Telesites isn’t just a new entity in the Mexican tower market, but a towerco evolved from the genes of one of the strongest mobile network operators in the Central and South American telecom landscape. A towerco which started trading with close to 11,000 towers in the unique Mexican tower market. Analysts have been underwhelmed with Telesites, and the company’s IPO was followed by a swift devaluation. However, closer analysis reveals a good reason for the volume of post IPO sales, while Telesites build volume has been impressive. The key challenge remains achieving the company’s bullish forecast of a tenancy ratio of 1.5 by 2020.

Necessity is the mother of invention and Carlos Slim had to create Telesites to address the regulator’s concerns about the dominant position of América Móvil in the Mexican telecom market. The story is well known to everyone but since its debut on the Mexican Stock Exchange, back in December 2015, Telesites’ shares have failed to impress and many jumped to the conclusion that the towerco was nothing but a financial exercise and a mechanism for the Mexican giant to keep operating and avoid IFETEL’s further restrictions.

The company’s trading debut was met with lukewarm reactions from the market and many analysts recommended selling as early as two days after its IPO on 21 December 2015. Another factor that drove the initial sale of shares was the initial assignment of Telesites’ shares to América Móvil’s shareholders as a condition of the spin-off. A fact that forced many investors to sell their shares to meet composition requirements for their portfolios.

Many investors sold their shares within one month of trading to re-balance their positions and drove the initial valuation of the stock down. In fact, Telesites started trading at MX$12.9 and is now stable in the 10s, with some analysts forecasting further drops within this year.

Telesites’ performance in the stock market received plenty of media coverage due to its link to Carlos Slim, the second richest man in the world with an estimated net worth of US$77.1bn, and the relative speed at which the spin-off came to life, mostly due to the pressure of the Mexican regulator.

Organic growth and tenancy ratio: expectations vs reality

But if we look beyond the dynamics of the financial market, how is Telesites doing as a towerco in Mexico? Did Mexico need it and if so, is the company likely to meet the goals it set for itself?

Telesites originally forecasted organic growth plans of as many as 1,000 new towers per year, exclusively for its anchor tenant América Móvil. A planned growth considerably higher than the expectation of any other listed towerco in the CALA market. Along with its organic growth plans, Telesites shared tenancy ratio goals of 1.5x by 2020.

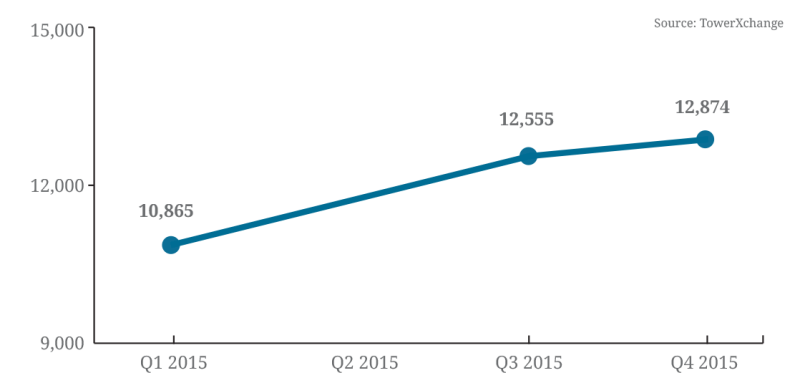

In terms of organic growth, in 2015 the company has been overachieving and grew its portfolio from 10,865 (Q1 2015) to 12,874 (Q4 2015), adding 2,009 new sites in less than twelve months of operations. Its original plan to reach 18,000 new sites by 2020 seems more achievable now than when first announced.

Telesites tower count

If Telesites was to maintain this growth pattern, we would see its tower count surpassing 20,000 by 2018. However, beside América Móvil’s expansion plans, I am not sure the other carriers are likely to greatly contribute to the towerco’s growth.

On one hand Telefónica doesn’t have a history of high investments in Mexico and isn’t likely to bring seizable business to Telesites, particularly given that Telefónica is currently creating its own carve-out towerco, Telxius. And the remaining player in the market, AT&T, is reportedly reducing its new build plans having audited assets acquired from Nextel and Iusacell.

In 2015 American Tower renewed a 14-year global MLA with AT&T which covers the U.S. as well as Mexico and referred to expectations for “double-digit organic growth” in the country, which hints that the alliance between AT&T and American Tower could include the carrier’s new sites in Mexico.

As said, AT&T isn’t likely to build aggressively in Mexico. In fact, they originally forecasted around 3,200 new sites (between swaps and new builds) by 2018 but this number could be reduced since sites acquired from Nextel have greater potential of utilisation than originally thought.

The government’s planned shared 4G network (Red Compartida) could further dampen the demand for new sites but for now the project is still up in the air. In fact, the bidding process has been postponed to give more time to the Secretariat of Communications and Transport (SCT) to deal with the requests for clarification submitted by the contestants. In order to function, it’s been estimated that the Red Compartida will require around 12,000 new sites at a cost of US$7bn. But to date, many seem sceptical with regards to the likelihood of this mega-project ever reaching scale.

In terms of tenancy ratio, Telesites’ outlook to bring it up to 1.5x by 2020 seems bold. First of all, América Móvil’s new builds - which are likely to be 100% developed by Telesites - will dilute its tenancy ratio and, as previously discussed, Telefónica and AT&T may contribute only marginally to its growth.

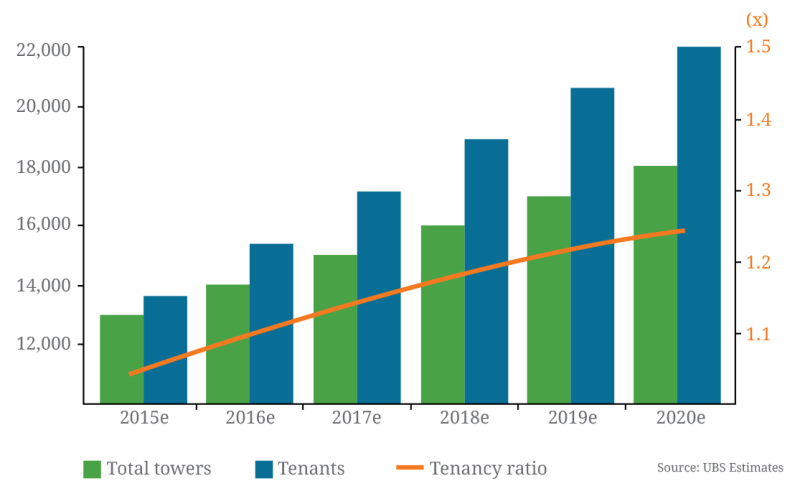

Tenancy ratio to expand: 2015-2020

Experts at UBS have forecasted the demand for new sites to reach 5,000 by 2020 and commented that “even with Telesites taking 80% share we believe this will drive its tenancy ratio to only 1.24x by 2020.” This scenario is created on the premise of an AT&T/American Tower alliance which would exclude Telesites from any BTS project assigned by the U.S. operator.

Experts at UBS have forecasted the demand for new sites to reach 5,000 by 2020 and commented that “even with Telesites taking 80% share we believe this will drive its tenancy ratio to only 1.24x by 2020.” This scenario is created on the premise of AT&T/American Tower alliance which would cut out Telesites from any BTS project assigned by the U.S. operator

As previously mentioned, Telefónica has a history of low investments in Mexico and many Mexican players have confirmed that to date, the Spanish operator hasn’t announced any change of strategy.

Five critical considerations to maximise towerco valuations

Telesites value considerations

Looking at critical considerations to maximise the valuation of a towerco, I’d like to compare them against Telesites’.

PAPER

América Móvil’s dominant position in the telecom sector has spread its effects on to Telesites, which is subject to peculiar rules aimed at de-risking its preponderance in the Mexican market. Specifically, Telesites must offer equal terms and prices to all its customers and publicise the terms and conditions as well as prices.

Additionally, Telesites is subject to ad-hoc regulatory inspections which are a definite incentive for the company to ensure its paperwork is always up to date and in order.

ASSETS

At the time of the spin-off, América Móvil didn’t transfer all of its assets to the new entity and possibly retained the core of its portfolio to avoid having to share it with its competitors. However, with close to 13,000 sites (or 50% of all sites in Mexico) in its portfolio, Telesites has much to offer to its customers.

It’s important to highlight that América Móvil didn’t only build towers but added so-called telecom oasis to its portfolio. These sites are highly remunerative commercial centres filled with stores, restaurants and services, where cables are turned into works of art and towers become much more than steel and grass.

An example is the Green Corner, located in a building owned by Carlos Slim. It hosts a massive telecom switch on the last floor and has a tall telecom tower on top. There is a restaurant on the top floor whose rooftop is entirely covered by solar panels. Instead of hiding cables and equipment, they became part of the design, along with a monitor showing how many kW are being generated by the site.

This reminds us that Telesites isn’t just a towerco. But a towerco created by a King Midas whose empire encompasses virtually every industry in Mexico, including telecoms, education, health care, real estate, media, retail and financial services.

It’s unclear whether these oasis have been transferred to Telesites but in any case I am convinced that the towerco will meet high quality standards and excel at building sites.

PERMITS

Permitting is one tricky business in most countries in CALA. And obtaining municipal permits in Mexico isn’t easy.

Having been in the business for decades, I am sure América Móvil knows its way around the complex local permitting system and Telesites can count on the experience of its parent company on this matter.

RATES

As previously mentioned, Telesites is forced to publicises its terms and conditions and offer fair prices to its customers by IFETEL, in light of its preponderance in the market.

Telesites rent prices are aligned with the typical lease rates charged by Mexican towercos. In fact, in 2015, the average net monthly rent per tenant in 2015 was MX$18,600 (~US$1,050) plus land rent pass-through of around MX$10,000 (~US$570).

GROWTH

Growth is indeed the most thorny aspect of all. In fact, if on one hand Telesites might have overestimated its tenancy ratio growth as well as the demand for new sites by Telefónica and AT&T, we need to remember that Mexico still needs as many as 70,000 new sites to reach its desired coverage and enhance its capacity.

Even with the Red Compartida actually happening, we are talking about thousands of new sites needed to bring Mexico’s mobile services in line with the rest of OECD countries. And in my view, there is only one mobile network operator - for now - able to satisfy the cell site densification needs of the country. And that is América Móvil.

Far from the - sometimes abstract - dynamics of the stock market, Telesites is a tower company. And its business is to build towers in Mexico (and beyond). So far, Telesites has added 2,009 sites in Mexico in less than a year, which seems quite an impressive result to me.

There is much uncertainty about Telesites’ growth potential but I would argue that the CALA tower industry as a whole is an uncertain business, as shown by the hard times faced by Brazilian towercos after years of excitement. And Mexico is simply no different. With as many as twenty-three towercos ranging from Mom and Pop shops to listed companies such as Telesites and American Tower, the country is a complex place to do business and growth forecasts are unpredictable just like anywhere else in the region.

It must be added that Telesites is already expanding beyond Mexico, with 300 sites being built on behalf of Claro in Costa Rica and the potential to start operations in fourteen other countries in CALA, a move which could turn the towerco into the largest and most regionally widespread towerco in the region.

Telesites is likely to face several challenges along its path towards success. Regulatory limitations, competition from the best in class such as American Tower, Mexico Tower Partners and SBA Communications (outside of Mexico), scarcity of new business from the second and third operators in Mexico… However, its DNA tells me that the company has a clear strategy in mind, in spite of what analysts think. And Telesites is poised to expand way beyond Mexico, even if the terms of its growth aren’t those that the stock market necessarily expects.

What we like about Telesites

Telesites may outperform their own forecast build volumes, but that will only make their target tenancy ratio of 1.5 by 2020 even more difficult to achieve. There are few precedents of carve-out, operator-led towerco driving tenancy growth of that magnitude over their first four years of existence, in fact none that TowerXchange are aware of. There are simply not enough tenancies up for grabs in Mexico to achieve that number, and those are available will be keenly fought for in this crowded towerco market.

But this doesn’t mean to say that we think the Telesites is a bad idea or a bad investment. A towerco adding 0.05 tenants per tower per year in investible markets can still be a bankable proposition. By 2020 Telesites could have a tenancy ratio over 1.2 and a footprint in half a dozen or more CALA countries. América Móvil is the most credit worthy tenant in CALA, and Telesites are optimally positioned to become their supplier of choice. The fundamentals of the tower business hold true: this is a growing infrastructure business, built on a proven business model, with long term contracts securing recurring revenue over a ten-plus year horizon. What’s not to like?