As Build Transfer Operate (BTO) agreements conclude, Thailand appears to be on the brink of resolving long standing tower ownership disputes through the formation of what is likely to be three groups of tower companies. TowerXchange connected with AEC Advisory Co-Founder and Managing Director, Dominic Arena, who has extensive experience of working with operators, investors and government stakeholders, to understand who owns what, and what the future could hold for Thailand’s telecom towers.

TowerXchange: Please introduce yourself, AEC Advisory and your substantial experience consulting to Asian telcos, particularly in Thailand.

Dominic P Arena, Managing Director, AEC Advisory:

I am co-founder and MD of AEC Advisory; a corporate advisory firm, primarily focused on the TMT, Digital Applications and Service, Energy and Government sectors. Our clients include telcos, satellite operators, tower companies, media operators, governments and regulators, and investors.

Our services include market entry analysis, feasibility studies, restructuring, M&A advisory and post transaction support as well as policy and regulatory work with government ministries and agencies.

Our focus is the ASEAN region, but our clients are expanding our regional remit – we go where they take us. For example, we have recently been working for one of our clients in China and even as far afield as a license application in Iran.

I started in the industry 21 years ago as a telecoms engineer with Vodafone Australia and later joined KPMG Consulting in 2001 when we came to Asia to help launch a mobile operator joint venture. I’ve lived in Singapore and Thailand for most of the past 15 years, working all across Asia including in Australia with KPMG Advisory where I was the responsible Director for the telecom and media business advisory practice. Post KPMG, I was the Regional Director for BT’s consulting business across the Asia Pacific region and prior to co-founding AEC Advisory, I was the Managing Partner for Value Partners’ South and Southeast Asia corporate advisory business up to early 2014.

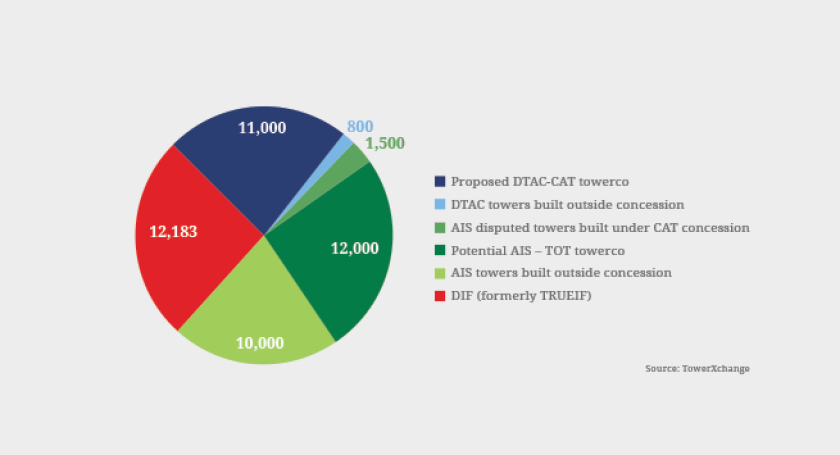

Figure one: Estimated tower ownership in Thailand

TowerXchange: Please introduce us to the telecom tower market in Thailand – it seems to be quite politicised by the BTO ownership dispute. Who owns what? What are the network characteristics?

Dominic P Arena, Managing Director, AEC Advisory:

You are correct; the Thai telecom towers market is quite complicated by the legacy BTO arrangements.

The concession / Build –Transfer – Operate (BTO) regime was adopted in the 1990’s to drive the development of the Thai mobile market. Whilst at the time it probably seemed like a reasonable approach – by offering private, efficient companies the chance to build important infrastructure using the spectrum rights and licences of the inexperienced and inefficient State Owned Enterprises – it is fair to say that the development of the mobile market in recent years has actually been hampered by this concession / BTO regime as they entered their sunset years.

Under the regime, 25 year concessions to build and operate nationwide 2G networks were given to three mobile operators – True (now owned by CP Group and China Mobile), AIS (now Temasek/Intouch and SingTel) and DTAC (Telenor plus local investors).

In return for the concessions, the operators entered into a 20-30% top line revenue share agreement with the state owned concessioners – CAT Telecom (for the 850 and 1,800MHz bands) and TOT (for the 900MHz band) and committed to return the ownership of their ‘networks’ to the state agencies.

As the concessions now expire (the only concession active beyond September is between DTAC and CAT Telecom, which expires in 2018), the suboptimal design of the BTO concept has become apparent.

People are now wiser to the long term value of network assets, especially towers and transmission, and the operators do not want to give ownership (and operational management) of their network back to CAT and TOT. The 2G active equipment itself has little value, but the towers and other passive assets still have considerable retained value. Since all the customers remain with the private operators (who have all now purchased licensed spectrum and also built some of their own towers outside of the concession regime) they want to own and operate those assets, and have argued that passive assets such as the towers did not constitute ‘network equipment’ to be returned under the BTO.

The initial response of both the operators and the state owned entities (SOEs) was enter into legal dispute processes to resolve the ownership issues, however given Thailand’s ambiguous BTO contracts, complex legal processes and many layers of telecommunications related laws (which have seen the SOEs argue for post-concession rights embedded in previous constitutions and regulations prior to the formation of the National Broadcasting and Telecommunications Commission), there was little chance of any agreements being reached for several years, leaving the entire industry in limbo with billions of dollars in stranded assets and billions more in duplicate investment being planned (and deployed).

However, over the past year consensus has been reached that a commercial solution rather than a legal solution is the only way to resolve the ownership disputes.

As a result, all operators, private and SOE, are currently negotiating and putting in place agreements to release their tower assets into joint ventures in order to avoid stranding those valuable assets and wasting more capital, while at the same time providing a means for the nearly bankrupt SOEs to enjoy some sustainable long term revenues to cover large employee welfare entitlements.

DTAC has reportedly almost reached an agreement with CAT for their 11,000 towers under concession - in return for the cancellation of all ownership disputes, wherein CAT will become the 49% shareholder in a joint venture with DTAC who will own the remaining 51% share. The Board of CAT has already acknowledged the JV as the logical way forward.

Similarly, AIS are reportedly attempting to do the same - a JV with TOT for their 12,000 towers under concession, although they appear to be a few steps behind in timing.

Last year, True listed the True Telecoms Growth Infrastructure Fund (TRUEIF, now know as DIF) on the Stock Exchange of Thailand (SET) for around US$1.8bn into which they injected all their non-concession tower and fiber assets – and they are reportedly seeking to inject their 7,500 towers under dispute with CAT into the fund in return for giving CAT a shareholding, as yet to be determined.

Therefore It is likely that we shall soon see three tower companies operational in Thailand – CAT / DTAC, AIS / TOT and DIF (already operational and paying handsome dividends of over 7%).

It’s important to recognise that each of the operators have built towers outside of the concession framework, as illustrated in figure one.

Figure one: Estimated tower ownership in Thailand

TowerXchange: The JV structure seems complicated; especially in terms of tower valuation.

Dominic P Arena, Managing Director, AEC Advisory:

Valuation of towers in Thailand is a complicated issue. It is worth scrutinising the DTAC / CAT joint venture in more detail to see the difficulties in assessing value.

Typically in Asia, US$100,000 to US$150,000 per tower is the valuation norm. Based on public information, in the DTAC / CAT venture, the entry value per tower will be well below this range even including the fact that the transaction also includes fibre transmission. Even given that CAT will receive dividends from the venture, compared to typical tower valuations the asset valuation in the JV seems low, something resembling replacement value only.

There are two main reasons why the value per tower may be lower than the norm. Firstly, DTAC has already paid for the towers once when they built them. Secondly, and this is the main reason; DTAC is the single and only anchor tenant on the towers so the tenancy ratio for valuation is likely to be 1.0.

Therefore, it looks like a ground zero valuation at the replacement cost of the towers. But also note that most of the towers in Thailand were constructed as single tenant towers due to the BTO regime, hence it is also likely that lots of improvement capex will be required for retrofitting and strengthening for multi-tenant sharing of these assets.

In addition, there is a significant overlap in tower locations. I recall 14 years ago when I came to Thailand to help launch the TA Orange network, being the third entrant using the same 1.8GHz spectrum band as the second player, their network plan largely resembled that of DTAC wherein the towers were built in close proximity.

Valuations for the towers outside the concession process, designed from the outset for multiple tenancies and built by AIS, DIF or DTAC for example, could attract valuations per tower within the normal range I mentioned.

TowerXchange: How aggressively will DIF, CAT and TOT’s towerco JVs be leasing up the towers?

Dominic P Arena, Managing Director, AEC Advisory:

There is considerable upside when you look beyond the current situation with the concession towers. There are three existing MNO players, 4G coming and a potential fourth entrant, and even 3G has only ~50% population coverage and 25-30% landmass coverage, so there will still be demand for towers beyond the roughly 47,500 towers currently in operation.

There could be a need for additional towers up to 66,000 over the next 15 to 20 years given the huge demand for mobile broadband services and lack of FTTH in Thailand.

For these reasons, I believe that the Thai tower market is at that “hockey stick” moment; poised for rapid growth.

We already see this with co-location deals that are happening. First DTAC signed a co-location deal with DIF that covers around 200 sites. Then just in mid August, DTAC signed a second deal with AIS for sharing up to 2,000 towers. The next round of tower sharing deals could be in the multiple thousands of sites.

The prevailing national tenancy ratio is low – currently averaging 1.05x tenancy ratio across all towers and all operators but higher in DIF at around 1.8. The 4G roll out on 1.8GHz next year followed by 2.3/2.6GHz in the absence of 700MHz (due to broadcasting conflicts) and the requirement to cover more of the Thai landmass will drive more sharing.

TowerXchange: Are there opportunities for international investors / towercos to get in on the Thai tower market?

Dominic P Arena, Managing Director, AEC Advisory:

I believe that yes you can get in. If you are a brand new player in the market with no existing relationships with an operator then I think it would be very difficult. But if you have prior relationships with the shareholders of the private operators and proven partnerships in other markets, then I think it is possible.

A couple of years ago, some of the regional tower companies came to take a look around but it was somewhat early and still lacking clarity on ownership of the assets, plus they may have misunderstood the mind-set of the Thai stakeholders. AIS, the largest player, has not shown interest in selling towers; AIS has 12,000 towers under concession but have 10,000 other towers that are outside the concession regime which they invested in as parallel capacity, so their mentality to date has been to spend capex (they have low gearing so can easily afford it) and keep control.

Telenor has partnered with towercos in other markets and the drivers for them are different. DTAC has 11,000 under dispute with CAT and only 800 further towers where they have guaranteed tenure as their own. Their motivation is likely less about cash and more about security of tenure and long term efficiency / opex reduction.

With regards to True, their plan is to move all their tower assets in to DIF and even to use the fund as a consolidator of industry assets. As a listed fund, their motivation is driven by fund value maximisation in which they remain the largest single shareholder.

TowerXchange: What are TOT and CAT’s drivers and obligations?

Dominic P Arena, Managing Director, AEC Advisory:

It’s important to understand that TOT and CAT’s only profitable income is the revenue share payments from the mobile operators. They are restricted in their ability to streamline their cost base and have little ability to contribute capex to future network investment. They are purely interested in long-term steady income to pay employee welfare benefits.

TowerXchange: What is the regulator NBTC’s position on infrastructure sharing – is there an established regulatory regime governing Thai towers?

Dominic P Arena, Managing Director, AEC Advisory:

To operate, tower companies need a license as a telecom facilitator. Obtaining a license is a simple process. You pay a small admin fee and that’s is it.

Tower companies are subject to infrastructure sharing regulations, which say you must share towers and also should not build near an existing tower – however such regulations to date have been challenging to enforce in the BTO transitional period.

Also, as a foreign company, any tower investor would be restricted to only owning 49% of the venture.

TowerXchange: How will future spectrum auctions and next generation network rollouts drive demand for new towers, co-locations and densification?

Dominic P Arena, Managing Director, AEC Advisory:

The auctions and next gen network rollouts can only be positive for tower companies. The bandwidths being auctioned will only generate more demand for tower sharing and new tower builds.

The capital city Bangkok accounts for 15% of the total tower stock in country and a large part of those towers are rooftops and not really leverageable for multi tenancy.

30MHz of 1,800MHz and 20MHz of 900MHz are coming to market in spectrum auctions due later this year – the latter for 2G and 3G, 1,800MHz almost exclusively for 4G. 2.1GHz is currently used for 3/4G today and 1,800MHz will be the expansion band.

700MHz still complicated – when digital TV was launched in Thailand it was put in the wrong part of the band so the ITU digital dividend doesn’t currently exist in Thailand.

Therefore we expect that 4G will go on 1,800 and 2,100MHz – that will underpin a lot of demand for additional sites and sharing. 2,300MHz and 2,600MHz spectrum is also coming in the near future.

TowerXchange: Is there a degree of parallel infrastructure in Thailand? Would decommissioning be part of a towerco play?

Dominic P Arena, Managing Director, AEC Advisory:

There is a significant degree of parallel infrastructure and I think there will be some decommissioning eventually, but we’re still in the early stages – as I said, the beginning of the hockey stick.

If we had 700MHz clear around corner we’d have more consolidation because there would be less demand for towers, but with restricted sub-1GHz (apart from 850/900MHz) and data demand growing at over 35%, I anticipate no huge consolidation of parallel infrastructure.

Once the tower JVs are established, the focus will be on how to drive revenues from the existing towers and on what additional sites will be needed for new spectrum. Only after that will there be a focus on what to do with redundant towers – which cost almost as much to decommission as to build.

Only DIF have the vehicle and appetite to be a consolidator and have the financial capability to decommission. The DIF has very little debt (0.18 Debt/NAV) but a high leverage ceiling (3.0 Debt/NAV) so it is only getting started.

Only DIF have the vehicle and appetite to be a consolidator and have the financial capability to decommission. The DIF has very little debt (0.18 Debt/NAV) but a high leverage ceiling (3.0 Debt/NAV) so it is only getting started

TowerXchange: The traditional market entry route in for an independent towerco would be to acquire a stake in an existing passive network – what about if somebody came with a pure BTS offering? They’d need a local partner, but would that be a credible play?

Dominic P Arena, Managing Director, AEC Advisory:

Probably not, as there are a number of good local players building towers in Thailand and they are well entrenched with low costs bases. They are not towercos so they don’t bring finance or co-location expertise, but they have strong hold on the market.

An affiliate of one of the Indonesian tower company investors tried a build to suit offering approach a couple of years ago, setting up a small local operation but had little success and ultimately pulled out. Were they too early? Not really, because AIS and DTAC were building their own 3G towers then, as was SOE TOT, but it’s just challenging against the local established players.

TowerXchange: The operators are having to pay twice for their existing passive network, CAT and TOT are capital constrained – who is going to finance the next generation rollout? Could someone come in with significant capital to build capacity? If the local players are purely builders, why couldn’t international towercos deploy capital to build a few thousand independent towers and lease them back to the operators?

Dominic P Arena, Managing Director, AEC Advisory:

There is nothing stopping them, but cash not a problem for a local player like AIS – they were still making 48% EBITDA margin after paying 25% of their top line revenues to TOT!

DTAC is somewhat more cash constrained, hence their interest in entering into tower sharing deals. You need to remember that they have over 90% of their towers under the concession regime and in dispute, so when CAT got an injunction to stop them putting 3G and 4G equipment on their disputed towers it somewhat focused them on JV negotiations. As we know, DTAC are pursuing tower sharing first and there may be a future need for new build towers. But ultimately there may be sufficient supply of existing towers to co-locate on.

The dark horse is DIF and they are not to be taken lightly by any foreign competitor. I already alluded to their funding capacity but to be specific, based on SEC regulations they can gear up to 3.0x Net Asset Value and at current valuations this means they still technically have borrowing capacity of US$6.2bn!

TowerXchange: What is the quality and connectivity of electricity grid and fibre?

Dominic P Arena, Managing Director, AEC Advisory:

All towers in Thailand now have fibre and there is a huge amount of backhaul fibre in Thailand. DIF alone has over 1.1 million core-km of fibre with their recent purchase of an additional 300,000 core-km from True.

Power is extremely expensive in Thailand and is about to get more expensive. Therefore renewable power solutions are definitely of interest

Since the 3G rollout, all new sites have been on fibre rings. There is very little microwave backhaul: during tropical storms there is too much fade with microwave, and latency is inadequate for 4G.

The electricity grid in Thailand is very good – blackouts are rare, although fairly regular flash brownouts do occur. For nearly all sites, basic battery backup is more than enough.

The problem does not lie with electricity provision but with cost. Power is extremely expensive in Thailand and is about to get more expensive. Therefore renewable power solutions are definitely of interest, such as solar, wind, hydrogen fuel cells et cetera.

Under the concession regime, there was no real rental market to establish lease rates and power pass through costs, however with DIF the tower rentals are net of utilities which are paid by the anchor tenant (True). If power assets do get wrapped into the JV towercos from concession assets, then we will see whether rental will include or pass through utilities costs. As we know that DIF operates a power pass through, the other towercos probably will be similar.