An increasing number of towercos are viewing the small cell market as a key area for growth, especially in developed markets where operator focus has shifted to urban infill and densification. With 2015 seeing small cell equipment sales pass the US$1bn mark for the first time, technological advances making multi-operator neutral host small cells readily available and market forecasts that by 2020 over 80% of small cell deployments will involve third parties – TowerXchange spoke to Alan Law, Chair of the Small Cell Forum to better understand the role that towercos could play in this rapidly expanding industry.

TowerXchange: Please can you give us a background to Small Cell Forum

Alan Law, Chair, Small Cell Forum:

The Small Cell Forum has been around since 2007. In its initial incarnation it was known as the Femto Forum and at that time it was primarily focused on the residential market and creating an industry vehicle to drive chipset availability for this whole new market potential. The starting question for the industry was “If I can buy a WiFi access point for a few dollars, why can’t I buy a cellular access point for the same sort of price and what is it that needs to be done in order to facilitate that?”

We have come a long way since then. We started focused solely on residential and then as a body we have expanded to cover use cases in enterprise, urban and rural and remote locations. With this broadening of scope, the “femto” name wasn’t so appropriate any more – femto is just one category which was suited to residential. So we needed a broader name for the forum and it became known as the Small Cell Forum.

Our specified goal is “solving the HetNet puzzle” which is really about driving the scale of adoption of small cell technology within the industry and the ecosystem. A lot of what we do is about addressing gaps in understanding and standards that exist that can be barriers to deployment. As we address each of these barriers the deployment path becomes smoother.

We have membership covering everything from chipset suppliers, component suppliers, OEMs that bring access points together, system integrators, test providers and operators – the whole ecosystem is represented.

TowerXchange: We hear lots of definitions surrounding small cells and DAS with many of these boundaries between systems blurring, how does the Small Cell Forum define the small cell market?

Alan Law, Chair, Small Cell Forum:

“Small cell” is an umbrella term for operator controlled low powered radio access nodes including those that operate in licensed spectrum and unlicensed carrier grade WiFi bands. Small cells typically have a range from 10 metres to several hundred metres and the types of small cells include femtocells, picocells and microcells (those groupings broadly increasing in size). Whilst this is the latest definition that we have, the definition is now certainly blurring with the adoption of new technologies and capabilities such as virtualisation. As you start to virtualise a small cell, the physical network equipment becomes quite similar to DAS (distributed antenna system) in the sense that it is an amplifier and a radiating element that you then seed with cellular base pan processing which is hosted somewhere else in your network through software. When you virtualise in that way you can conceptually think about it as a tightly integrated DAS and base station infrastructure- it’s similar in an architectural sense.

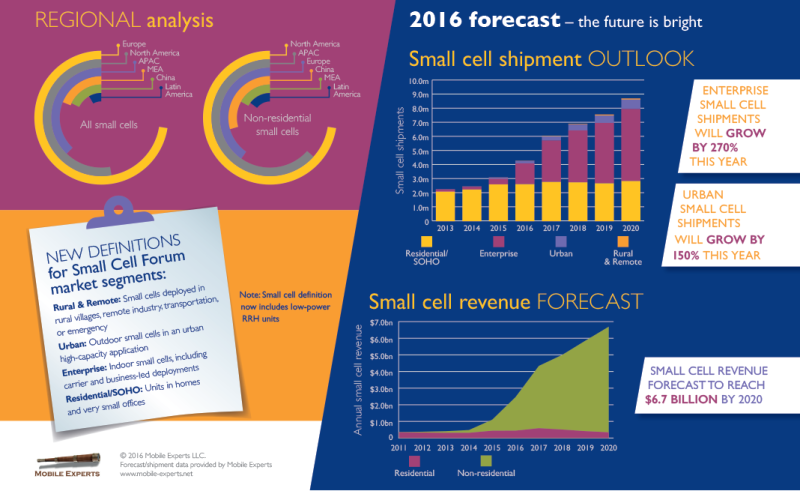

In the sense of the environments that we look at, we do have these categorisations of Residential and SoHo (small office, home office), Enterprise, Urban and Rural & Remote. The whole idea is that forum covers the broad spectrum of deployment scenarios which have been organised on an environmental basis.

TowerXchange: Can you tell us a little more about the Small Cell Forum’s key areas of work?

Alan Law, Chair, Small Cell Forum:

The Small Cell Forum has effectively got six prongs to its work program which look at new technologies that we think will be quite transformational. In the enterprise and smart enterprise space we have a workstream looking at virtualisation, another looking at SONs (self organising networks) and HetNet and increasingly we add in what we call automation on to that. The difference with automation really being the fact that it covers everything from the workflow management and the site instructions to the technology, configuration, set-up, maintenance and optimisation piece. We’re also working on license exempt technologies (in the sense of understanding what that means for the small cell densification story) as well as working on multi-operator, neutral host systems and 5G, M2M and IoT.

We’ve created a model where we have champions for each of these activities where we assign both an operator lead and a vendor lead. This gives us a balance of what an operator wants to see and what a vendor thinks needs to happen and so we end up with a balanced output. It makes sure anything that we’re doing has a strong customer focus whilst also being underpinned with the realities of what can actually be delivered.

TowerXchange: How is the work communicated to the community?

Alan Law, Chair, Small Cell Forum:

Throughout the year we have various releases. Whilst we have no fixed schedule, we would expect to have at least one release per year. 2016 is unusual in that we are likely to have three releases. This is a bit unprecedented in terms of output but is a great testament to the activity in the forum and how the work is being distributed amongst the membership. It is also indicative of the fact that so much is happening from a technological standpoint.

We presented the smart enterprise release at the Mobile World Congress, we plan to release our next piece on HetNet foundations at our London event, and then we’ll have another release later in the year which will include lots of the work we’re doing on virtualisation. It is an incredibly busy year but it is great content that is coming out which we think will help the market to continue to grow significantly over the forthcoming period.

TowerXchange: When you speak about the size of the small cell industry and the sort of growth that is expected what kind of numbers are we looking at?

Alan Law, Chair, Small Cell Forum:

An important milestone for the industry was back in November last year where we released what we called our “Crossing the Chasm” report, the messaging behind the report was “we’re on the hockey stick of growth now’. There have been, to date, lots of projections which get changed due to all kinds of circumstances -there’s always the fear that the growth will start “next year”, with that “next year” continuously being pushed out. Our Crossing the Chasm report states that we think we are already on the growth curve, we have put the stake in the ground and we have the confidence in the statistics to believe that.

We released our latest small cell deployment numbers for Mobile World Congress [all these release documents are free to download on the site www.scf.io]. There have been 13.3mn small cells shipped to date making it a substantive market in terms of where it stands. In the sense of understanding how the market has developed to get to that, during course of 2015, enterprise shipments doubled, urban shipments grew 280%, rural and remote grew 70% and residential (the most established market) grew 20% - there was significant growth in each sector which is encouraging.

Another important milestone during the course of the year was that we crossed US$1bn of small cell equipment revenue, that was just for equipment and so doesn’t include any of the extra market opportunity around installation and site acquisition. But in the sense of where the numbers are going in the shorter term we’re looking at 270% growth for enterprise during the course 2016, another 150% growth in the urban sector and if we cast eye further ahead we’re anticipating that small cell equipment revenue will be around US$6.7bn by 2020 – growing from the billion of last year (see figure one).

TowerXchange: As the market matures, are we seeing consolidation of the equipment suppliers whose equipment sales are accounting for the numbers in these statistics?

Alan Law, Chair, Small Cell Forum:

I would say there is still a broad market, there has been a degree of market consolidation, but that is more due to small players being acquired by big companies such as CommScope and Cisco, and the Nokia-Alcatel Lucent merger. There is a degree of consolidation but there is still a lot of competition and we continue to see new entrants as well entering the market.

TowerXchange: Is the growth that we’re seeing across the sectors worldwide or do you see bigger growth in some regions that others?

Alan Law, Chair, Small Cell Forum:

We’re seeing the split across different regions being quite varied, the largest regions being Europe, North America and APAC (figure two). However, there is significant growth globally. For example, the smallest region at the moment is LatAm but if we look over the course of the last year it grew 500%; even though its a late blossomer it’s working hard to catch up! Similarly, when you look at the numbers for China, they are currently very modest, but there are certain deals in place that if we look into 2016, China will most probably swamp everybody by the end of the year.

There is a need for small cell technology internationally and there are tremendous opportunities. A good reference is the presentation Reliance Jio (one of the Indian operators) gave at our Dallas event. In terms of deployment over the next two years they are looking to create 100,000 macro sites, 300,000 small cells and 500,000 WiFi access points; this is nearly a million assets being deployed in two years which is quite incredible in the sense of the numbers.

TowerXchange: With such big numbers being forecasted for deployment how do you envisage that deployment will be rolled out? Who will be the key stakeholders and what business models make most sense?

Alan Law, Chair, Small Cell Forum:

We don’t have all the answers right now but let me give you some statistics. Our Crossing the Chasm report contains research from Rethink Research who estimate that by 2020 only 20% of small cells will be fully deployed and managed by MNOs; what that means is that for 80% of these future small cells there will be some other party involved in the deployment and management of those assets. There’s a good chance that towercos that are building this infrastructure can have a role in that. A significant new potential opportunity is up for grabs and it’s a massive growth area.

By 2020 only 20% of small cells will be fully deployed and managed by MNOs; what that means is that for 80% of these future small cells there will be some other party involved in the deployment and management of those assets. There’s a good chance that towercos that are building this infrastructure can have a role in that

In release six there’s a document which might be interesting to the TowerXchange community called “Market drivers for multi-operator small cells”. Within the report it takes a look what the market might look like, both with and without multi-operator neutral host small cells. It estimates that for the enterprise vertical the multi operator market is 91% bigger than without and in public spaces it is double the market with multi-operator than without. Hence why in the forum we have theme looking at multi operator and neutral hosts as we believe it will be one of the key requirements of the future.

TowerXchange Has there been reluctance in the past to look at multi-operator, neutral host solutions and if so, why?

Alan Law, Chair, Small Cell Forum:

To some extent, yes, but technology has clearly got better with time and it continues to improve which makes it easier to do multi-operator and do it better. There is also an appreciation of changing market conditions, in the sense that for many operators, coverage is quite similar and no longer a differentiator. Operators always want to differentiate what they can do in their market to gain customers and customer loyalty. They can differentiate either through upper layer services or the radio capabilities that they have in their network. One of the newer changes which is having an impact is with concepts such as mobile edge compute and virtualisation; these enable operators to differentiate even over common sets of infrastructure. That makes it easy to support some of the business cases for shared infrastructure going forward.

In our questionnaire that went out we asked MNOs what they considered to be the biggest concerns surrounding multi-operator deployment. The three highest scoring concerns were upfront capex and return on investment; monetisation; and enabling competition - over 50% of respondents gave those as their top three. Our work programs seek to address these concerns; looking at the right technological deployment and solutions that will help address the capex and ROI issue; developing new service enablement supporting the monetisation piece; and working on changes in virtualisation that will help to ensure that competition remains between the operators.

TowerXchange: When speaking of challenges, what barriers exist around the physical deployment of small cells?

Alan Law, Chair, Small Cell Forum:

There are always the classic challenges around gaining access to a site, to power, and to transmission to support any small cell deployment. The good news is that there are a number of companies that own worldwide international portfolios of street infrastructure assets and advertising hoardings (such as JC Decaux) who are starting to make sure that their new street furniture is equipped with space to allow small cells. You see special tram stops in the Netherlands that have been created to host small cell infrastructure, there are smart advertising hoardings being developed where small cells can sit at the back and we have seen solutions on street lighting in China.

This type of infrastructure is a good testament to maturity of market; people are not debating whether to use small cell technology, they are asking how to deploy it and how to do it at scale – we‘ve moved away from the “why” and on to the “how”. This again was an interesting part of the Reliance Jio presentation back in Dallas. With all of those hundreds of thousands of assets they are working to deploy, the only way that it can be achieved is through automation on every level. The company has worked very hard to automate every process which then allows them to scale to the thousands of deployments they need to make every month in order to hit targets.

TowerXchange: When we move away from the urban side and look at the enterprise side, where have you seen the biggest uptake and how important are multi-operator small cells?

Alan Law, Chair, Small Cell Forum:

In public spaces you don’t have the degree of control over which operators are in use in a particular area and so there will be a strong aspiration to have multi-operator deployments.

When it comes to enterprises, a lot of the drive for technology is to allow greater efficiencies to be delivered and to have a greater level of flexibility. The beauty of small cells is that it allows great fluidity in your business, with opportunities to ramp up and scale down very quickly in order to address demands that are being placed on the company. Having solutions that are also very quick and rapid to deploy (which is what you get out of small cell technology) also helps that agility. If I need to send 50 people to a site, I can equip them with the small cell infrastructure they need to go with them. Installing it means they can continue to work in the way that they naturally would in the office in that same agile way; similarly when they move on, it’s very easy to remove again.

There is tremendous flexibility that is coming out of these new capabilities and technologies and it’s happening not only in the sense of workplace improvements but also in the way that things such as retail are transforming. There is a real change in consumer behaviour – if you go into a shop and they don’t have the item in that you’re looking for, you can go online and order it there and then. People often think of the increasing demands on mobile infrastructure in terms of increasing social media levels, but this is also an important part of the equation – adapting to consumer and workplace behaviour with the view of selling more goods or driving better working efficiencies.

TowerXchange: How has the Small Cell Forum engaged with the towerco market in the past and how to you foresee this changing?

Alan Law, Chair, Small Cell Forum:

We’ve had variable degrees of interaction with towercos in the past and count some of the larger companies (such as Arqiva and Crown Castle amongst our members). As we advance into a new world where there will be a bigger focus on neutrally deployed assets, I think there is even more potential for towercos and we hope to work closely with the market to improve synergies.