On 28 April 2016, Turkcell’s Board of Directors announced that the company was initiating the process for an IPO of an undisclosed amount of equity in its infrastructure business Global Tower. Drawing upon discussions held at the Turkey roundtable at April’s TowerXchange Meetup Europe, we examine the Turkish market and Turkcell’s freshly announced IPO process.

The Turkish mobile market

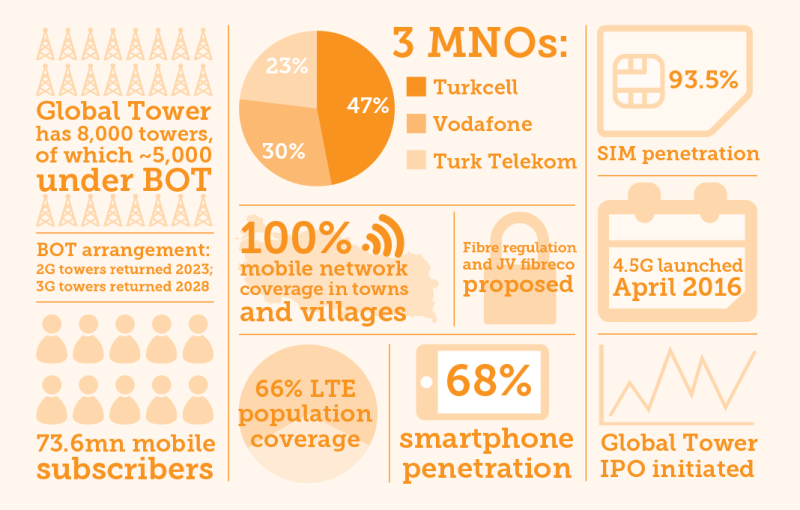

As of December 2015 there were 73.6mn mobile subscribers in the Turkish mobile market, representing a penetration rate of 93.5%. On 9th April 2016, the Turkish Ministry of Transportation, Communication and Maritime Affairs announced that all villages in Turkey now have mobile coverage following the rollout of the government’s Universal Service Fund Network Mobile network which brought coverage to underserved populated rural areas.

Turkey’s mobile operators

There are three mobile network operators in the Turkish market - Turkcell, Vodafone and Turk Telekom. With both Turkcell and Turk Telekom active in both fixed line and TV, and Vodafone looking to go the same way, the companies are better described as converged communication and technology services providers than pure-play mobile network operators.

Turkcell are Turkey’s incumbent mobile operator, boasting the largest market share with 34mn mobile subscribers (47%). Turkcell Turkey’s Q1 16 revenues were TRY2.9bn, up 10% on the previous year’s performance. In 2006 Turkcell founded Global Tower, a 100% owned subsidiary which is the country’s only telecom infrastructure operator and which is responsible for managing Turkcell’s infrastructure. Whilst Turkcell have not confirmed the size of their tower portfolio, they are believed to have approximately 24,000 sites of which an estimated 8,000 are ground based towers.

Multinational player Vodafone are the market’s number two operator with 30% of the market share. The company entered the country in 2006 and, after a turbulent first couple of years, have seen their revenues grow continuously.

Whilst leading the fixed-line market, Turk Telekom is number three in terms of mobile market share, with 17.7mn mobile subscribers as of Q1 2016 (adding 1.1mm subscribers in the past 12 months). The Turkish government has a 35% stake in the company, whilst 55% is owned by Oger Telecom and 15% is listed on the Istanbul Stock Exchange. Previously operating their mobile business under the brand Avea, January 2016 saw the company rebrand the unit as Turk Telekom.

Mobile subscriber market share

The launch of 4.5G and LTE rollout

On 1st April, Turkey launched LTE services with LTE population coverage currently sitting at 66%. Smartphone penetration stands at 68% of which 42% of smartphones are 4.5G enabled, while 22% of data traffic currently uses 4.5G networks. In the 26 August 2015 4.5G spectrum auction, Turkcell acquired the largest share, acquiring 47% of all spectrum auctioned, whilst Turk Telekom acquired 30% and Vodafone 23%. The spectrum was technology neutral, giving operators more flexibility in their network planning.

Fibre penetration and the establishment of a joint venture

Fibre penetration levels in Turkey are less than half the OECD average. Turk Telekom has by far the most extensive network in the country, having invested over US$7bn in the past decade in developing their infrastructure. The operator has laid 213,000km of fibre, approximately six times more than mobile incumbent Turkcell which has an estimated 35,000km. Turk Telekom effectively sets the rates at which it charges its competitors to use the network, and both Turkcell and Vodafone are calling upon the government to ease the burden on investment and introduce tighter regulation of wholesale fibre access prices, whilst proposing a joint venture which brings together all of the fibre resources of the three operators. Whilst Vodafone and Turkcell are strongly behind the notion of a joint venture, estimating that it will save operators around US$12.5bn, Turk Telekom are less than keen having already deployed a significant amount of their own capital in establishing a network.

Tower ownership in Turkey

Towers in the Turkish market were constructed under a build-operate-transfer (BOT) model with licenses for 2G spectrum set to end in 2023 and licenses for 3G by 2029. At this time, applicable active and passive infrastructure must be returned. Exactly how this will play out is yet unclear with it thought that a tender process will be introduced for the operators to buy back the towers, although reference prices have not been determined.

Not all of Turkey’s towers were constructed under the BOT agreement. Global Tower is Turkey’s first and the single tower operator offering professional tower and infrastructure services. Since the establishment of the company in 2006 Global Tower has erected their own towers and has a revenue share model with the tower owners. This unique position gives Global Tower the opportunity to grow its business at the end of the MNO’s BOT time period.

Infrastructure sharing

1,100 - 1,200 RANshared base stations belong to the government’s universal service network which was designed to bring connectivity to rural communities where the population of the community is under 500. As mentioned previously, under the arrangement each of the mobile network operators must take it in turns to manage the network for a three year period, without no financial remuneration from the other parties or the government.

Beyond the RANsharing agreement put in place under the universal service network, there is a degree of passive infrastructure sharing between the operators. Turkcell have confirmed they use a small number of third party towers in the country, whilst around 25% (~2,000) of their towers are thought to be used by Turk Telekom and Vodafone. Assuming most of the co-locations are on ground based towers rather than other sites (e.g. rooftops), this suggests Global Tower might have a tenancy ratio of around 1.25 on their greenfield towers.

Power supply to Turkey’s towers

Nearly all of Turkey’s towers are thought to be connected to the grid, although in the eastern part of the country, some issues exist with the sustainability of the grid. In order to bring power to sites quickly some of the operators have paid to build the connections from the electricity grid. Electricity costs in Turkey are thought to account for 30% of total site costs.

What is the rate of new build and what does it cost to build a tower?

The average cost to build a tower in Turkey is thought to be US$30-50k which is low by international standards, perhaps reflecting the strong local steel tower manufacturing industry.

Last year approximately 500 towers are thought to have been erected in the country, with about 50% of these built to replace existing towers. New towers built by the operators, or their towerco, will not need to be returned to the government when those built under the BOT scheme are.

The commencement of an IPO process for Global Tower

On 28 April Turkcell announced that its Board of Directors had decided to initiated the process for an IPO of a “certain amount of shares” in Global Tower. Global Tower is thought to possess a portfolio of approximately 8,000 towers in Turkey, while they also have a wholly owned subsidiary, UkrTower, with an additional 1,181 towers in the Ukraine. Both the Turkish and the Ukrainian assets are held under the Global Tower business unit, putting the portfolio at just over 9,000 towers. This number is complicated by the fact that an estimated 60% of their Turkish towers are held under a BOT arrangement with the Turkish government, with those erected as part of 2G rollout reaching the end of their license and needing to be returned in 2023; and those under 3G by 2028. Negotiations are ongoing between the operators and government to reach an agreement on how this will be managed, however it is an uncertain variable to any potential valuation of the Global Tower portfolio.

With regards to the motivations behind the IPO, Turkcell Chief Strategy Officer Ilter Terzioglu stated in an interview with TowerXchange, that the company wanted to ensure that the true value of their assets was understood and appreciated by the market. He added that the evaluation of different options to create shareholder value was key and that “managing our business more efficiently and achieving a more accurate positioning of our assets are among our priorities for the entire Turkcell Group”. With Turkcell currently trading at 6.2x EBITDA and most listed towercos trading at >12x EBITDA, it is likely that Turkcell will stand to benefit from transferring its assets from their balance sheet to that of a listed towerco.Then known as Avea, Turk Telekom tried to monetise their towers around five years ago, but the process was aborted. That Turkcell is now listing their towerco, Global Tower, illustrates the maturation of the Turkish market.