April 2015’s announcement of a landmark sale of 2,000 Egyptian towers to Eaton Towers for US$131.15mn may be MENA’s maiden tower transaction, but it will not be the last.

“This is a model that is just being introduced in MENA and Egypt so I believe that people will look at it carefully and if it’s successful I’d expect that it can be replicated,” said Kais Ben Hamida, the CFO who championed MobiNil’s tower sale. “In Egypt itself we have 19,000 towers so there’s certainly potential for replication here and also in other countries in the MENA region. So yes, I would expect that people will be looking at this transaction to see how it evolves.”

Expressions of interest have been solicited and received in two further parcels of MENA towers: 9,200 Mobily towers in the Kingdom of Saudi Arabia and further 5,000 Zain towers in the same market, together with around 1,600 Zain towers in Kuwait. TowerXchange also understands one of Algeria’s operators are appointing an advisor to explore the divestiture of ~6,000 towers. Together with the already announced Egypt transaction, we could see tower transactions in MENA’s three largest tower markets within the next year.

How will the MENA tower market differ from its obvious comps in SSA and Europe? How will potential tenancy ratios and valuations be affected by the fact that most countries, including the three largest markets, host only three nationwide MNOs? Much remains to be defined, including the regulatory regimes around infrastructure sharing in many markets, but what seems certain is that there is capital interested in MENA towers, and there is growing appetite for the region’s MNO’s to monetise passive infrastructure.

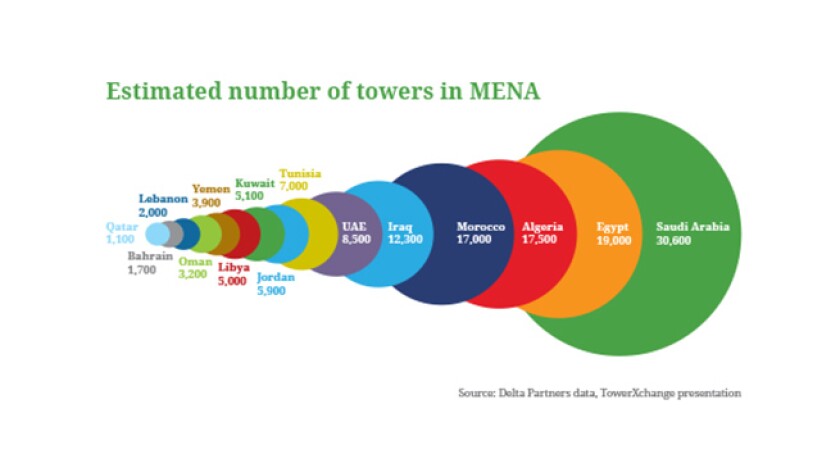

While the current penetration of towercos in MENA is just 1.4%, TowerXchange forecast that 17% of MENA’s 139,800 will be owned and operated by independent towercos by the end of 2016, rising above 25% by 2017.

Recommended reading:

Finding the balance: MobiNil’s CFO explains the rationale and strategy behind their tower sale

What we know about the Zain and Mobily tower sales in Saudi and Kuwait (2015)

Passive infrastructure potential in the Middle East

Is North Africa the new hotspot?

How the Egyptian tower market works

Stability and the road to a new infrastructure model: towers in modern Egypt