A culture of infrastructure sharing has existed in Poland since 2011 when T-Mobile and Orange signed a 15 year deal to share radio access networks. Fast forward to 2016, and the joint venture (JV) appears to be in danger of collapse. There is speculation that one or both of the parties may want to exit the agreement and sell some of their towers to a third party. Drawing on insights gleaned from the Poland roundtable at the TowerXchange Meetup Europe 2016, moderated by Darragh Stokes of Hardiman Telecommunications, let’s explore the JV in more detail and take a broader look at the structure of Poland’s tower and mobile market.

Poland is seen as one of the most investible economies in CEE with real GDP growth expected to be 3.6% YOY in 2015, forecast to rise to 3.9% in 2016, giving GDP per capita of €11,262 in 2016, according to BMI. So how investible is Poland’s tower market, and what are the prospects for towercos to enter the market?

Polish telecoms market

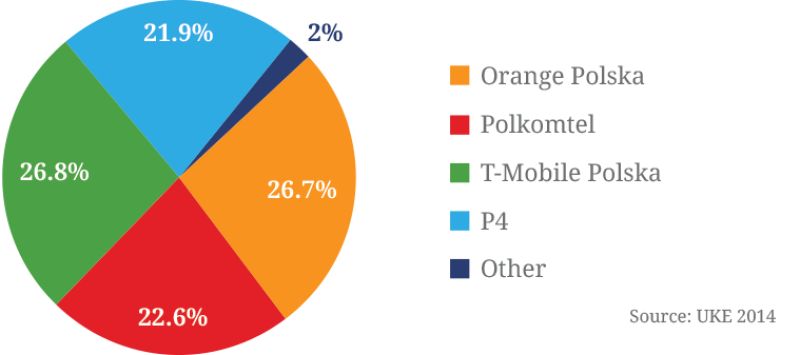

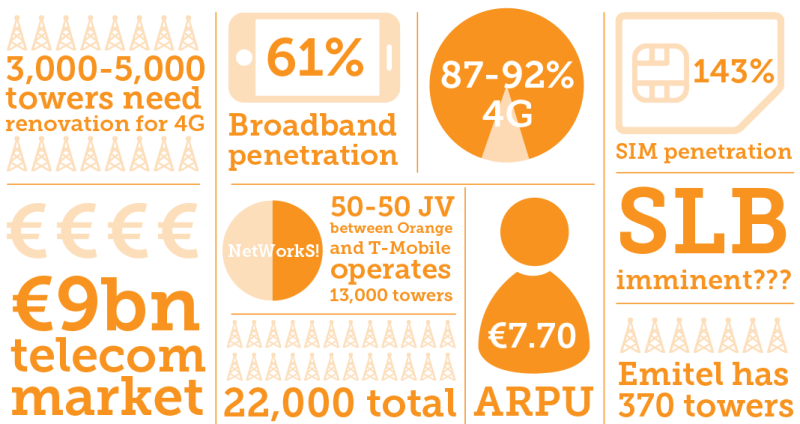

The Polish mobile market is attractive to towercos because it is relatively evenly balanced between four players – T-Mobile, Orange Polska, Plus and Play, although at the end of 2014 Polish regulator the UKE had licensed seven MNOs and 20 MVNOs. In 2014, the entire telecommunications market in Poland was worth PLN 39.21 billion (around €9bn).

Over the past few years there has been a steady decline in revenue from fixed line and mobile telephony (According to Analysys Mason ARPU had declined to PLN 32.3 / €7.70 by 2014), which has been compensated for by a rapid increase in income from Internet services. In 2014, the Polish Internet market grew by more than 11.5% compared to the previous year. According to GSMA Intelligence (Q4 2015), SIM penetration is at 143% with mobile broadband penetration at 61% in a 38.6mn population country.

Orange and T-Mobile joint venture

In July 2011, Orange and T-Mobile signed a 15 year deal to share their radio access networks. A JV infraco called NetWorkS! was set up by the two operators to cover the management, planning, support, development and maintenance of their base stations and infrastructure. Orange and T-Mobile have continued to manage their core networks and frequencies.

The 50/50 JV was set up with the intention of enhancing network performance, cutting costs and preparing the shared network for LTE. At present, combined the two operators own about 13,000 towers and rooftops. There is a significant amount of parallel infrastructure that is held in common between them. Over the next few years, the MNOs plan to eliminate some duplicate base stations and re-build and refurbish a significant proportion of their towers to use recently acquired 4G spectrum.

3G coverage is almost complete in Poland, while Orange claim 87% 4G coverage and T-Mobile is forecasting 92% 4G coverage by the end of Q2 2016. According to TeleGeography, recipients of new 4G spectrum have two years to cover 1,149 regions with no internet access or access at speeds of below 10Mbps. They must also cover 1,053 towns of up to 30,000 inhabitants within three years and 91 towns of between 30,000 and 50,000 inhabitants within four years.

Polish mobile subscriber market share

Polish tower market

There are roughly 22,000 towers in Poland. Orange owns roughly 7,000 towers, while T-Mobile and Plus have 6,400 and 4,000 towers respectively. There is currently one independent tower company in the country – Emitel – which owns about 370 towers, most of which are broadcast facilities. TowerXchange is tracking one further startup towerco in the country, details of which have yet to emerge into the public domain.

There is speculation that T-Mobile and Orange may be open to selling some of their towers to an independent tower company. They have different values – T-Mobile is strongly focused on cutting costs, while Orange is more focused on expansion. In addition, the JV hasn’t operated as efficiently as some might have hoped. This has led some analysts to conclude that the JV is ill-fated, and that one or both of the MNOs may be interested in divesting towers in the future.

There is speculation that T-Mobile and Orange may be open to selling some of their towers to an independent tower company. They have different values – T-Mobile is strongly focused on cutting costs, while Orange is more focused on expansion

Preparing for LTE

In October 2015, the Polish telecom market regulator UKE launched an auction for 19 frequencies in the 800 MHz and 2.6 GHz ranges. Frequency bands offered by UKE had been freed after the switch to digital TV from analogue services. Poland, as the rest of Europe, intends to allocate these frequencies to the development of fast mobile Internet.

The auction came at an opportune moment – had the government restricted Internet services to the current frequencies, the operators would have struggled to provide good quality services within two years.

Since the frequencies were announced, a number of broadcasters have expressed an interest in the multiplex licenses (multiplex five and six). DDT channels in Poland are still growing in terms of ownership and ad revenues, and there has been considerable interest in the licenses. Over twenty channels have applied for the licenses so far, which will be allocated shortly in a beauty contest.

It is estimated that between 3,000 and 5,000 towers will need to be renovated to support the rollout of 4G. Ultimately, the success or failure of the rollout will be determined by the willingness of the MNOs to share resources.

The format that this sharing will take has yet to be decided, but there are a number of avenues that the MNOs can explore. They may choose to increase the number of Points of Presence (POPs) on their towers by installing 4G antennae across their existing portfolio. Alternatively, they may opt to retro fit their towers with multi band antennae.

Operators are also exploring the possibility of using small cells, street furniture and fibre to provide fast broadband to customers. Emitel has already embarked on a programme to add fibre to its towers, and other operators are likely to follow suit. Converting street furniture presents a bigger challenge and it is not always immediately clear who actually owns the assets. Despite this, the MNOs have already approached some municipalities in the country to set up pilots.

Conclusion

The number of Fibre to the Home (FTTH) network connections is expected to grow rapidly in Poland over the next few years. Over five million connections are expected to be added over the next four years. To give a sense of the increase, Poland only had 77,000 FTTH lines at the end of 2013. Given these facts, it is hardly surprising that Polish MNOs are focused so strongly on delivering 4G services. The rollout of a nationwide LTE network over the next five years – as mandated by law – will create many opportunities for tower companies and equipment providers.

Then there is the Orange and T-Mobile JV. If the JV dissolves, it is likely that one or both operators may wish to sell some of its towers.

The prospects for increased competition in the tower market in Poland are good, so watch this space.