Mobile market overview

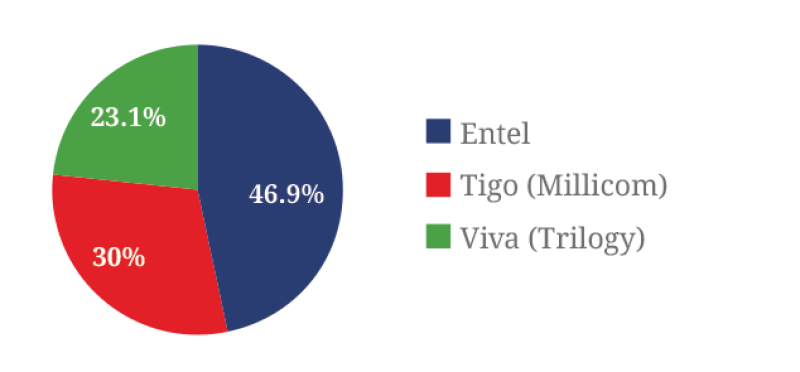

Bolivia had an estimated population of 10.8mn people and 10.4mn mobile subscriptions at the end of 20151, giving a mobile penetration of 96% - the third lowest level of penetration in South America ahead of only Guyana (84%) and Ecuador (80%). Around 90% of subscribers have a pre-paid account, which ranks 2nd highest amongst the South American countries. Guyana ranks the highest with 96% pre-paid subscribers. There are three mobile network operators (MNOs) serving the Bolivian market (See figure 1). The largest operator, Entel, serves 4.9mn subscribers which equates to a market share of 46.9%. The second largest operator by subscriber numbers is Tigo (Millicom) which has 3.1mn subscribers (30.0%) and VIVA, the smallest of the three operators, serves the remaining 2.4mn (23.1%) subscribers.

Key mobile developments

Bolivia has low mobile penetration for the South American region when compared with the highest performing countries of Suriname (175%), Uruguay (159%), Chile (146%) and Argentina (144%). However, Bolivia’s national subscriber base grew significantly between 2007 and 2013, almost tripling in size from 3.6mn subscribers to 9.8mn in the six years. Since 2013 subscriber growth appears to have stagnated somewhat, only increasing by 0.6mn in the two years to the end of 2015. Forecasts predict that the subscriber base will reach 13.2mn by 2020.

Entel first launched 3G services in Bolivia in Q3 2008 and enjoyed monopoly status for two years until Tigo joined the market, shortly followed by Viva in the first half of 2011. The uptake of 3G subscribers in Bolivia was initially slow however the market quickly developed and the number of new subscribers per quarter reached 244,000 at its highest point in 2013. This number has since fallen, averaging 133,000 new subscribers per quarter in 2015 and this number is expected to remain relatively constant up to 2020.

Bolivia’s first telecommunications satellite was launched in December 2013 and came online in April 2014 with the purpose of providing internet and mobile connections to Bolivians in areas not currently covered by the operators’ infrastructure.

Mobile subscriptions - market share

Rollout of 4G

Entel first launched 4G services in Q4 2012 and was the sole provider within the market until Q4 2013 when the regulator, ATT (Autoridad de Regulación y Fiscalización de Telecomunicaciones y Transportes), assigned 4G LTE spectrum in the 700MHz band to Tigo and Entel following successful bids at auction. The third operator, Viva, chose not to participate in the auction.

Entel first offered 4G services in the cities of La Paz, El Alto, Santa Cruz and Cochabamba in April 2014. The market responded well to the service offering and reports stated that Entel signed up to 2,000 subscribers in its first week of operation. Tigo quickly followed Entel to the 4G market launching its services in July 2014, citing that demand was clearly present as demonstrated by a trend of increasing smartphone and tablet usage across the country. Viva launched its 4G services exactly one year after Tigo in the 1700MHz and 2100MHz frequency bands.

Entel leads the way in terms of market share in 4G with 0.37mn (68.3%) of the total 0.55mn 4G subscribers. Tigo holds 24.8% market share with 0.14mn subscribers and the smallest 4G provider, Viva, serves 0.04mn subscribers, a market share of 6.9%.

As the 4G market matures and coverage begins to reach the more rural areas, operators are investing in physical infrastructure, in order to improve their service offering to subscribers. In the last two years Tigo and Entel have invested heavily in lengthening the country’s fibre infrastructure as well as improving Bolivia’s connectivity with international submarine cables.

MNOs activity

Entel (Empresa Nacional de Telecomunicaciones), Bolivia’s largest mobile operator by market share was state owned until 1995 when it was acquired by Telecom Italia (TIM). Entel operated as a subsidiary of TIM for thirteen years until the Bolivian President decided to re-nationalise a number of the country’s energy services and the government reclaimed the operator through a contentious supreme decree. Entel has posted a positive financial performance in Q1 2016 and has recently announced a significant investment plan to increase the country’s fibre-optic backbone by 4,000km.

Tigo (Millicom) first entered the Bolivian telecommunications market in 1991 under its previous guise of Telecel which launched Bolivia’s first analogue cellular network. In 2006, with a market share of 23%, the company rebranded to use the more recognised Tigo name, whilst remaining a subsidiary of Luxembourg-based Millicom.

Viva (Trilogy) is the market name for the mobile operator NuevaTel PCS de Bolivia which was acquired by U.S. holding company Trilogy International Partners in 2006. Following an investment of US$100mn, which included the deployment of 200 new antennas, Viva reached 75% coverage by geographical territory in 2012.

Regulation and the tower sharing market

Telecommunications in Bolivia was regulated by SITTEL (Superintendencia de Telecomunicaciones), until 2009 when the Bolivian government decided to consolidate the regulatory authorities of three sectors: transportation, post and telecommunications. The resulting regulator is ATT (Autoridad de Regulación y Fiscalización de Telecomunicaciones y Transportes).

ATT regulates the entire telecommunications industry, including radio spectrum, merger and acquisition activity, coverage and service agreements and price competition. A major initiative of the ATT in recent years has been to encourage all subscribers to reregister their phones with their operators in order to switch off unregistered devices, in an attempt to decrease the amount of mobile phone related crime in the country - which has been on the rise.

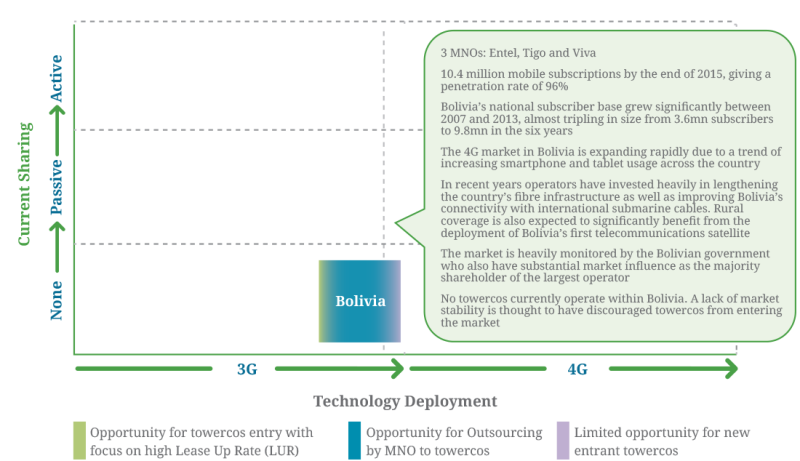

No towercos currently operate within Bolivia, even though market developments, including the three operators rolling out 4G and prioritising cell site densification, could favour the entrance of infrastructure investors.

Reports suggest that a lack of market stability is a significant factor driving the lack of towercos within the Bolivian market. In 2008, following months of disputes, the Bolivian president Evo Morales decided to re-nationalise the country’s largest operator Entel, purchasing a 50.9% stake from majority shareholder TIM. This move coincided with the re-nationalisation of major oil and gas companies through a mixture of decrees and acquisition, as part of an initiative by the president to reclaim the countries “basic services”.

In 2013, Morales is reported to have threatened Tigo and Viva with re-nationalisation following claims that the operators were not communicating with police in a timely manner during investigations surrounding the countries rising mobile phone related crime.

Government interference is likely to have influenced the poor ranking Bolivia received from the World Bank in its 2015 ‘ease of doing business’ indicator – Bolivia was given a ranking of 157th out of 189 countries.

Despite the increasing favourability of the market, it is reported that towercos require further convincing before seeking to acquire infrastructure within the market.

Conclusions

With the 8th largest population in South America (10.8mn people) and the third lowest mobile penetration (96%), there is considerable room for subscriber growth in the Bolivian mobile market. 4G services have been launched and consumer appetite is growing rapidly with all three operators now providing a service in the country. Major advancements in fibre infrastructure as well as rural coverage in the form of satellite deployment have been witnessed and are expected to significantly increase the service offerings available to the 10.4mn mobile subscribers.

The market remains heavily monitored by the Bolivian government who also have substantial market influence as the majority shareholder of the largest operator. Reports suggest that potential towercos are dubious with regard to government interference and the volatility displayed during the re-nationalisation of Entel, and are only likely to enter the market when a more stable environment is evident.

1. GSMA