At the TowerXchange Meetup Europe, TowerXchange opened proceedings with a run down of the key characteristics, trends and transactions in the European tower industry, examining key motivators and forecasting how the shape of the market is set to change. We summarise some of the main take home messages and revisit key charts and figures presented to provide a 101 on this rapidly evolving marketplace.

The current state and forecast future growth of the European tower industry through 2020

In Europe (inclusive of Russia and the CIS), there are a total of 600,000 cell sites. These sites are comprised of towers, streetpoles, rooftops and in-building solutions – by TowerXchange’s definition, we count any site that is potentially shareable. As a mature tower market, that total of around 600,000 is staying fairly constant with new build being more or less cancelled out by the decommissioning of parallel infrastructure.

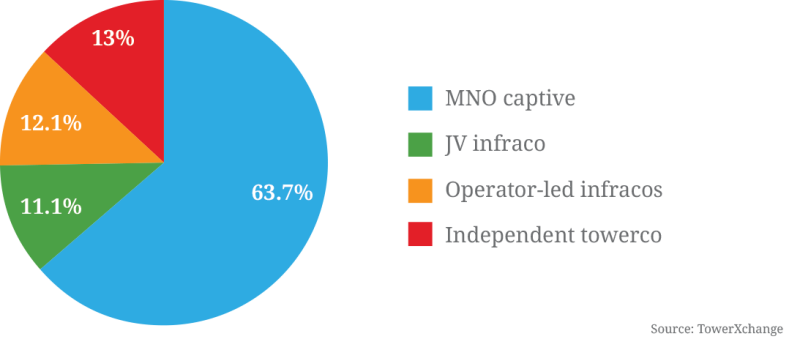

The structure of the European tower market is quite unique, with joint venture infrastructure sharing companies such as CTIL and MBNL in the UK, VICTUS Networks in Greece, NetGrid in Romania, Mosaic in Ireland and a host of others in Scandinavia operating (if not always owning) 11.1% of the continent’s towers (figure one). They’re a different breed from a commercial towerco because they are typically created to serve solely the needs of their parent MNOs, may price leases solely at a chargeback level, and may not lease sites to third parties.

A second unique characteristic of the European market is the prevalence and scale of broadcast-telecom hybrid towercos. Broadcast infrastructure is generally a different but parallel asset class characterised by less growth than the telecom towerco asset class. Hybrid broadcast and telecom towercos represent around 9% of the 13% of Europe’s towers owned by independent towercos; just 4% are pureplay telecom towercos… for now!

Operator-led carve out towercos, where the parent MNO retains >51% of the equity in the towerco, account for 12.1% of Europe’s towers, a segment supplemented by the addition of Telefónica’s Telxius, but from which INWIT may be exiting upon completion of their sale: carve out and monetise is becoming as popular as the pure sale and leaseback model.

There is no European tower market per se, there are 50 local tower markets, the size of some of which are shown in TowerXchange’s analysis of the independent tower market in Europe. There are also no pan-European towercos, in fact of the 61 European towercos and infracos identified by TowerXchange, only six have a presence in multiple countries, and most of those are neighboring countries. However, we expect to see the rise of multi-country towercos of scale in the coming five years, led by Cellnex.

Figure one: Current ownership of Europe’s ~600,000 towers

Towers versus rooftops and streetpoles

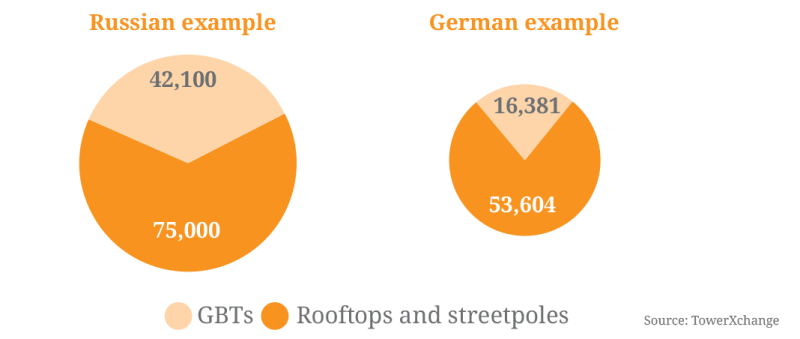

It is something of a misnomer to talk about a 600,000 tower European tower market, since in several markets, rooftop structures significantly outnumber traditional ground based towers (GBTs), exemplified by Russia where only 36% of telecom structures are GBTs, and Germany where it’s only 23% (figure two)

Rooftop structures may be as investible or less investible than full GBTs as a function of their structural capacity, rights of access and the contractual relationship with the landlord.

A lot of the new build we’re seeing in Europe consists of streetpoles and infill microcell sites, rather than full scale GBTs.

Figure two: Towers versus rooftops and streetpoles

An introduction to Europe’s towercos

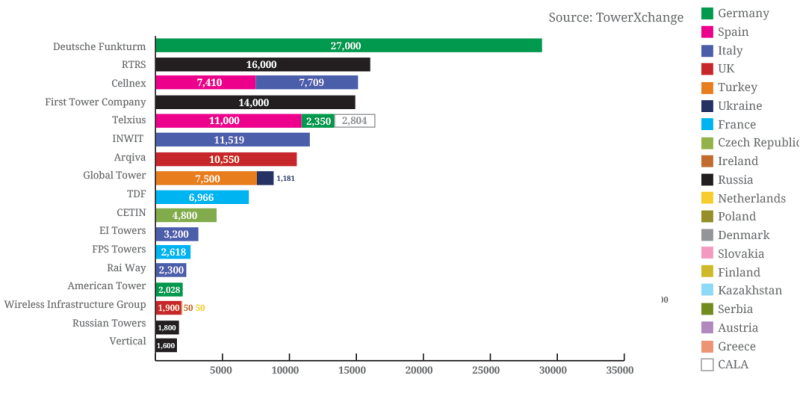

There are 17 towercos in Europe which possess portfolios of over 1000 towers, rooftops and streetpoles (figure 3).

1. Deutsche Funkturm is Deutsche Telekom’s captive towerco, and owns just under 40% of the towers and rooftops in Germany.

2. RTRS is the Russian broadcast towerco with 16,000 towers.

3. Cellnex is the fastest growing towerco in Europe, with 15,120 towers across Spain and Italy and an appetite for further opportunities in their existing markets plus Portugal, France, Germany, Austria, Switzerland, Belgium, the Netherlands, the UK and Ireland.

4. First Tower Company is Russian operator MegaFon’s infraco and manages a portfolio of 14,000 towers. MegaFon has been open about its intention to sell to a strategic investor in the next 12-24 months.

5. Telxius, Telefónica’s infraco manages a portfolio of 13,350 sites in Europe – 2,350 ground based towers in Germany and an estimated 11,000 ground based towers and rooftop sites in Spain. Telefónica is considering an IPO of the unit on the Madrid Stock Exchange in early July.

6. INWIT, Telecom Italia’s infraco with 11,519 sites was listed on the Milan Stock Exchange last year and a further stake in the company is being fought over by Cellnex/F2i and EI Towers.

7. Arqiva, the UK’s broadcast telecom hybrid with 10,550 towers, are currently restructuring their balance sheet.

8. Global Tower, Turkcell’s infrastructure subsidiary with ~8,000 towers in Turkey and a further 1,181 in the Ukraine (managed under UkrTower) is at the beginning of an IPO process.

9. TDF, the French broadcast/telecom hybrid towerco has 6,966 towers, was recently refinanced and is now owned by a consortium including Brookfield and Arcus.

10. CETIN is a 4,800 tower infraco carved out of O2 Czech Republic, which owns and operates transmission, passive and active infrastructure.

11. EI Towers, the Italian broadcast towerco with 2,300 sites, also incorporates TowerTel with over 900 telecom towers. The company is one of the shortlisted bidders for the INWIT equity stake and is in talks regarding a takeover of rival Italian broadcast towerco, Rai Way.

12. FPS Towers has 2,618 towers plus rights to over 20,000 rooftops in France. It is rumoured that the company may be sold by investors Antin Infrastructure Partners.

13. Rai Way is an Italian broadcast towerco, less aggressively seeking opportunities in the telecoms sector than its rival EI Towers. There exists the possibility that Rai Way and EI Towers may merge.

14. American Tower, the world’s largest independent towerco American Tower has just a 2,028 tower portfolio in Germany. The company is reportedly seeking a new minority investor, potentially to fund expansion in Europe.

15. Wireless Infrastructure Group is the largest pureplay independent towerco in the UK with over 2,000 sites, a few of which are in Ireland and the Netherlands.

16. Russian Towers has built a portfolio of 1,800 sites in their home country Russia. As one of the finalists to acquire VimpelCom’s 10,400 towers in Russia and with an appetite for transactions across the CIS, their portfolio may be set to increase substantially.

17. Vertical, with a portfolio of 1,600 sites are competing with Russian Towers in the ongoing VimpelCom process in Russia and similarly have an appetite for further tower sales in the region.

Beyond this, TowerXchange track 27 telecom towercos and smaller broadcast towercos with less than 1,000 towers and 12 JV infracos, the largest of which are the UK’s CTIL and MBNL, each managing portfolios of ~18,000 sites. Further information on these players can be found in Read TowerXchange’s who’s who in European towers for more information on each player.

Figure three: Europe’s 18 towercos with >1,000 assets

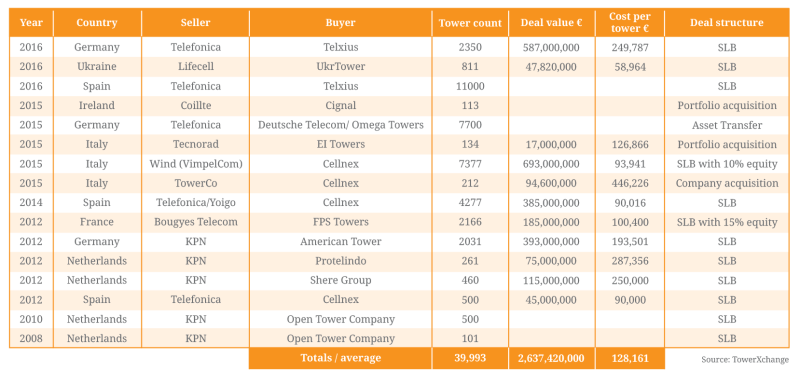

European tower deals since 2008

We’ve seen over €2bn deployed since 2012 to transfer 25,000 towers from MNO-captive to independent towercos (see table one). However, we think this is the tip of the iceberg of an investment of more than 10x that magnitude over the coming five years.

The trend to monetise European towers was initiated in the Netherlands where KPN sold 1,300 towers to three different towercos, then again by KPN in Germany to American Tower, before Bouygues Telecom’s sale of over 2,000 towers to Antin’s FPS Towers in France.

What really kick started the European tower industry were large transactions by Cellnex in Spain (with Telefónica and Yoigo) and 14 months ago with Wind in Italy, bringing us up to the current day with the VimpelCom process to sell 10,400 towers well under way in Russia.

A second trend is starting to emerge in the monetisation of European passive infrastructure, initiated by Telecom Italia’s strategy for their infraco, INWIT. With a partial listing of INWIT on the Madrid Stock Exchange now being followed by a strategic sale of a further tranche of equity in the infraco, other operators are considering both options for their newly created captive towercos. Turkcell have initiated the IPO process for Global Tower, Deutsche Telekom have hinted at a potential listing of Deutsche Funkturm, Telefónica are rumoured to be planning an early July IPO of Telxius, and MegaFon are looking for a strategic buyer for First Tower Company.

Table one: European tower deals since 2008

Drivers of change

Why wasn’t there a substantial pipeline of European tower transactions and monetisations when there is now?

Firstly, many European MNOs didn’t need the cash as urgently as did their counterparts in Africa for example. But the efficiency benefits of transferring assets to infrastructure specialists, whilst focusing on selling minutes and megabytes, remains common to MNOs worldwide.

European towers is a seller’s market, and with relative valuation arbitrage so significant, whether they’re considering selling and leasing back or carving out and keeping their towers, the monetisation of towers is creeping up the boardroom agenda within MNOs across Europe.

Where is activity expected?

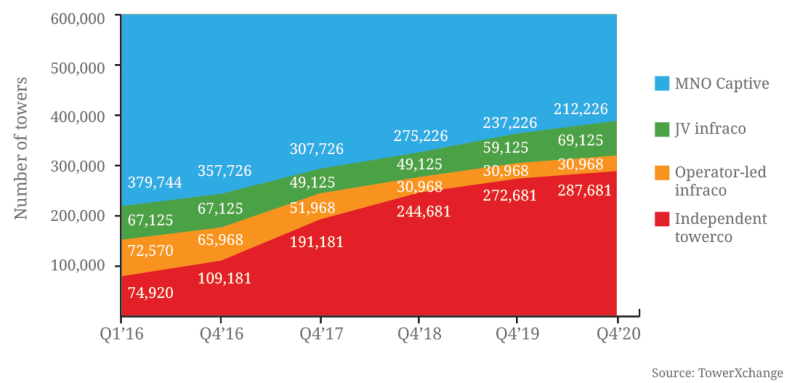

Looking at figure four, one can see that the European tower industry is awash with activity. Of Europe’s 600,000 towers (including Russia and the CIS) 36% are owned by infracos and a third of which (13%) are owned by independent tower companies. Examining the transactions which TowerXchange are tracking and the trends we are observing, we forecast the percentage of towers to be owned by infracos (independent towercos + operator-led towercos + JV infracos) to increase to 40% by the end of this year and 65% by 2020. In terms of ownership by independent towercos, we forecast this to increase to 18% by the end of 2016 and 48% by 2020 (see figure five).

Figure four: Europe heatmap

Figure five: Forecasted breakdown of ownership of Europe’s ~600,000 telecom tower and rooftop structures 2016-2020