By Kieron Osmotherly, Founder & CEO, TowerXchange.

On October 23 2015, HTN Towers announced their intention to IPO 50-60% equity on the London Stock Exchange. On November 6 HTN Towers announced the IPO process would be discontinued due to “expressions of interest from potential buyers to acquire the company.” The following commentary is TowerXchange’s analysis of the HTN Towers business from a tower industry KPIs perspective – we are not financial analysts, and readers should make their own evaluation of the financial performance of the company.

The tale of HTN Towers is a twin narrative. One story is of Africa’s oldest growth organic tower build in the continent’s largest and most vibrant telecom and tower market – Nigeria. HTN Towers has built over 700 greenfield towers, many in prime locations, and over the last four years has added an impressive 0.25 tenants per annum to achieve one of the continent’s highest tenancy ratios of 2.2, backed by solid lease rates on long term contracts.

The other HTN story is a successful turnaround play. In the early days of the African tower business, tier one MNOs were reluctant to divest towers – thus the first tower transactions were agreed with second tier CDMA operators. HTN Towers, then Helios Towers Nigeria, and their new partners SWAP Technologies agreed partnerships with Multi-Links and Starcomms respectively. Alas, the CDMA operators hemorrhaged market share and margin to their GSM competitors in 2010-11. HTN lost 50% of their revenues in a very short space of time, refocused on GSM clients, and settled the outstanding Multi-Links debts by taking ownership of their 491 towers from exiting parent Telkom South Africa. The decline of the CDMA operators left both HTN and SWAP with a legacy of zero tenant “dormant” towers, towers they acquired for a price well below the premiums that were later paid in a Nigerian tower sale spree in 2014. The second HTN Towers story has a happy ending; 65% of HTN’s tenants and over 70% of their revenue now comes from tier one GSM operators, and 251 of those dormant towers now have tenants on them.

When the dust settled on the Nigerian tower sale spree of 2014, the country had transitioned from an operator-led tower market to one where independent towercos owned 79% of the county’s towers. Yet HTN Towers were financially outmuscled in those auctions by larger competitors IHS, Africa’s #1 towerco with over 23,700 towers, and American Tower, the largest towerco outside of China, which will have over 140,000 towers upon closing of announced acquisitions. With lots left to build but little left to buy in Nigeria, HTN may have to look beyond the borders of Nigeria for inorganic growth. HTN had been limited by an agreement with Helios Invest Partners’ other towerco, Helios Towers Africa, which restricted HTN to acquisitions in their domestic market (for the avoidance of doubt Helios Towers Africa remains a separate entity with a common shareholder in Helios Investment Partners – the two companies have in the past been close enough for one another’s CEO to serve on their respective boards of Directors, but that is no longer the case). The recent rebranding announcement of HTN Towers suggests that restricted remit might have been relaxed – there is a reason why the word “Nigeria” has been dropped from the company’s name!

The HTN towers narrative which was being promoted to prospective investors is primarily that organic growth success story. But prospective investors who dig deeper should be equally impressed at the successful turnaround of a business that started out as a cautionary tale of the hazards of towercos partnering with less than investment-grade tenants. HTN has since refocused to partner with some of Africa’s most investible opcos, they’ve created value by leasing up towers left dormant by their defunct original partner, and they’ve restructured their balance sheet with the first bond issuance by an African towerco.They may have finite acquisition opportunities in Nigeria, but TowerXchange are tracking several opportunities outside of Nigeria which might represent good acquisition targets for HTN Towers.

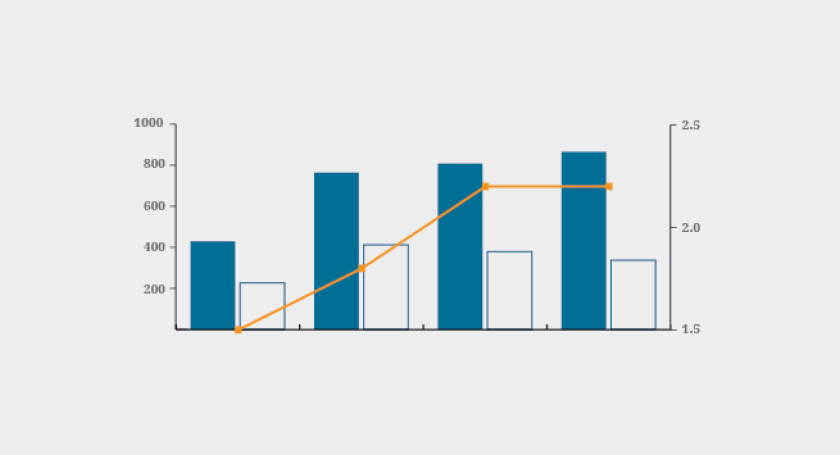

Solid performance in H1 2015

HTN Towers achieved US$73.3mn revenue and US$31.7mn EBITDA in the FY ending 31 December 2014, rising to US$36mn revenue and $19.8mn EBITDA for H1 2015, representing a growth in EBITDA margin from 43% to 55%. Their tower count rose slightly from 1,202 to 1,203, tenants were added to three more dormant towers, bringing their live tower count to 869, on which their tenancy ratio rose from 2.16 to 2.20. HTN also reports having a further 300 co-location orders “in hand” as at June 2015, which would effectively raise their live site tenancy ratio to 2.4. Technology co-location, where the same tenant hanging equipment for two technologies on the same tower counts as two tenancies, stood at 2.7.

History

2006: The history of the African telecom tower industry starts with the inauguration of HTN Towers, then Helios Towers Nigeria, in 2006.

2007: HTN passes the landmark of having built their first 100 towers.

2010: HTN secures a managed services deal to operate 400 towers for CDMA operator Multi-Links.

2011: Losing market share and with parent company Telkom South Africa seeking an exit, Multi-Links is acquired by HIP Oils, an affiliate of Helios Towers Nigeria.

2012: HTN takes control of 491 towers from Multi-Links en lieu of receivables.

2012: HTN builds their 500th tower. 2013: Capcom acquires Multi-Links from HIP Oils. Towers remain on HTN balance sheet.

2014: HTN completes a US$250mn high yield bond, the first bond issuance by an African towerco. The bond, which matures in July 2019, was three times oversubscribed.

2014: We believe HTN Towers unsuccessfully bid to acquire one or more of three large tower portfolios sold by Nigerian GSM operators. The portfolios would later be closed by IHS (acquiring a total of 8,850 towers from MTN and 2,691 from Etisalat) and American Tower (acquiring 4,700 towers from Airtel).

2015: HTN reaches agreement to manage and market SWAP Technologies’ 702 towers.

2015: Rebranded as HTN Towers with a pan-African remit.

2015: Announcement of intent to float 50-60% of the equity of the business on the LSE.

2015: Cancelled IPO citing receipt of expressions of interest from prospective buyers

What we know about the HTN Towers portfolio

At the end of Q2 2015, HTN Towers owned all 1,203 towers in their own portfolio, and had secured an agreement to manage and market a further 702 sites owned by SWAP Technologies. HTN Towers boasts one of the highest tenancy ratios in Africa at 2.2 tenants per live tower, having increased roughly 0.25 every year from 2010 to 2014. Any tenancy ratio growth above 0.2 per annum is generally considered very healthy. The live tower tenancy ratio on the SWAP towers is 1.4. HTN’s leases are typically five to ten years in duration with an average of 4.7 years remaining, representing future contracted revenue of US$336mn, excluding the effect of contracted lease rate increases.

Monthly TCF (tower cash flow) per live HTN site is just under US$4,500. Forex and fuel price exposure is limited by agreed increases in lease rates and, in some cases, US dollar pegged with power indexation. To date, Nigeria’s towercos have largely resisted downward pressure on lease rates being exerted by the country’s leading MNOs, but if the Naira continues to devalue against the US dollar, anticipate intense price negotiations when leases are up for renewal.

All of HTN’s own and managed sites are currently located in Nigeria, with around half the towers located in Nigeria’s ten biggest cities, but with a presence in 35/36 States.

HTN Towers have done a tremendous job re-calibrating their business away from their initial reliance on CDMA operators as anchor tenants. The decline and fall of initial client Multi-Links lead to the loss of more than 50% of HTN’s revenues at the time, and embroiled the company in lengthy legal proceedings culminating in the acquisition of Multi-Links by HTN affiliate HIP Oils. At the time, 2011, GSM operators generated just 31% of HTN’s revenue, but by FY14 76% of HTN’s adjusted revenues came from three credit worthy GSM operators: MTN, Airtel and Etisalat. A further 16 broadband and telecommunications customers are tenants on HTN towers, joined by broadcasting, transmission and corporate tenants.

Customer mix, H1 2015

Of 491 dormant tower sites, acquired as a function of HTN’s acquisition of Multi-Links’ towers en lieu of debts, 251 have since been activated. HTN reports that it costs an average of US$126,000 for a new BTS tower in Nigeria compared to US$30,000 to bring a dormant tower live.

Opex and power

Over half of HTN’s opex is related to power (52% in FY2014, 56% in H1 2015). While dual DGs are extensively used to ensure uptime, HTN Towers has deployed battery hybrids at 600 sites in their network to reduce energy opex and improve margins, with a further 100 sites to be upgraded in 2015. This represents 81% of the current HTN network, an impressive rollout considering just 9% (58) of HTN’s towers were hybridised as recently as 2011. HTN had suggested that US$80mn of the proceeds from their IPO would be used to fund new hybrid and solar equipped BTS sites, with a further US$13mn deployed to upgrade existing sites with hybrid and solar technology. HTN reports that battery hybridisation can reduce opex by ~US$350pcm, and called attention to a 12% decrease in opex in the last year attributable to hybridisation. The company is also piloting solar hybridisation, which could treble those savings to US$1,000pcm, having identified up to 650 existing sites suited to solar, with intent to deploy solar on new BTS sites also.

HTN Towers achieved an average of 99.97% uptime in 2014, compared to SLAs calling for 99.5%, with MTTR (mean time to repair) of 136 minutes compared to an SLA of 180 minutes. Having started deployment in 2012, 95% of HTN’s live sites are connected with RMS (remote monitoring systems).

The Nigerian mobile market

We’ve written about this many times before: Nigeria is one of the most profitable and investible frontier telecom and tower markets in the world, but it’s not for the feint hearted. Unreliable grid power and a rampant diesel mafia pose inescapable operational challenges, meaning operating Nigerian towers is a job best left to experienced practitioners like HTN Towers and their peers.

On the plus side, Nigeria is the largest economy in Africa, one of the fastest growing in the world, and has a rising urban population. A country with 150.6mn subscribers and a population of 140mn might sound like a reasonably mature emerging market, but Nigeria’s teledensity figure of 108% is distorted by widespread multi-SIMing. An urgent need to improve QoS suggests a long runway for growth both in network densification and coverage extensions – Nigeria may need to increase its current stock of 30,941 towers by 50% by 2020. Nigeria currently has 4,458 mobile subscribers per tower compared to 3,545 in South Africa and 1,417 in the UK.

MTN fine

The implications of the NCC imposing a US$5.2bn fine on MTN Nigeria, later reduced to US$3.9bn and the subject of legal challenge, remains unclear. Prior to the imposition of the fine, MTN had indicated a US$1bn capex budget to be deployed in Nigeria in 2016, with a healthy pipeline of build-to-suit search rings being issued and an equally healthy appetite for co-locations for both coverage and, in particular, capacity.

It seems likely that the threat of such a substantial fine will adversely affect MTN’s expenditure in Nigeria and, given that the operator is HTN Towers’ number one customer, the timing of the fine announcement, shortly after the IPO announcement, cannot have been ideal.

Nonetheless, TowerXchange remain bullish about the Nigerian mobile and tower market in the long term. MTN may have already paid a heavy price in executive jobs and a tumbling share price, but the company remains Africa’s most recognised brand and a blue chip client for HTN Towers and Nigeria’s other towercos. Nigeria needs a lot more towers, and as market leader MTN will remain at the vanguard of network investments, even if the challenges to the NCC fine and associated uncertainty cause a reduction in spend in the near term.

Competitive landscape

Independent towercos own 79% of Nigeria’s 30,941 towers. The combined HTN+SWAP portfolio is the third largest towerco in Nigeria: IHS’s deep partnership with MTN gives them an unassailable market lead with 16,541 towers (53% of the total stock), ATC Nigeria is integrating 4,700 (15%) towers recently acquired from Airtel, then you have HTN and SWAP with 1,905 (6%), followed by BCTek, which markets 700 towers on police compounds, Hotspot with around 250 towers and assorted small privately owned towercos representing around a further 200 towers.

Estimated tower ownership in Nigeria

Despite the fact that 10% of HTN’s towers are located within 100m of an IHS tower, 4% within 100m of an ATC tower, most telecom towers in Nigeria, indeed anywhere in the world, effectively operate as a monopoly. There is minimal competition on lease rates, which tend to settle at a ‘market rate’. Radio network planners seldom have choice between sites at overlapping locations, and the cost and time to market of building a new tower is usually so substantial that co-locating on an independent tower is preferable to building. This situation is accentuated in Nigeria by two important factors. One, layers of state and local taxation and bureaucracy make it even more time consuming and expensive to permit a new site – indeed such permits are unlikely to be granted if a co-locatable structure is in the near vicinity. And two, three of Nigeria’s four largest MNOs have divested all their towers, and with them has gone much of their internal competency and capacity to build towers. Almost all the new towers in Nigeria are being built by towercos, and co-location is always preferable to building a new site.

HTN’s challenge will be to secure a significant share of BTS (build to suit) towers in the face of competition from IHS and ATC Nigeria. While IHS has no formal right of first refusal on tower builds, their joint venture partnership with MTN and anchor tenant relationship with Etisalat suggests they will be in pole position to continue building most of Nigeria’s new towers (IHS has already built around seven times the number of BTS towers HTN has constructed in Nigeria). Meanwhile ATC Nigeria will be keen to compete for BTS opportunities to supplement their acquisition from Airtel. Increased competition for BTS opportunities may mean towercos are less able to ‘cherry pick’ locations where a second tenant can rapidly be added to a BTS tower.

The future

With HTN Towers’ rebrand came the suggestion that they would now have a pan-African growth plan, whereas previously their remit had been limited to their domestic market by agreement with Helios Towers Africa.

HTN Towers has a stated intent to build a further 1,000 towers by 2020 in Nigeria, a realistic goal given the 3-5,000 new towers currently being constructed each year, but a goal which they will have to fight to achieve in the face of considerable competition. HTN Towers can also generate significant growth simply by adding tenants to theirs and SWAP’s dormant towers. The company has also called attention to the opportunity to diversify into rooftops, oDAS, iDAS, billboards and even electricity transmission towers.

HTN Towers also has an M&A agenda, although remaining inorganic growth opportunities are limited in Nigeria where only Globacom and NATCOM’s towers remain on MNO balance sheets. Acquiring full ownership and control of SWAP’s 702 towers may be one option for HTN to consider. HTN Towers’ potential to pursue and close sale and leaseback opportunities elsewhere in Africa may be facilitated by Africa’s ‘Big Four’ towercos (American Tower, IHS, Eaton and Helios Towers Africa) being increasingly focused on the integration of an unprecedented spree of recently acquired towers.

Full disclosure; Inder Bajaj, CEO of HTN Towers has served as a member of TowerXchange informal ‘inner circle’ advisory board for the past two years and continues to be a member of that informal body. However, TowerXchange have no investment or stake in HTN Towers, nor does Inder nor HTN Towers hold any stake or formal position within or own any stake in TowerXchange.

The HTN management team

Pierre Danon newly appointed (October 2015) HTN Towers Director and Chairman Pierre Danon has an illustrious pedigree in telecommunications, having served as CEO of BT Retail (2000-5), in 2006 Danon helped Babcock and Brown Capital take over Eircom, becoming President from 2006-8. He served as President of the Numericable-Completel quad-play in France (2008-12), and is currently Chairman of Volia, a Ukrainian cable operator (2011-) and Vice Chairman of Danish market leader TDC.

Inder Bajaj has been CEO of HTN Towers since 2010, prior to which he managed the RCom’s 50,000+ towerco Reliance Infratel. Previously Inder spent ten years in senior management roles at RCom and Bharti Airtel, preceded by ten years as GM of Xerox India. In my dealings with Inder I’ve found him to be affable, passionate and highly knowledgeable about both the tower industry in general and the Nigerian tower market in particular.

Abhulime Ehiagwina serves as HTN Towers’ CFO, prior to which he held the same position at Etisalat Nigeria. Abhulime’s 21 years’ experience include senior Financial roles at Airtel and Total. Possibly the tallest man to take the stage at a TowerXchange Meetup (!), the soft spoken Abhulime is eloquent and insightful.

Chandrakent Modi, HTN Towers’ CTO, represented the company at the TowerXchange Meetup Americas where he also led a round table on Nigeria. Prior to his current role Chandrakant spent nine years with RCom in Mumbai, where was SVP Projects for passive infra sharing and sites delivery to tenant operators.