Mobile market overview

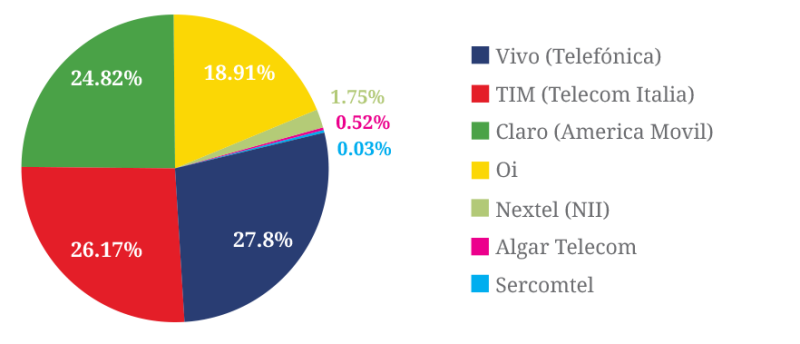

Brazil had an estimated population of 208.7mn people and 248.3mn mobile subscriptions at the end of 20151, giving a mobile penetration of 119% - the fifth highest level of penetration in South America. Around 74% of subscribers have a pre-paid account, which ranks 7th amongst the South American countries. Peru ranks the lowest with 65% pre-paid subscribers. There are seven mobile network operators (MNOs) serving the Brazilian market (See figure 1), with four large operators serving more than 45mn subscribers each and three smaller operators with a combined subscriber base of less than 6mn. Vivo (Telefónica) currently holds the largest market share with 69.0mn subscribers closely followed by TIM (Telecom Italia) 65.0mn, Claro (América Móvil) 61.6mn and Oi with 47.0mn subscribers. The smallest operator Sercomtel, had fewer than 65,000 subscribers at the end of 2015.

Key mobile developments

Brazil has an average mobile penetration for the South American region, surpassed by Suriname (175%), Uruguay (159%), Chile (146%) and Argentina (144%). Brazil’s national subscriber base has grown rapidly in recent years, doubling since 2008 to reach a record high of 275.5mn in Q1 2015. However, subscriber numbers reversed as the year developed and an estimated 10% reduction in subscribers was observed across the Brazilian market, with the reduction felt relatively evenly across the four large operators in relation to their market share. The fall in subscribers is reportedly a result of the operators’ efforts to disconnect inactive or non-paying users, as well as a tightening of the credit policies available to customers. The subscriber numbers of the three smaller operators were reportedly unaffected in 2015. Subscriber numbers are expected to remain stagnant through 2016 before increasing in 2017.

3G services were first rolled out in Brazil in Q4 2007 when Vivo and Claro introduced the technology into a small number of key states. Following the official 3G auction in December 2007 for the rights to offer UMTS services in the 2100MHz band, TIM, Algar, Sercomtel and Oi rolled-out a 3G service offering within a year of purchasing the licenses. The remaining operator, Nextel waited until 2010 to purchase the required licences and began offering a 3G service in the second half of 2012. Vivo, Claro and TIM expanded aggressively into the 3G market and the three operators held 95.6% of the 3G market share after 4 years (Q4 2011). This figure has fallen to 82.8% following the growth of Oi in this area.

Mobile subscriptions- market share

Rollout of 4G

The announcement of plans to auction licences for 4G frequencies in the 450MHz and 2.5GHz bands in June 2012 was met with significant resistance from the incumbent operators who believed the auction was premature. The auction went ahead nonetheless and Vivo, TIM, Claro and Oi all successfully purchased licenses at the auction, however desire for the 450MHz band was significantly less than anticipated by the regulator. In response to this, the regulator stated that the winners of the lucrative 2.5GHz bands were also required to take the 450MHz bands for deployment in rural areas.

The four operators faced new competition in the 4G market in the major cities of São Paulo and Rio de Janeiro from pay-TV and Video-on-Demand service providers Sunrise Telecomunicações and Sky Brasil Serviços who also successfully acquired 4G licences, as well as from Nextel who rolled-out their service offering in Q2 2014. As of the end of 2015, GSMA estimates that there were 25.4mn 4G subscribers in Brazil, with Vivo and TIM leading the way in terms of subscribers with 9.5mn and 7.1mn respectively.

Operator activity

Vivo (Telefónica) launched its mobile service offering in Brazil in 2003 as a 50-50 joint venture between Portugal Telecom (PT) and Telefónica Móviles and was the largest mobile operator in the country at the time with a subscriber base of 17mn. Vivo was the first operator to reach 1mn 4G subscribers and has continued to maintain the largest subscriber base in the 4G market (Q4 2015).

TIM (Telecom Italia) is Brazil’s second largest mobile operator by subscriber number and has featured in the mobile market since 2002. TIM has struggled to withstand intense market competition in recent years, and since 2013 increasing reports of merger and acquisition activities involving TIM have been recorded.

Claro (América Móvil) entered the Brazilian market through the joining of five companies owned by parent company America Movil in 2003. Claro currently services the highest number of 3G subscribers in Brazil at 49.7mn (Q4 2015) and the third largest number of 4G subscribers - 4.5mn.

Oi entered Brazil’s mobile market in June 2002 as the country’s first GSM operator. Oi has grown mainly through acquisition, most noticeably acquiring rival telecoms group Brasil Telecom (BrT) in 2008, to achieve the fourth largest market share by mobile subscribers.

Nextel, Algar Telecom and Sercomtel service the remaining 2.1% of mobile subscribers in the Brazilian market. Algar Telecom and Sercomtel have diversified their service offering by also supplying pay-TV services whereas Nextel, the largest of the three operators, is reportedly up for sale following its parent company NII Holdings experiencing financial difficulties in 2014 and 2015.

Regulation

Following Constitutional Amendment 8/1995, which removed exclusivity in the operation of public services to state managed companies, and General Telecommunications Law 1997, Agência Nacional de Telecomunicações (Anatel) was formed to regulate the Brazilian telecoms market in 1997. Anatel is entirely independent from the Brazilian government, both financially and administratively. Anatel regulates the entire telecommunications industry, including radio spectrum, merger and acquisition activity, conflict resolution amongst operators, violation prosecution and product certification. The Agency’s aim is to support the development of Brazilian telecommunications and bridge the regional inequalities.

Brazil’s telecommunications infrastructure fell behind the U.S. and Europe in the 1990s due to a lack of investment, however investment has steadily improved and the main cities now boast comparable, modern technologies. This vacuum of investment towards the larger cities has left regional imbalances across the country with the north and north-west regions lacking even basic telecommunications systems in some areas. Anatel has attempted to combat these inequalities through a number of initiatives including packaging together the purchase of 450MHz spectrum with sought after 2.5GHz spectrum to help drive rural coverage.

The tower sharing market

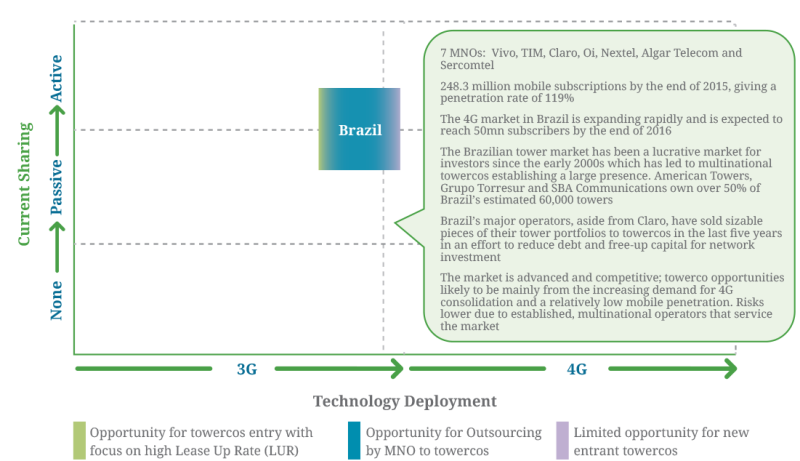

The Brazilian tower market has been a lucrative market for investors since the early 2000s which has led to multinational towercos establishing a large presence. Approximately 35,000 of the estimated 60,000 towers in Brazil are owned by towercos, with the vast majority of these towers owned by three towercos: American Tower, Grupo TorreSur and SBA Communications.

American Tower first entered the Brazilian towerco market in 2000 and has grown largely through acquisition, including the purchase of 6,400 towers from mobile operator TIM in 2014, to reach its current total of just under 19,000 towers. SBA Communications entered the market in 2012 after an acquisition of 800 towers from Vivo. SBA has since rapidly developed a significant presence in Brazil and today own 7,000 towers. Grupo TorreSur is the third largest towerco in Brazil by number of towers (6,500) which includes 1,641 towers acquired from Oi in 2014.

The remainder of the towerco owned infrastructure in Brazil is shared between towercos of varying size and global presence. Telxius, a global company created by Telefónica in Q1 2016 to manage selected infrastructure assets, owns 2,500 towers. Highline do Brasil owns just under 200 towers after initially starting out as a build-to-suit company in 2013 and an estimated 3,387 towers are owned by a number of small independent towercos.

The prominence of towercos within the Brazilian market has been assisted in recent years by a shift from operators who no longer see the ownership of their tower portfolio as a core element of their business. Brazil’s major operators, aside from Claro, have sold seizable pieces of their tower portfolios to towercos in the last five years in an effort to reduce debt and free-up capital for network investment.

Conclusions

With the largest population in South America (208.7mn people) and the fifth highest mobile penetration (119%), there is considerable room for subscriber growth in the Brazilian mobile market. 4G services have been launched and consumer appetite is growing rapidly with 4G subscribers expected to reach 50mn by the end of 2016.

The presence of four multinational MNOs within the market has encouraged competition and innovation and subsequently ensured that the Brazilian market has matched the roll-out of speeds and technologies seen in equivalent developed countries. There are also three smaller operators that concentrate their services mainly within the larger cities of Brazil. Nonetheless, the current market structure has failed to bridge the regional imbalances across the country leaving certain regions lacking even basic telecommunications systems. Increasing reports suggest that the market structure may change as the fourth and fifth largest operators, TIM and Nextel, are reportedly up for sale.

After a period of concentrated tower transactions which has seen many of the large MNOs significantly reduce their tower portfolio and a number of towercos establish a significant presence in the market, both the MNOs and towercos are now expected to consolidate their positions leading to a reduction in the number of tower transactions.

1. GSMA