over 20,000 total sites.

4. Axiata may list their towerco edotco on the Bursa Malaysia within the next couple of years. edotco has 16,450 towers across six Asian countires.

5. Telefónica has carved out over 16,000 of their sites, plus substantial sub-sea cable holdings, into Telxius with a view to an IPO later this year.

6. The restructuring of Arqiva’s balance sheet could see a partial listing on the London stock exchange for Britain’s 10,550 tower hybrid broadcast-telecom towerco.

7. The sheer scale of the company means African giant IHS looks increasingly likely to IPO rather than be sold to a strategic investor.

No wonder institutional investor interest in the asset class is at an all-time high; towercos with a prospective market cap in excess US$50bn could be coming to market in the coming two years!

China embraces co-construction and infrastructure sharing

China Tower Company (CTC) recently celebrated their second year anniversary, with a staggering 1.55mn towers on their balance sheet, in a Chinese market supplemented by a fragmented ecosystem of 200+ local independent towercos which owns around 50,000 towers between them.

A collaborative approach to co-construction and infrastructure sharing was mandated by the MIIT and SASAC, culminating in the creation of CTC, into which the infrastructure assets of all three Chinese MNOs were injected, with the operators retaining a 94% stake in the venture.

Like India, the Chinese tower market seems to be calibrated to share significant efficiencies with MNOs, illustrated by the lease pricing structure recently released by CTC which shares increasing discounts with anchor and co-locating tenants as more equipment is added to a site, further enhanced through shared energy savings. With an average lease rate thought to be around CNY$2166pcm (US$325), leasing a tower in China is 30% cheaper than anywhere else in the world.

The strength of State influence makes the Chinese tower market unique, as a function of the Party’s agenda to improve the efficiency of deploying CNY tens of billions of capex into China’s tower network for 4G and 5G rollout, and their enthusiasm to improve the efficiency of real estate usage. These agendas are playing out successfully through CTC which claims to have already saved CNY50bn in investment and 13,000 acres of land as a result of co-construction and infrastructure sharing.

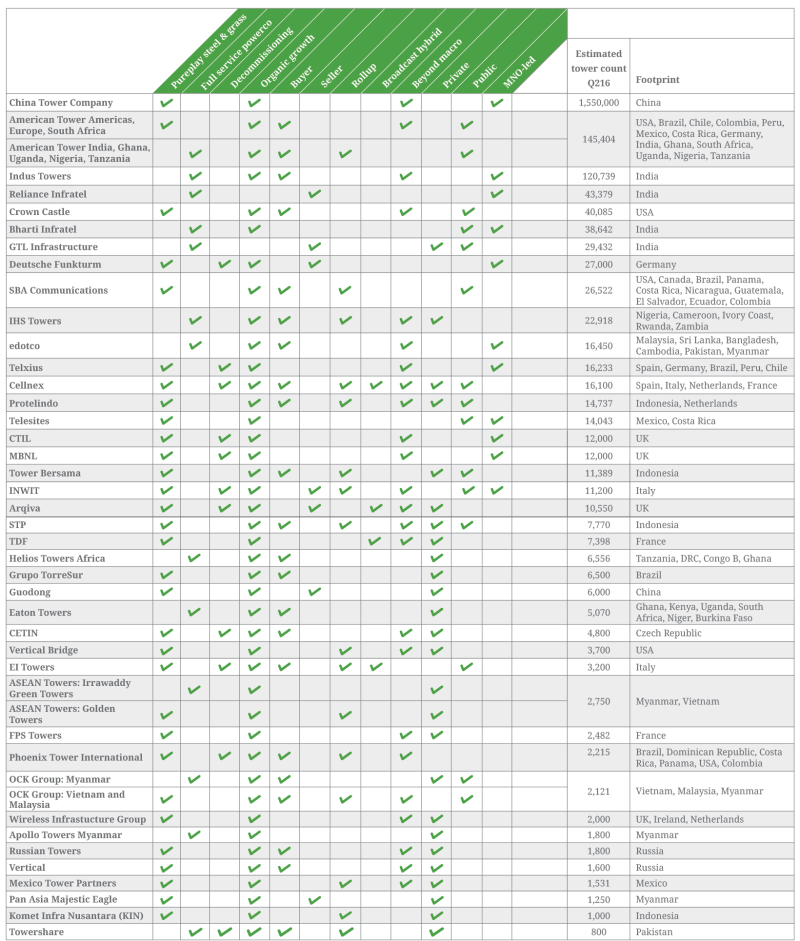

Enough history lesson – let’s compare business models!

TowerXchange have created 11 business model variants into which we have categorised 42 towercos with 800 or more towers. We have excluded a handful of towercos whose business model we don’t know well enough to categorise in this exercise.

The other two towerco business model variants

TowerXchange also classifies some towercos as operating a ‘build to flip’ business model. Focused on build to suit opportunities, high quality build to flip towercos build safe, high capacity structures underpinned by a full set of permits and a good MLA / MSA. There can be a temptation for tower entrepreneurs operating this business model to cut corners on permitting and to deeply discount lease prices – these practices generally have an adverse impact on valuation at exit. There are no build to flip towercos in our matrix of towercos with 800 or more towers as by their nature, build-to-flip tower entrepreneurs have usually sold and restarted their business before reaching this scale.

TowerXchange also recognises small ‘Mom and Pop’ towercos; typically family-owned, these companies seldom have more than 50 towers, and the owners are often keen to retain them as ‘pensionable assets.’

The critical role of independent developers

While our matrix focuses on larger tower companies with 800+ sites, readers should note that in many markets independent developers are grabbing the lion’s share of the new build. For example American Tower built nine towers in South Africa between Q115 and Q116, while independent developers Atlas Towers and Eaton Towers South Africa each built around 100. Over the same period in Brazil, independent developers built 1,430 towers, while the three largest towercos in Brazil, American Tower, SBA and GTS, added just a few hundred towers.

The gap between the new build of large towercos isn’t always as pronounced, but they are seldom the #1 builder in a market; even in a priority market like Mexico, American Tower added 440 towers between Q215 and Q216, whilst privately owned Mexico Tower Partners (MTP) added 571.

TowerXchange’s towerco business model definitions

Pureplay steel and grass: manages only the real estate and tower structure, power is a “pass through” – which means it is a cost which remains the responsibility of the tenant.

Full service powerco: lease rate includes power and O&M, so the towerco is responsible for distributed generation, energy storage and managed services.

Decommissioning: towerco which at least in part specialises in acquiring and consolidating parallel infrastructure in over-built markets.

Organic growth: builds new towers in response to MNO search rings, often supplemented by the speculative acquisition of land usage rights at sites which may be of future interest to mobile network planners.

Buyer: derives, or aspires to derive, a significant level of inorganic growth through large scale sale and leasebacks or participation in joint ventures with MNOs.

Seller: towerco believed to be for sale or heading toward IPO.

Rollup: drives inorganic growth through a series of small acquisitions, often consolidating the assets of ‘build to flip’ or ‘Mom and Pop’ towercos.

Broadcast hybrid: makes significant proportion of lease revenue from broadcast tenants; broadcast towers’ height and dispersed locations make them ideal for MNOs’ rural coverage and microwave backhaul, so many broadcast towercos are diversifying into telecom.

Beyond macro: some towercos include a significant amount of DAS, microcells, small cells, fibre, data centres and/or sub-sea cable in their portfolios.

Finally, we have added the last known tower count for each company, their geographical footprint, and fields indicating ownership: private, public or MNO-led. These fields are not mutually exclusive, e.g. a towerco can be listed on the stock market but significant equity can be retained by an MNO or private company.

If you’re more interested in the future of independent towercos than in their history, meet the leaders of the tower industry at annual TowerXchange Meetups for Africa, Asia, Europe and the Americas - with a Chinese event coming soon! www.towerxchange.com/meetups

Download the business model matrix