A culture of infrastructure sharing has existed in Malaysia since the turn of the millennium when the MCMC licensed over a dozen State-backed towercos, one stop agencies to permit and build towers in their respective States. Fast forward to 2014, after the consolidation of Malaysia’s MNOs from five the three, and Malaysia was host to the first carve out within Axiata’s edotco empire. edotco now operates 3,600 of Malaysia’s 22,000 towers, while the State-backed towercos operate a further 3,200. Drawing on insights gleaned from the Malaysia roundtable at the TowerXchange Meetup Asia 2015, let’s take a closer look at the unique structure of Malaysia’s tower and mobile market.

Malaysia’s mobile market

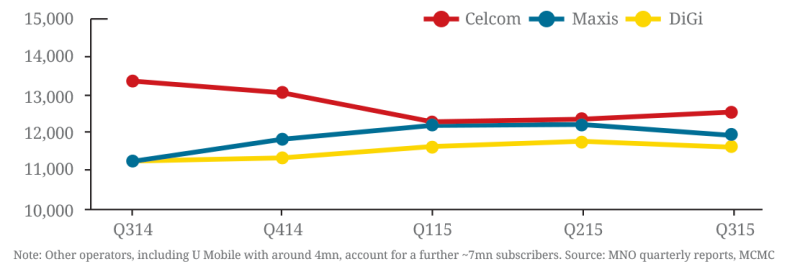

Malaysia is home to a mature, fiercely competitive mobile market led by listed entities Celcom, Maxis and DiGi each with between 11.5 and 12.5mn subscribers, with fourth operator U Mobile claiming around 4mn subscribers. Eight LTE operators have been newly licensed.

Figure one: Malaysia’s mature, competitive mobile market: subscriber numbers (in 000s)

Among a population of 30.49mn, mobile penetration declined to 144.8% in Q2 2015 from 145.8% a year earlier (Source: MCMC Pocket Book of Statistics), indicating the maturity of the mobile market. The battle among Malaysia’s operators is now concentrated on capturing 4G customers.

Malaysia’s tower market

There are around 22,000 towers now in Malaysia, representing almost exactly 2,000 mobile subscribers per tower.

Around 1,000 new towers were erected in Malaysia in 2015, where a new ground based tower (GBT) can cost in excess of RM300,000 (US$69,000). All of Celcom’s new build went through edotco, while Maxis and DiGi continued to build their own towers in 2015 – that may change in the latter’s case in 2016.

Much of Malaysia’s growth has come not from new GBTs but from ‘special structures’ like lamp posts, billboards, flagpoles, clock towers, minarets and water tanks which are easier to permit and harmonise with the skyline in dense urban areas where there is substantial demand for infill sites. The problem with permitting is particularly acute in Malaysia’s administrative capital Putrajaya, where it is reportedly almost impossible to permit a macro tower. In response to such challenges, edotco are soon to erect Asia’s first space-saving carbon fibre tower.

There are a substantial number of multi-tenant DAS solutions in Malaysia, including several hundred in edotco’s portfolio. edotco is also working on the first of several BTS hotels for the Malaysian market, wherein each site in a cluster would be equipped with a neutral antenna, with MNOs’ equipment hosted in a centralised equipment room.

An estimated 30-40% of Malaysia’s GBTs are in overlapping locations, but to date we’ve seen relatively little decommissioning.

DiGi and Maxis each have a similar sized tower network (an estimated 3,400 and 3,800 respectively), while Telekom Malaysia retained around 1,000 towers. There is substantial bi-lateral sharing of MNO-captive towers in Malaysia, although there are less tenants on the 5,000 towers owned by YTL, a Malaysian integrated infrastructure developer with investments in communications, utilities, construction, property, hospitality and IT. U Mobile owns a negligible number of towers, and has leveraged co-location to accelerate time to market.

Figure two: Estimated tower counts for Malaysia

Towercos own 31% of Malaysia’s towers, led by edotco’s 3,600 towers carved out of Celcom / Axiata. edotco aims to increase their Malaysian tower count by around 1,000 in 2016. A further 3,200 towers are owned by 14 different State-backed and other independent towercos. State backed towercos have a monopoly on new builds in four or five States as “One Stop Agencies” (they do the permitting as well as the building), but edotco has been able to negotiate rights to build in most other States.

Figure three: Estimated tower counts for Malaysia’s State-backed and other independent towercos

YTL acquired KJS, a state-backed towerco which then owned 309 towers, for US$15mn in 2014. Multiple parties have appetite to acquire further State backed towercos, although it may not be an easy process given political and personal vested interests.

Another potential stakeholder in Malaysian towers is OCK, a leading turnkey service provider operating across Asia with a strong presence in Malaysia, where they received a Network Facilities Provider license in 2011. In December 2014 OCK incorporated a wholly owned subsidiary in Singapore, OCK Telco Infra Pte. Ltd. to act as their platform in invest in the tower leasing business. OCK has since secured a contract to build 900 towers for Telenor Myanmar. While the company has unsuccessfully bid to build and operate some of the MCMC’s rural towers, OCK do not appear to have yet commenced operation as a towerco in Malaysia.

The Naza Group, a diversified engineering business, also has a registered Network Facilities Provider known as Premium Radius, which is Kedah state’s exclusive partner for telecom structures. Premium Radius claims to have an order book for 235 telestructures and an exclusive contract for microcell coverage with Kuala Lumpur City Hall.

Universal Service Provision fund deploying rural towers

As in many telecom markets, Malaysia’s MNOs are required to contribute 6% of their earnings toward a Universal Service Provision Fund. This fund has been active deploying RM3bn (US$700mn) to commission rural towers based on a RAN sharing business model. According to Malaysian publication The Star, 699 towers had been built by 2013 by the so-called Time 3 Phase 3 (T3E) project, while a tender for a further 400 towers was released in April 2014, with a further 1,000 being commissioned in 2015.

Progress of LTE and fibre rollouts

Around 3,000-4,000 LTE nodes have been deployed by each of Malaysia’s three leading MNOs, totalling around 13,000 LTE nodes to date. As usual, these are concentrated mostly in the major cities, but rollout is moving to secondary cities and is primarily using existing sites.

At the Malaysia roundtable at the TowerXchange Meetup Asia 2015, it was estimated than an additional 8,000 towers could be needed for 4G. However with local authorities reluctant to permit macro sites, most of that demand will be met by microcells, lamp-poles, DAS and IBS.

Malaysia’s eight newly licensed LTE operators are subject to license conditions requiring 10% coverage within the first year, and few have the time or capital to build their own towers. Some of their demand for points of service will be fulfilled by co-location, some by active infrastructure sharing.

Fibre availability is reasonably widespread in Malaysia and, although there are several fibrecos, it still sometimes feels like Telekom Malaysia has monopoly status. Their nearest competitor is City.

Power and RMS on Malaysian cell sites

There aren’t a lot of off grid sites in Malaysia, but edotco are looking at various off-grid power solutions including lithium-ion battery and solar hybrids.

Power is a pass through at almost all Malaysia’s cell sites.

RMS is not widely used by MNOs but is being considered by some State backed towercos. At time of press edotco’s Echo RMS solution was deployed on 2,800 of edotco’s 3,600 Malaysian sites.

Conclusion

The innovation and acquisitiveness of edotco makes Axiata’s carve-out towerco the most influential change agent in the mature Malaysian mobile and tower market. In 2016 and beyond, we expect the majority of new towers and special structures in the country to be built by edotco, which could also join YTL in a drive to rollup selected State-backed and independent towercos.