Since Free Mobile burst onto the French MNO market in early 2012, the incumbent operators have struggled to retain market share. As they battle with lower ARPUs, higher need for capital investment and increased market competition, French towercos are seeing an opportunity to help release cash, reduce opex and build new, fit-for-purpose networks for their customers.

France is a highly developed Western European market, a founding member of the European Union and is one of the top ten global economies. While it’s easy to assume the ‘data boom’ has already taken place, there remains significant growth potential in the French tower market, both through urban infill and improving rural services. France is also at the forefront of the drive towards the Internet of Things, which will substantially change both the way mobile communications are consumed and the way they are delivered. In a market where operators are jostling for market share and towercos are taking very different approaches to growth, we assess some of the drivers which have brought the market to its current point, and evaluate how it may develop over time.

The French population is currently 64.09mn making it the third biggest country in Europe. Offering GSM services since 1996, there are now around 64.4mn subscribers. Despite struggling to recover from the recession of 2009, the French economy is now slowly coming into line with European growth levels, with the slow growth of 0.4% in 2014 unlikely to be replicated in 2015.

3/4G rollout is well underway with 68% of subscriptions including mobile broadband and all four MNOs in France rolling out their 4G networks since 2012.

French MNOs

The French market currently supports four national MNOs, although rumours of market consolidation have been rife for several years. From Orange, one of France’s most established brands and successful exports, to Free Mobile, the newest market entrant, the French market remains dynamic and highly competitive.

Orange

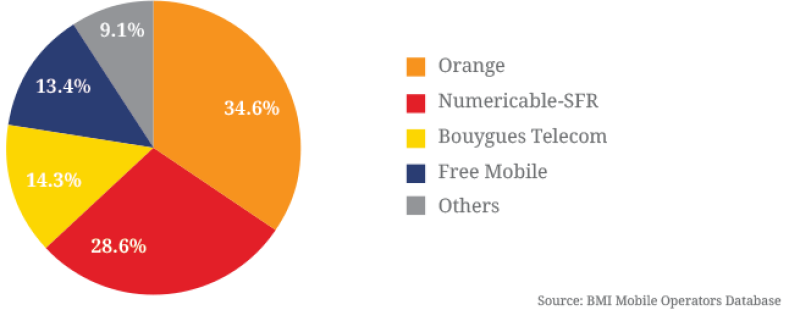

Orange is France’s oldest and largest MNO and currently owns 34.6% mobile market share. With origins dating back to the formation of France Telecom in 1988, Orange is a highly recognisable French institution, operational in various forms in 27 countries worldwide, Orange is listed on the Paris Stock Exchange, with a current market cap (at 20.9.15) of €37bn. The state owns 25% of the company, 13.4% directly and 11.6% though BpiFrance, the state-owned investment bank. The remainder is in free float on the Euronext Paris market and the New York Stock Exchange, with no other shareholder owning a stake greater than 5%.

In June 2015 Orange’s Fitch rating was upgraded from Negative to Stable, as a result of both Orange’s moves to reduce debt and the growth potential identified in the French market.

Orange lost out in terms of market share when Free Mobile entered the market, losing the most market share to the new entrant. Although competitive pressures will continue to keep tariffs down and force Orange to maintain market share through capex-intensive projects, the market does seem to have stabilised since Free Mobile’s launch in January 2012 and we believe that Orange’s faster deployment of 4G networks should provide an important point of differentiation in the market.

Despite the fact that capex is likely to remain high due to upcoming spectrum auctions, fibre rollout and their commercial strategy to lead the market in mobile data provision, Orange is targeting gross cost savings of €3bn from its transformation programme over 2015-2018.

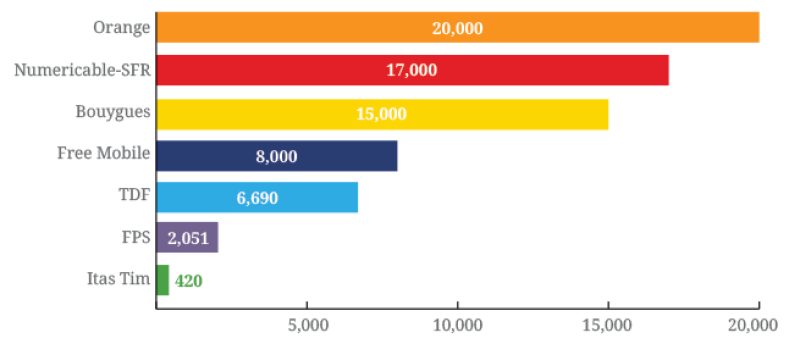

In 2014 Orange spent €5.6bn (or 14% of revenues) on capex, a number which is likely to increase in the next two years before it can be reduced. Therefore they need to explore different ways to raise cash and reduce opex to support this. Orange does plan to release cash through the prospective sale if its 50% stake in EE in the UK, which should raise around £3.4bn plus a 4% stake in the acquiring party, but there is also a significant asset sitting on their balance sheet in the form of around 20,000 telecoms towers, the sale of which could not only release well in excess of €2bn but which could also help them to stabilise opex for the next ten plus years.

Mobile subscription market shares, Q115

Numericable-SFR

Founded in February 1987, SFR also has a long history in the French market and offers services in both fixed line and mobile telephony. Originally founded as an arm of Vodafone in France, in April 2011 Vodafone sold their 44% stake in the company to media giant Vivendi, who owned the company with Altice until Q2 2015. With 28.6% of French market share, they are currently the second biggest MNO in France.

In April 2014 Vivendi’s management accepted a takeover offer for SFR from Numericable’s parent Altice. Under the terms of this deal, Altice paid Vivendi €13.5bn in cash and Vivendi took a 20% stake in a newly formed company, Numericable-SFR, of which 60% was owned by Altice and 20% publicly listed in Paris. Vivendi exercised its option to sell its 20% SFR-Numericable stake in February 2015, with half of its stake being sold to Numericable-SFR for €1.947bn in cash in February 2014 and an agreement for the remaining shares to be acquired by Altice France no later then 7 April 2016.

Notably, Vivendi’s withdrawal from SFR came only two months after SFR signed a network sharing deal with their competitor Bouygues Telecom. The agreement, which will see the two operators share some 11,500 towers in low-population areas, should save SFR around €200mn and Bouygues around €100mn per annum, a move necessitated by the price war initiated by Free Mobile’s entry into the market in 2012.

Between them, SFR and Bouygues Telecom currently have around 18,500 mobile towers in the underserved areas covered by the network sharing agreement (representing 80% of French territory and 57% of the population), necessitating the decommissioning of over 7,000 towers, as well as further build to suit in areas which are inadequately served by either network. Once the new network configuration is complete, each company will assume responsibility for part of the territory on behalf of both parties.

Between them, SFR and Bouygues Telecom currently have around 18,500 base stations in the areas covered by the network sharing agreement (representing 80% of French territory and 57% of the population), necessitating the decommissioning of over 7,000 towers, as well as further build to suit in areas which are inadequately served by either network

Bouygues Telecom

Bouygues, a giant in both the French telecoms and construction markets, is the third biggest operator in the French market, with 14.3% market share. The company is listed on Euronext Paris exchange and is a blue chip in the CAC 40 stock market index. Founded in 1952 by Francis Bouygues, since 1989 it has been led by his son Martin Bouygues who has overseen the expansion of the company, and launch of Bouygues Telecom in 1996.

On June 21 2015, French Sunday newspaper Journal du Dimanche reported that the owner of Altice, telecommunications billionaire Patrick Drahi, had offered more than €10bn to buy Bouygues Telecom, the assumption being that he could merge the company with his existing asset Numericable-SFR to jump straight to the number one market position. However, the offer proved unpopular with the French government and on June 23 the offer was rejected by Bouygues, citing the significant growth potential it sees in the French market. The move surprised many, as Drahi’s price tag was considered to be a generous valuation – roughly twice that of many estimates.

Bouygues’ ownership is currently dominated by the Bougyues family themselves, with 20.9% ownership of capital and 27.3% of voting rights, the remainder is split between Bougues employees, who own 23.3% of capital, 19.2% of capital is owned by French investors and the remaining 36.6% is owned by foreign investors in the company.

Free Mobile

Arguably the most disruptive force in the French mobile market in the last five years, Free Mobile has quickly reached 13.4% of market share since its launch in January 2012. Owned by French entrepreneur Xavier Nel, who also co-owns French newspaper Le Monde and Monaco Telecom, Free Mobile’s model relied on low numbers of physical outlets, low-cost offers and non-handset deals to undercut the existing market players, with Nel claiming the incumbent MNOs saw their subscribers as ‘cash cows’ rather than customers.

Originally reliant on France Telcom for around 70% of their network, Free Mobile has been building up their own network coverage and now owns around 10,000 towers in the country. This leaves them some 7,000 short of the 17,000 sites TowerXchange estimates MNOs need for full coverage of the French territory, and makes Free Mobile attractive prospective tenants for towercos in the market.

France’s towercos

Given the rapid change taking place in the French market, it’s unsurprising that the towerco market has recently enabled smaller players to enter the market and grow rapidly. With Free Mobile’s appetite to grab market share, Numbericable-SFR and Bouygues’ network redesign and Orange’s need to reduce opex in favour of high capex deployment to maintain their position as market leader, both the reduced opex offering and the potential to release cash through the sale of towers could prove highly tempting to France’s MNOs.

Estimated tower ownership in France

TDF

TDF is the most established player in the French tower market, founded in 1975 as a public-sector broadcasting operator and becoming part of France Telecom in 1991. From 2002, the when France Telecom first sold off 64% of the company, TDF has been through several acquisition processes, most recently being acquired in 2015 by Brookfield Infrastructure Group, Public Sector Pension Investment Board (PSP Investments), APG Asset Management N.V. and Arcus Infrastructure Partners, valuing the company at approximately €3.6bn.

TDF provides services and infrastructure to the media, broadcasting and telecommunications sectors in France, owning and operating a national network of infrastructure with more than 6,690 multi-purpose towers and active rooftop sites, as well as 5,000 km of fibre backbone. These services drive almost 90% of the current revenues of the business, supported by long-term contracts and inflation-linked cash flows. The company expects the portfolio’s growth to be driven by ‘increasing tower deployment by mobile network operators as a result of rising mobile data consumption needs’.

Indeed, when Free Mobile entered the market in 2012, declining revenues from the existing three operators meant TDF was forced to take hit in terms of revenue from these clients, however, Free Mobile’s need for rapid market coverage worked to TDF’s advantage, and the towerco was able to offer services to all four of the French MNOs, working with them on 4G roll out and securing 35% of their overall revenues in 2012-2013 from the telecoms side of their business (the largest single contributor to Group revenue). TDF sees the ongoing data boom and the future of the Internet of Things as a significant opportunity for them to further capitalise on their network, which remains the biggest in France by some margin.

For the short term, TDF’s growth ambitions appear to be focussed heavily on the domestic French market. Despite owning assets abroad from as early as 2001, when TDF acquired a 49% stake in Digita in Finland, from 2011-2014 they divested several European businesses including Axión in Spain, Alticom in the Netherlands, Digita in Finland and Antenna Hungaria in Hungary. CEO Olivier Huart claimed this series of divestitures was made in order to pay off group debt by selling off non-core assets and refocus the business geographically.

FPS

Founded in 2012 through the acquisition of 2,166 towers from Bouygues Telecom by Antin Infrastructure Partners, FPS sees itself as offering the market an alternative to TDF. Particularly focused at first on less well-served rural areas, FPS identified Free Mobile as a potential tenant who would need to make significant headway into their rural network over the next few years.FPS has also benefitted greatly from the 15% stake retained until September 2015 by Bouygues Telecom, who remain their anchor tenant on the majority of sites. As the Bouygues/SFR network sharing deal was already under negotiation when FPS was created, the towerco is in the enviable position of being contractually protected from the worst of the potential revenue loss through decommissioning, while simultaneously being the first choice partner for network extensions and other build to suit opportunities required by the new entity.

A very ambitious towerco, with an eye on significant growth over the next few years, FPS also recently acquired Loxel, a rooftop management company, which opened up their urban network and has made a further 20,000 rooftop points of service potentially available to their clients.

Itas Tim

Currently the smallest of the French mainstream towercos, Itas Tim is still well established in the market. Launched in 2008, the Itas group focussed originally on the broadcast market and provision of active equipment to TV, radio and telecoms clients and their core business remains Digital Terrestrial Television (DTT) provision, within which a partnership with TDF allows them to cover the whole of the French territory and serve more than 11mn households.

However Itas Tim does own around 420 points of service in France and sees telecoms as an important new line of service. Their aim is to position themselves as a ‘new challenger’ to TDF and FPS in terms of market position.

What next?

Further consolidation in the French mobile market is still likely, and indeed is considered necessary by many, not least the French MVNO community, who represent 9% of the market and have struggled to maintain a competitive advantage since the arrival of Free Mobile in 2012.

Whether this consolidation happens in the short term or not, the market looks promising for independent towercos, whether because of France’s impending 4G specutrum auction, Free Mobile’s need for network expansion or Orange’s desire to increase capex spending in order to support their position in the market.

In terms of the French towercos, TowerXchange believes that there is still a significant amount of organic growth potential in the market due to the above factors. However, this doesn’t rule out the potential for a significant acquisition should a package of towers come to market. Certainly, we believe TDF and FPS would both have the financial backing to raise funds for a large-scale acquisition of >5,000 towers. Of course with both Cellnex (formerly Abertis Telecom) and Telecom Italia’s Inwit eager to prove they can close significant deals in order to justify their high market valuations, and American Tower keen to expand beyond their successful base in Germany, there is a good chance that the French market could become even more competitive than it is now.