Senegal is a stable democracy targeting strong growth over the next few years. The country’s three operators all offer 3G services but 4G licensing controversy means there’s still significant growth to be found should independent towercos enter the market. As Orange’s Sonatel looks for partners to manage and build their tower portfolio in the country, TowerXchange explores the potential for growth and asks which towercos might be interested in this West African market.

Senegal: relatively low country risk, solid growth prospects

As one of the most stable countries in Africa, Senegal has operated a democratic process since 2000, with former prime minister Macky Sall’s Alliance for the Republic party winning over 65% of the vote in the most recent 2012 elections. Senegal has a population of around 13.5 million, of which a fairly high (by SSA standards) 50% live in urban areas.

Despite Senegal’s aspirations for strong economic growth, it struggled to grow its economy significantly between 2006 and 2012, achieving only 4.5% as opposed to the SSA average of 6%. This was been driven in part by poor harvests and low production rates from industry and mining. However services, technology and construction are underpinning the country’s growth and Senegal is targeting growth of 7% in 2015 by prioritising diversification and exports, representing a significant improvement.

Despite the Ebola outbreak in 2014 hitting many West African economies hard, Senegal’s speedy and decisive action against the outbreak resulted in the country only having one case of the disease and being declared Ebola-free in October 2014, meaning the country’s economy has fared significantly better against this potential setback than its west African peers.

The MNO landscape

Senegal is served by three operators; Sonatel (a 42.33% controlling stake in which is owned by Orange, with the government retaining 27.67%, the public owning 25% and employees owning 5%), Tigo (owned by Milicom) and Expresso (75% owned by Sudan’s Sudatel). Sonatel leads the market with a 56% market share versus Tigo’s 24% and Expresso’s 20% market share.

Sonatel (Société Nationale des Télécommunications du Senegal) was privatised in 2007 with France Telecom (now Orange) as strategic partner. The company currently has 8.1 million subscribers and operates GSM spectrum 900-2100 MHz, UMTS.

Tigo has been operating since 2006 and is the second largest operator in the country with 3.55 million subscribers. Tigo operates GSM spectrum 900 MHz, UMTS and HSPA+ mobile broadband.

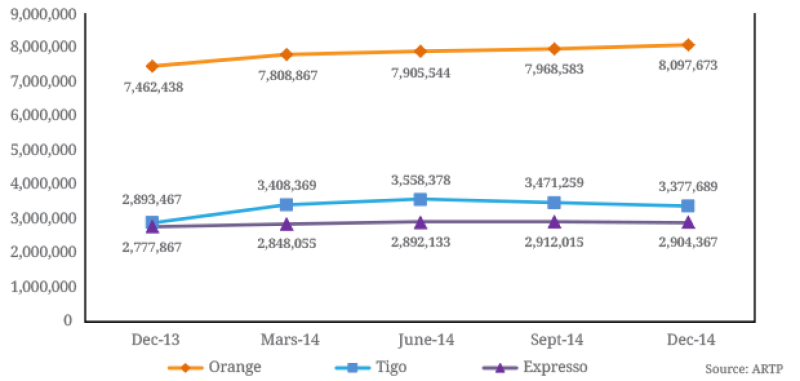

Due to poor fixed-line infrastructure in Senegal’s more rural areas, mobile penetration has grown quickly and reached around 111% in early 2015, with mobile broadband becoming the dominant platform accounting for 93% of internet access in the country

Expresso launched both fixed line and mobile operations in Senegal in 2009, initially choosing CDMA2000 technology to serve both market segments but switching to GSM technology using 900 and 1800 MHz spectrum in 2010, including offering 3G/HSPA mobile broadband.

Due to poor fixed-line infrastructure in Senegal’s more rural areas, mobile penetration has grown quickly and reached around 111% in early 2015, with mobile broadband becoming the dominant platform accounting for 93% of internet access in the country.

Quarterly evolution of telecoms subscribers by operator

Technology roll out

In terms of roll out, all three operators have been involved in LTE trials in Senegal over the last year, with Sonatel’s pilot the most extensive, lasting two years and live in over 40 regions after network upgrades costing US$240 million. However, in April this year it was announced that Senegal’s regulator, the Agency for Telecommunications and Postal Regulation (ARTP), had put a halt to these LTE trials after being disappointed by all three operators’ license tender submissions.

Previously the government had said it would base its decision on how best to commercialise 4G, and whether to grant licenses to existing operators or new entrants, on the implications for quality of service and the ability to deliver national coverage. However in this case ARTP found that the proposals received from the national operators were insufficient and failed to account for the government’s concerns about future investment. As such, LTE services will for now no longer be offered to the Senegalese population, although TowerXchange speculates that the forthcoming restructuring of the Sonatel passive infrastructure and the potential involvement of an independent towerco in the market will no doubt generate further pressure to answer the questions raised by the government, while the operators and the population will be keen for 4G services to resume as quickly as possible.

Towers in Senegal

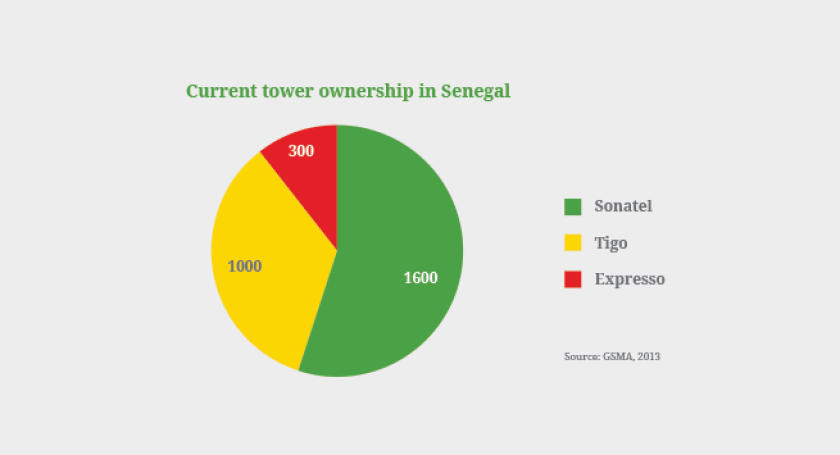

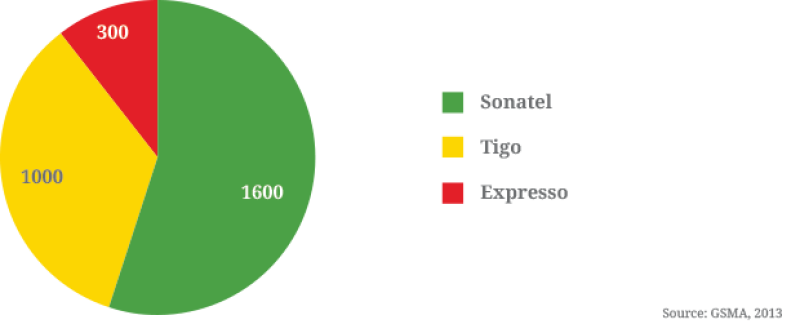

The most recent data we have on the Senegalese tower count comes from the GSMA in 2013, suggesting there were around 2,900 towers in Senegal, of which Sonatel owned 1,600 towers, Tigo around 1,000 and Expesso in the region of 300. TowerXchange believes Sonatel will outsource the construction and management of around 200 new towers to an independent towerco, giving them a market share of around 8%.

Despite Sonatel’s recent investment of US$240 million on network upgrades, the Senegalese government deemed the network not sufficient to support a full LTE roll out and that further investment was needed for infill capacity in large cities as well as rural roll out across the county.

Tower sharing in Senegal

To date there has been very little tower sharing in Senegal, either by way of independent towercos or bilateral swaps. Orange have been reviewing their infrastructure sharing strategy to the Sonatel assets by outsourcing 2,800-3,000 towers to a towerco across Senegal, Mali, Guinea Bissau and Guinea Conakry. TowerXchange’s sources suggest the process to seek a towerco or managed services partner in these four countries is underway with management of the towers being transferred between Q4 2015 and Q2 2016.

Our sources suggest that ownership of existing towers may not be transferred, with Sonatel preferring to engage separate managed services and build to suit partners

Orange has in the past preferred a ‘Manage with License to Lease’ (MLL) model as opposed to an outright sale of towers, as completed in Cameroon and Cote’D’Ivoire with IHS and in Kenya with Eaton, although that deal has since been terminated. Our sources suggest that ownership of existing towers may not be transferred, with Sonatel preferring to engage separate managed services and build to suit partners, and so TowerXchange watches with interest to see how this deal will be structured.

Current tower ownership in Senegal

Towerco interest in the market

At the current time it seems possible that three of the ‘Big Four’ towercos in Africa could have an interest in the Senegalese market. The Sonatel process in Senegal, Mali, Guinea Bissau and Guinea Conakry may be of interest to IHS as an extension of their West African footprint and relationship with Orange. Eaton’s history with Orange and appetite for market diversification could mean they have an interest in the market. Helios Towers Africa also have a presence in West Africa and a relationship with the second operator, Tigo, and may consider the opportunity as well.

One challenge the market will face is that over the last nine months, Africa’s leading towercos have driven to scale through the acquisition of 15,000 Airtel towers. They are therefore busy integrating new acquisitions and consolidating their businesses in preparation for the next major capital event. Africa’s towercos are therefore less acquisitive than they have been in the past and may be less interested to engage with Sonatel if the towers are offered on a less attractive MLL basis, as a straightforward sale and leaseback is preferred. If the towers were brought to market on a MLL basis, much would depend on the terms of the agreement at the conclusion of the initial 10-15 term.

The rise of the middle market towerco may offer further opportunity for divestment and tower sharing in Senegal, however. Growing companies such as Africa Mobile Networks and SWAP already operate in West Africa. AMN tends to focus on rural connectivity and opex sharing business models, while SWAP are gearing up to offer business models which may be more suited to acquiring smaller networks or offering build to suit services in the country.

Future implications for Senegalese towers

There is a strong chance that if the Sonatel towers were ever to come to market it could prompt Millicom to consider divesting their towers as well, as they did in 2010 in Ghana, DRC and Tanzania (in all three cases selling to Helios Towers Africa). Expresso may well also see the advantage in divesting their small network in order to free up capital to pursue their LTE ambitions. Certainly, if all three operators were to decide to divest there would be a level of ‘last mover disadvantage’ for the last to bring their towers to market given the high numbers of towers clustered around the main urban areas, giving any interested towercos a chance to secure the most desirable tenants in each area.