Cellnex will acquire 100% of the share capital in Protelindo’s 261 tower Dutch business for €109mn (EV on a cash, debt-free basis). The valuation is in the 15-16x range, based on an expected EBITDA of €8mn in 2017, generating recurrent free cash flow at a 90% ratio. The deal is expected to close within two months, subject to the usual CPs. Cellnex will finance the transaction through existing credit facilities. Here, TowerXchange analyses the deal and shares some exclusive quotes from Cellnex CEO Tobias Martinez.

Why the deal made sense for Cellnex: synergies, scale and a platform to push into Northern and Central Europe

Boosted with a substantial M&A warchest from their successful IPO, Cellnex currently owns 15,120 towers in Southern Europe (Spain and Italy), but their acquisition of 261 Dutch towers from Protelindo may be the first of several transactions in Northern and Central Europe as the company seeks to fulfill their pan-European growth vision.

“From the very beginning Cellnex’s project is to build a true European player, consolidating the business model of independent telco infrastructure operators,” Cellnex CEO Tobias Martinez told TowerXchange. “In this kind of network business size matters. Our focus on European markets will provide us the right scope and presence to better serve our customers.”

Martinez continued: “So the Dutch market fits within our strategic framework: a mature market with potential synergy creation opportunities; a platform to get familiar with markets closer to central and northern Europe as well as the UK; not to say predictability, rule of law as well as stability. Moreover The Netherlands is a market with a solid footprint of independent towercos, and as a stand alone market offers opportunities to further consolidate due to overlapping networks, and with the expected infrastructure densification through small cells and DAS deployment. Infrastructure markets tend to be opportunity driven and if yours is a growth strategy then you have to have heads up and be aware where those opportunities emerge as it has been the case with Protelindo in Netherlands,” concluded Martinez.

Why the deal made sense for Protelindo: a 45% increase in valuation in four years

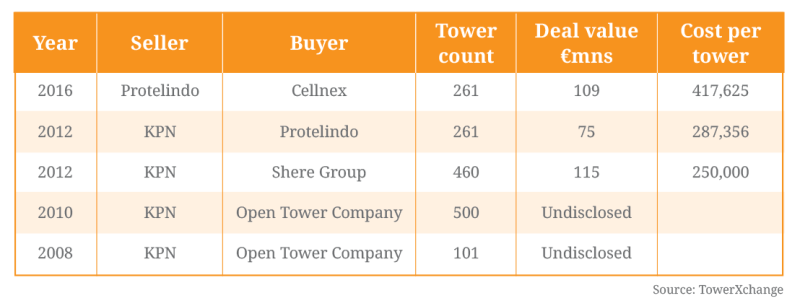

Protelindo had acquired these 261 Dutch towers for €75mn in a sale and leaseback with KPN in 2012. Having financed that acquisition with cash and low cost debt, the acquisition paid for itself in a year, so an exit at a €34mn premium represents a very nice piece of business for Protelindo, particularly since one of the primary motivations for their acquisition of assets in The Netherlands was taxation and, with a tax treaty now in place between the Netherlands and Indonesia, the company no longer needed to retain the assets.

Protelindo grew the revenue of their Dutch business from €7mn to €8.5mn between 2012 and 2016. Protelindo’s 21% increase in revenue yielded a 45% increase in valuation, reflecting not just the exponential value added through lease up, but the background levels of increased interest and valuation ascribed to telecom towers as an asset class.

Protelindo Netherlands BV is a subsidiary of PT Sarana Menara Nusantara, which owns 14,476 towers in Indonesia, and which traces its roots back to Michael Gearon, one of the forefathers of American Tower’s presence in Latin America. The sale of Protelindo’s Dutch assets will enable the company to focus on their Indonesian business.

History of tower transactions in The Netherlands

What Cellnex is buying, and how the portfolio fits into the Dutch tower market

The 261 towers Cellnex are buying from Protelindo are dispersed across The Netherlands, with 80% strategically located along transit corridors and the balance in urban and rural areas. The current tenancy ratio is 1.88, with 75% of revenues linked to contracts extending until 2028. Protelindo operates a lean business model in The Netherlands, with O&M outsourced, so the acquisition is not likely to add significant SG&A to Cellnex’s balance sheet.

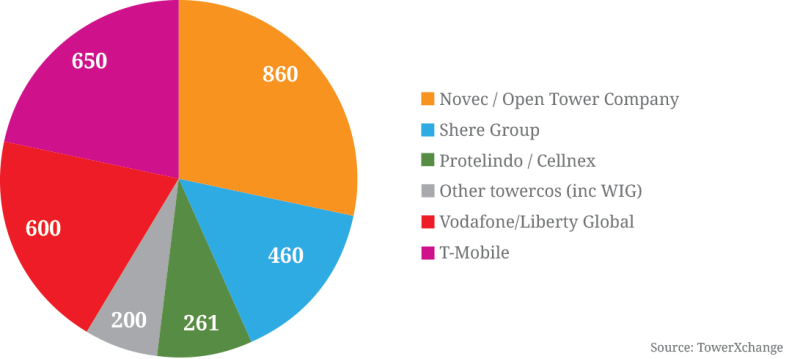

When closed, Cellnex will own 8.6% of the towers in The Netherlands, where 1,721 (57%) of the country’s 3,021 ground based towers are already owned by towercos. While KPN has sold their towers, neither Vodafone nor T-Mobile has a track record of selling towers, but there may be opportunities for Cellnex to drive their market share in The Netherlands through the consolidation of other towercos. However, Cellnex CEO Martinez was cautious when asked about the prospects for further acquisitions in The Netherlands in the short term: “This is not something that has been factored in the model. Having said that, The Netherlands is a market which offers space for rationalisation in terms of the deployed telco passive infrastructure. Thus the possibility of some sort of consolidation cannot be excluded although there are no plans at this point.”

Cellnex will compete with Dutch market leader Novec, which was spun out of broadcast towerco Nozema in 2005 and which scaled through organic and inorganic growth to today’s portfolio of around 850 towers. Novec added 101 towers when KPN bought Telfort, then added three of five batches of towers subsequently sold by KPN. Novec also has access to over 1,000 electricity network sites. TenneT Holding BV is the sole shareholder, Open Tower Company owns the assets, and Novec runs the business.

Other tower companies in The Netherlands include Arcus Infrastructure Partners’ Sheere Group, and Wood Creek Capital Management’s Wireless Infrastructure Group (WIG), which recently secured a significant minority investment from 3i. Both Sheere Group and WIG also have substantial UK tower portfolios.

43% of Dutch telecom towers remain MNO-captive, and TowerXchange are not aware of any near term prospect of sale and leasebacks in the country. There is some bi-lateral sharing of towers between MNOs in the Netherlands on a non-commercial basis but, having sold their towers, KPN no longer participates. Vodafone (now a joint venture with Liberty Global) has around 600 towers, while T-Mobile has around 650 towers. None of Vodafone, Liberty and T-Mobile has a history of monetising their towers. Tele2 recently launched an exclusively 4G network in the Netherlands, but sold most of the few towers they own. Tele2 are likely to rely heavily on co-location and on a RANsharing deal with T-Mobile.

Estimated ground based tower ownership in The Netherlands

“The fact that existing MNOs in the market may deploy their own equipment beyond their current RAN sharing agreements can support further growth opportunities from an organic perspective. MNOs’ divestment or unbundling of their existing passive infrastructure is always a potential scenario,” said Cellnex’s Martinez.

A significant majority of towers in The Netherlands are fibreised. Only 20% of The Netherlands’ 15,204 cell sites are macro cell sites, with the balance being rooftops, DAS and small cells.

Investment in macro towers is minimal in this mature market: a low double digit count of new towers is erected in a typical year, with Novec seemingly getting the majority of the BTS work. With 4G coverage ranging from 92-99% having been deployed primarily on existing 2G and 3G infrastructure, Cellnex anticipates opportunities in small cells and DAS. “This is a structural change that will drive every single market in which mobile broadband becomes a priority. Small cells, indoor as well as outdoor, and DAS too is a kind of next frontier which is close to hatching. It is clear that network densification to ensure a smooth and wide penetration of LTE technologies will be a core part of the business in the upcoming years and in every market,” commented Martinez.

There hasn’t been much decommissioning to date in The Netherlands, and what there has been has been driven by optimising land lease costs rather than driven by consolidation.

There have been some reports of ground lease aggregators kicking the tyres on the Dutch market, but nothing of significant scale.

What next for Cellnex?

The Netherlands might be a first step in a larger expansion into Northern and Central Europe for Cellnex, so TowerXchange asked Martinez to share Cellnex’s vision for expansion in the region.

“There are no specific targets in quantitative terms beyond the fact that we aim to become a European player as we already are in fact. Again a key driver for growth are opportunities and those arise where there is an MNO willing to divest its assets or an existing towerco whose shareholders would like to sell or become part of a wider international project. This is what frames our approach together with customary analysis regarding market specifics like stand alone growth potential, size, competitors, space for rationalisation, market stability and predictability,” concluded Cellnex’s Martinez.

TowerXchange conclusions

The Netherlands is a mid-sized Northern European tower market characterised by a culture of infrastructure sharing, and steady growth. Operational and country risk is low. This creates a justifiably high valuation of telecom towers as ‘pensionable assets’ – robust infrastructure with long term contracts, generating predictable returns from credit-worthy customers.

The Netherlands is a great first step North for Cellnex, and it won’t be their last. Martinez and his team are well on the way to fulfilling a vision of creating the first pan-European towerco of scale. This deal also represents tremendous return on capital invested by Protelindo from a European venture initially motivated partly by taxation, a venture which seldom caused them any operational problems, and which in four years turned €75mn into €109mn.

European towers: nice work if you can get it!

Cellnex admitted to prestigious IBEX® 35 benchmark index

Cellnex Telecom (CLNX:SM) will been included in the IBEX® 35 benchmark index of Spain’s stock exchange on 20 June 2016.

Since its debut on the Spanish stock exchange on 7 May 2015, Cellnex Telecom has maintained its initial pricing in the €14 range, accumulating a positive differential against the IBEX 35 of 22%. Cellnex’s current market cap is €3.3bn. The reference shareholders of Cellnex Telecom include Abertis (34%), Columbia Threadneedle (7.8%), BlackRock (6.2%), CriteriaCaixa (4.62%), and Cantillon Capital Management (3%), leaving the company’s free float at 43%.

The incorporation into the IBEX® 35 index will raise the visibility of Cellnex Telecom’s shares and highlight the company’s growth plan.

If you missed Tobias Martinez’s keynote, and Protelindo’s roundtable on how to scale a towerco, at the last TowerXchange Meetup Europe, don’t miss the 2nd annual TowerXchange Meetup Europe, taking place on 4-5 April 2017 at the Business Design Centre, London. Click here for more details.