With the acquisition of MTC by edotco announced, Myanmar is now home to six tower companies, four of which are deeply engaged in the third phase of the rollout. New towers are going up by the dozen and the rollout remains broadly on track with GSMA forecasts suggesting 7,600 towers would be constructed by the end of 2015 and 17,300 by the end of 2017. The build rate may be impressive, but how are tenancy ratios progressing? TowerXchange’s Myanmar rollout FAQ summarises the latest market dynamics and baseline data.

Mobile market

1. Who are Myanmar’s operators?

State-backed incumbent operator, Myanmar Post and Telecommunications (MPT), now backed by KDDI-Sumitomo joint venture KGSM, remains the market leader, although their market share declined from 66.6% to 50.3% between Q4 2014 and Q2 2015.

International new licensees Ooredoo and Telenor launched services in August and September 2014 respectively, and both raced to a million subscribers within weeks. Telenor has more subscribers in total, Ooredoo has more 3G subscribers.

2. What is the latest on Myanmar’s prospective fourth operator?

At time of writing, Myanmar’s Ministry of Communications and Information Technology (MCIT) had postponed the allocation of the nation’s fourth mobile licence due to delays in selection from 17 local companies who applied to join a consortium with an international counterparty which would receive the coveted fourth license. Local ISP Yatanarpon Teleport (YTP), which was granted a limited private operator license in February 2015, remains a favorite.

Seeking to raise over US$1bn in international investment, YTP has been the subject of on-off partnership rumours, starting with Thailand’s True and Malaysia’s Axiata, while more recently Reuters reported a prospective US$800mn partnership with Vietnam’s Viettel. While the talks with Viettel have not been formally discontinued (insofar as they were ever formally started!), in May 2015 the Myanmar Times quoted YTP CEO U Shane Thu Aung as saying: “We are founding a new consortium under the direction of a management committee, which includes the deputy minister of the Ministry of Communications and Information Technology… The second stage will be forming a joint venture with a foreign partner.” Aung went on to suggest that it had not yet been determined whether the Myanmar government would hold a majority stake.

Myanmar mobile subscriber growth by MNO over the last year

3. Will the Myanmar military play a role in the telecoms rollout?

The precise role of MECTel, part of the military-owned Myanmar Economic Corporation which had been announced as a joint venture partner of MPT, remains unclear – they could become part of YTP’s consortium, they could yet emerge as a fifth operator.

Military participation in the Myanmar tower rollout has its advantages. For example, the assumption that many rural towers will need to be built with capacity for microwave backhaul may be incorrect as apparently there are thousands of military bunkers connected by fibre. In addition to possibly making this fibre available as a transmission network, the military continue to own a significant amount of land.

4. What spectrum has been allocated to Myanmar’s two new international MNOs, and have any LTE trials taken place?

According to Hardiman Telecommunications, Telenor and Oordedoo each received 2 X 5 MHz in the 900 MHz band, and 2 X 10 MHz in the 2100 MHz band. Both have suggested a future migration to LTE. Telenor acquired a further 5MHz of 2100 MHz spectrum in 2015 for US$75mn.” so it now reads “Both have suggested a future migration to LTE. Telenor acquired a further 5MHz of 2100 MHz spectrum in 2015 for US$75mn. MPT undertook trials of LTE using 20 MHz in the 1800 MHz band during the course of 2013. YTP currently operates WiMAX, and claims 40 MHz in the 2600 MHz band and has announced plans to migrate to LTE.

5. How have mobile subscriber numbers grown in Myanmar, and what mobile penetration does that represent?

There were 27.8mn mobile subscribers at the end of Q2 2015, representing 54% penetration. Subscriber numbers increased by almost 10mn since Q1 2015 when 18.1mn subscribers were reported, itself representing a 33% YOY increase from the 5.4mn subscribers reported a year earlier before the launch of Telenor and Ooredoo.

6. How many of those subscribers are on smartphones?

80% of Ooredoo subscribers are smartphone users, compared to around two thirds of Telenor’s. Bear in mind that mobile services and early adopters remain concentrated in Myanmar’s relatively affluent big cities, so that proportion is expected to fall as coverage is extended into rural areas with lower GDP per capital.

Estimated current state of the Myanmar rollout

7. What was each operator’s market share at the end of Q2 2015?

Telenor continues to add over 3mn subscribers every quarter, concluding Q2 2015 with 9.5mn subscribers, 55% of which were active data users. This represented 34.2% market share. Around 1.5mn of Telenor’s subscribers are 3G users whereas all 4.3mn Ooredoo subscribers are 3G. Ooredoo added 1mn subscribers, finishing Q2 2015 on 15.5% market share, down from 18.2% the previous quarter.

MPT had seen subscriber numbers fall (by 2.6mn) for the first time in Q1 2015, but recovered to climb to 14mn in Q2, retaining market leadership with 50.3%.

8. What levels of ARPU are being reported?

Telenor reported higher than anticipated ARPU of US$6.4 in Q1 2015, impacted by early adopters with high usage, slipping to $5.7 in Q2 as lower ARPU generators in rural Myanmar were connected. Ooredoo’s 3G-only network continues to generate slightly higher ARPU of US$6.5. In their Q1 2015 conference call, Ooredoo CFO Ajay Bahri suggested “what you are seeing right now is the ARPU from the high-income and high-GDP areas. As we move to more semi-urban areas, I think you will obviously see an impact of that as well. And within the urban areas, as we move to the next segment of the customers, I think that one should expect some sort of an ARPU decline.”

9. Any sign of price wars breaking out?

In October 2015 MPT dropped Internet charges from 7 to 6 kyat per MB , with voice calls coming in at 23 kyat per minute. In comparison Ooredoo offered a lower rate of 4.5-5.5 kyat per MB.

10. How much capex is being deployed by the new licensees?

Telenor continues to deploy capex more aggressively into Myanmar. Telenor’s total capex deployed in Myanmar to date is US$692.1mn, including US$106.9mn deployed in Q2 2015.

Ooredoo deployed US$416.3mn capex in Myanmar, including US$54.7mn deployed in Q2 2015.

Tower market

11. How many towers have been built to date?

Phases one and two of Telenor and Ooredoo’s rollout, which concentrated on Yangon, Mandalay, Naypyidaw and the transport links between these three largest cities, are now complete. Together with MPT / KGSM’s towers, TowerXchange estimate 7,410 towers have been built in Myanmar, although not all are on air.

Telenor added 718 new sites in Q1 and a further 536 sites in Q2 2015, bringing their total at the time to 2,308.

Ooredoo are less open about their tower count, which is believed to be approaching 2,000.

MPT has around 2,400 sites, with increasing use of co-location as well as continuing to build.

12. What does that translate to in terms of coverage?

MPT still has the widest coverage in Myanmar, but Telenor now connect to 113 townships which is roughly two-thirds of all townships in the country, while Ooredoo currently cover 35mn citizens, just under 70% population coverage.

13. What caused the phases one and two of the rollout to run approximately three months late?

Phases one and two of the rollout suffered operational delays for a variety of reasons, from the time taken to establish and train local construction resources, and the inability to complete certain tasks during the monsoon season, to bureaucratic delays, from importing equipment (at one point the rollout effectively ran out of steel!) and permitting sites, to the year-plus taken to grant licenses to Myanmar’s towercos. This has created knock-on financial delays, compounding the already challenging task of attracting investment into Myanmar’s towercos.

It remains to be seen whether Myanmar’s towercos can pick up the pace of rollout during phase three and enable Telenor and Ooredoo to meet the aggressive coverage obligations set out in their licenses.

14. What has been the progress to date of phase three of the rollout?

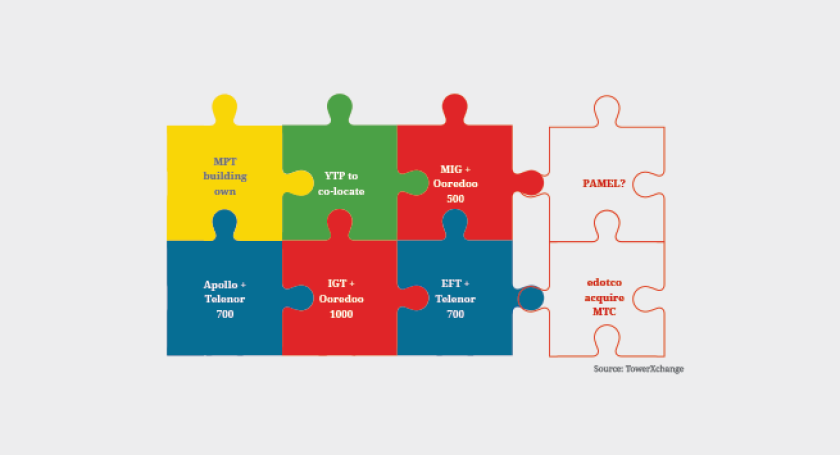

Phase three of the rollout is well under way with the four towercos involved, IGT, Apollo, EFT and MIG, building dozens of new towers per month. Priorities had to be shifted during the rainy season, when it became difficult to pour foundations in the Northern States, but site acquisition and equipment delivery continued, and build contractors focused on the drier Southern states.

“All that really distinguishes the first from the latest phase of the rollout is that there is a new Purchase Order (PO) for this next phase – in reality there is some overlap in terms of execution,” stated Apollo CEO Philippe Luxcey in a recent TowerXchange interview. “Our first phase build is all but complete, and we’ve already started building the 717 towers in the next phase.”

15. A-Z of Myanmar’s towercos: What did each towerco build in phase one and two, and what contracts have been secured in phase three?

Apollo Towers built around 1,100 towers for Telenor in phases one and two and have since secured a contract to build a further 700 towers for Telenor in phase three. Apollo Towers is Chaired by serial towerco entrepreneur Sanjiv Ahuja, who was the original Chairman of Eaton Towers in Africa and who is behind the new Staghorn Infrastructure venture in the US. Ahuja’s Tillman Global Holdings and Texas Pacific Group are the majority shareholders of Apollo Towers Myanmar, whose Managing Director is Philippe Luxcey. Apollo provides a ‘full service’ tower and power offering.

Digicel Myanmar Tower Company (MTC) built 1,250 towers for Ooredoo in phases one and two of the rollout. MTC’s portfolio featured some prime urban locations secured by Digicel’s site finders in advance of the company’s ultimately unsuccessful bid for an MNO license in Myanmar. Axiata-owned towerco edotco recently announced intent to acquire a majority stake in MTC from Digicel for US$221mn. edotco are believed to have beaten competition from PAMEL and American Tower to secure the assets. The acquisition remains subject to regulatory approval and the consent of minority shareholder Yoma Strategic Holdings, chaired and 37% owned by local tycoon Serge Pun. CEO Oliver Coughlan represented MTC at the most recent TowerXchange Meetup Asia. Digicel MTC provides a conventional ‘steel and grass’ offering – anchor tenant Ooredoo retains ownership of power assets.

Eco-Friendly Towers (EFT), a subsidiary of diversified Myanmar conglomerate Young Investment Group, is a new entrant towerco. EFT has secured an order for roughly 700 phase three towers from Telenor. EFT were initially the only towerco able to deploy and manage towers in several Northern Myanmar States, where security can be challenging, but TowerXchange sources have confirmed that EFT’s phase three contract is nationwide. Young Investment Group Chairman Thiha Aung represented EFT at the most recent TowerXchange Meetup Asia. EFT provides a ‘full service’ tower+power offering.

When we last checked in with Irrawaddy Green Towers (IGT), they had built 1,500 of 2,000 towers in phases one and two for Telenor, and have reportedly secured an order for a further 1,000 phase three towers, this time from Ooredoo. IGT was initially established as a partnership between Alcazar Capital Limited and Viom Quippo, whose former Group President Arun Kapur continues to serve as Executive Chairman and who, together with then CFO Karim Dakki, represented IGT at the most recent TowerXchange Meetup Asia. Today IGT’s sponsors still include Alcazar Capital, plus EPC Investors, M1 Group and Barons Telelink (a local Myanmar company). IGT provides a ‘full service’ tower+power offering.

Myanmar Infrastructure Group (MIG) is a joint venture between majority shareholder Singapore Myanmar Investco (SMI) and Golden Infrastructure Group (GIG), a venture involving Dan Ryan of Square1 Infrastructure. MIG had proved themselves building rooftops and poles in for both Telenor and Ooredoo in Yangon, as well as executing a substantial DAS project within Yangon’s airport, off the back of which they have secured a contract to build 503 towers in phase three of Ooredoo’s rollout. MIG has access to the capital markets via SMI’s Singapore stock exchange listing. MIG provides a full service tower+power proposition.

Pan Asia Majestic Eagle Limited (PAMEL, sometimes referred to as Pan Asia Towers or PAT) built 1,250 towers for Ooredoo in phases one and two. Along with Michael Gearon, PAMEL has management DNA in common with Indonesia’s Protelindo, but remains a distinct entity. In 2014 PAMEL secured US$85mn in financing from a consortium of five banks: DBS, ING, OCBC, Standard Chartered and Sumitomo Mitsui. PAMEL has not yet announced any participation in the third phase of the rollout, and was reportedly engaged in intense negotiations with Ooredoo on lease rates.

The final picture of phase three of the rollout may not yet be complete. TowerXchange sources suggest that Telenor may have a couple of hundred additional phase three sites to award, Ooredoo perhaps as many as 1,000 (which could be an opportunity for PAMEL or edotco).

Pieces coming together in phase three of Myanmar rollout

16. What is TowerXchange’s verdict on edotco’s acquisition of MTC?

edotco’s acquisition of a majority stake in MTC and their portfolio of 1,250 towers sets a benchmark price per tower of US$176,800 in Myanmar. While this is a considerably higher price than India, where towers changed hands for an average of US$114,301 between 2009 and 2015, lease rates in India are typically just US$600 whereas is Myanmar lease rates range from US$1,400 to US$1,700, driven by relatively high opex.

Another factor which justifies the price paid for MTC’s towers is that they were built in phase one of the rollout (which concentrated on Myanmar’s three biggest cities, Yangon, Mandalay and Naypyidaw), and built on highly desirable sites secured by Digicel in advance of their own ultimately unsuccessful bid for an operator license in Myanmar.

Whether US$176,800 remains a sustainable benchmark price for a Myanmar tower remains to be seen. But the premium paid by edotco to secure some of Myanmar’s most attractive towers, and to establish their maiden transaction beyond the Axiata footprint, seems justifiable to us.

17. Will phase three of the rollout draw towercos deeper into rural areas?

“Geographically the first round of towers was aimed at getting coverage up the central spine of Myanmar. Now it’s going to be much more spread out, mostly in rural areas, with fewer rooftop towers,” said Apollo Towers CEO Phillippe in a recent article in the Myanmar Times.

“It will become more difficult in terms of access roads as we begin to build in more remote places, and there’s still a lot of Myanmar to cover.”

18. Are Myanmar’s towercos finally licensed?

All four towercos (Apollo, IGT, MTC and PAMEL) who rolled out towers in phases one and two received “Network Facilities Service (Class)” or NFS(C) licenses on 3 February 2015, just over a year after Ooredoo and Telenor were granted their licenses.

MIG and EFT’s licenses have been applied for. Any delays to licensing MIG and EFT are unlikely to be problematic as a precedent has already been established by the MCIT to allow towercos to trade whilst license applications are progressed.

19. Is the regulatory regime around Myanmar’s towercos now complete?

“The Ministry of Communications and information Technologies has not yet issued all of the rules and regulations required to be issued under the Telecommunications Law, leading to continued regulatory uncertainty in key areas,” said Nicholas Towle of DFDL in a recent edition of NCRA’s “Myanmar: All That Matters.”

Mature tower markets are often characterised by regulation introducing a uniform approach to permitting, standardising processes across the various municipalities and authorities whose permission is required to build a site. However, in Myanmar permitting remains “a long process, and the government has so far not been able to arrange for a ‘blanket’ permit to override the need for individual permits in each case,” said DFDL’s Towle in the same publication. “Some tower companies have had to rely on letters of ‘no objection’ from village and town chiefs to give the go-ahead for construction and this is not a satisfactory legal basis for the future.”

Proving title within incomplete land registries, with many farmers having not yet applied for land use rights under the Farmland Act of 2012, complicates site acquisition for towercos. And even once they’ve secured a site, towerco’s exemption to the usual rule restricting foreign entities from leasing land for more than one year seems to not always be recognised by Myanmar’s Office of Registration.

20. What does a towerco’s “Network Facilities Service (Class)” or NFS(C) license cost in Myanmar?

The fees payable for an NFS(C) license in Myanmar are currently MMK 12.5mn per year (~US$12,000), plus 0.5% of relevant revenues and a MMK 2.5mn application / registration fee (~US$2,400).

21. What are prevailing lease rates in Myanmar?

Lease rates are seldom in the public domain, but TowerXchange research suggests that Telenor’s phase one and two lease rates were ~US$1,400pcm, with Ooredoo’s a little over US$1,700. The difference is explained for by the heavier, more power hungry but ultimately efficient equipment mounted on Ooredoo’s towers.

Such lease rates are relatively high by Asian standards, but equipment and construction costs are much lower elsewhere on the continent, particularly in India, where local towercos benefit both from economies of scale and from certain tax breaks as a result of being conferred infrastructure status. A better benchmark might be some of the more challenging SSA tower markets, in which case Myanmar’s lease rates appear on the low side.

22. What has been the progress of tower sharing in Myanmar?

Telenor and Ooredoo continue to appoint different towercos and, to date, have shared few of the towers built during phases one and two of the rollout.

Initially it looked like a more co-ordinated approach might be taken for phase three, known as “Project Optima”, in which Telenor would be the anchor tenant and Ooredoo would co-locate, but the strategy floundered, owing to difficulties agreeing a uniform lease rate given the different load requirements of Telenor and Ooredoo’s equipment.

Ajay Bahri, CFO of Ooredoo, said in their Q1 2015 conf call: “In terms of tower sharing… it has been a little more challenging to come to a conclusion than we initially anticipated, which is not unusual in a highly competitive environment as well where each one is trying to launch earlier than the other. But as in all markets when a little stability comes in, which is what we assume we should be reaching through, a more higher percentage of sharing would be evident then.”

Petter Furberg, CEO of Telenor Myanmar said in an email to the Myanmar Times: “Telenor is focused on building a long term sustainable cost structure which will allow us to offer the most affordable services to the mass market in Myanmar and at the most remote places in Myanmar; tower sharing is an important element to make this happen.”

Tenancy ratios remain much nearer one than two, but Myanmar’s towercos remain bullish about the prospects for improved lease up rates as networks fill up with capacity and cell splitting is required, and as MPT and, eventually, YPT expand through co-location. YPT seem to be planning extensive co-location, quoting CEO U Shane Thu Aung in the Myanmar Times: “we will come in very fast and use the existing infrastructure,” going on to suggest YPT had ongoing discussions with tower companies, but had not yet commissioned any sites.

When TowerXchange visited Yangon last year, it was apparent that few of incumbent operator MPT’s then 1,800 cell sites, consisting primarily of guyed-masts, had the structural capacity for multiple tenants, and sure enough MPT has since confirmed that less than 100 of their towers are suitable for co-location.

23. How investible are Myanmar’s towercos?

There has been plenty of capital interested in tower investments in Myanmar, but CFOs report it has been tough to close financing, particularly debt.

Myanmar has an under-developed domestic bank market, until now host to only a handful of small local banks, with no foreign banks allowed until an imminent change in the law. Even when debt can be sourced through foreign banks, typically in Singapore, securing authorisation to draw down the debt from the Central Bank of Myanmar can cause further delays. With so little credit available, with the local currency the Kyat not readily convertible, and with minimal US$ reserves in Myanmar, the mechanics of servicing a debt deal have proved extremely challenging in Myanmar.

The investibility of Myanmar’s tower companies is inextricably linked with two critical factors – lease rates and tenancy ratios. Lease rates remain under pressure, particularly from Ooredoo who are seeking parity with the pricing secured by Telenor despite using heavier equipment. Meanwhile, since Telenor and Oordeoo continue to rollout largely independently of one another, tower sharing and tenancy ratios are not being maximised. We expect both lease rates and tenancy ratios to ‘shake out’ in the long term, but in the short term, Myanmar’s MNO’s are outsourcing the financing of their rollout to towercos who are less credit worthy counterparts than themselves, then squeezing those counterparts as if they were suppliers not partners.

“It’s important to make sure no shortage of capital holds back development,” said IFC representative Vikram Kumar in the Myanmar Times in May 2015. “The World Bank Group is fully committed that nothing holds back telecoms,” he added. TowerXchange sources suggest an IFC investment into at least one of the Myanmar tower companies is imminent.

24. Can the towercos acquire the land under the towers in Myanmar?

No. All land belongs the government in Myanmar; citizens can only lease land. If foreign companies secure an investment permit they are allowed to enter into long term leases of up to fifty years, with two ten year term extensions.

25. Who is building the towers in Myanmar?

The towers being built for Telenor and Oordeoo will be owned by the towercos, but they are subcontracting the construction work to specialist managed service providers.

While most subcontractors employ substantial local workforces, it seems the lion’s share of the business to date has been won by proven international turnkey infrastructure firms such as Camusat, Leadcom, i engineering and GTL Infrastructure, while firms like GSM Telecom Partners are being drawn up the value chain from tower manufacture into project management.

26. How many towers are needed in Myanmar in the next four years? And how many will be on-grid, how many on unreliable grid connections and how many off grid

Despite delays, the Myanmar tower rollout remains broadly on track with the growth projections contained within the excellent GSMA Green Power for Mobile forecast published a year ago (download it here!), which suggested a total tower count of 17,300 by 2017, up from 7,600 in 2015 (a reminder: TowerXchange estimate the current tower count in Myanmar to be around 7,410, and it seems perfectly plausible that a further 190 towers might be lit by year end). Therefore we continue to use the GSMA model as the benchmark, in which it was forecast that there would be just under 10,000 prospective green power sites in Myanmar in 2017 requiring an investment of US$388.5mn but yielding US$137.4mn in annual opex savings for a 2.83 year RoI period, based on reducing diesel consumption by 83%.

Forecast tower site growth and grid connections in Myanmar

Power

27. Who owns the energy equipment at Myanmar’s cell sites?

A ‘Mexican standoff’ in tower power strategies took place in phases one and two of the rollout, as Telenor required their towercos to acquire and operate power systems, whilst Ooredoo retained ownership of their energy assets and did not include power in their SLAs. This made it very difficult for Telenor to co-locate on any Oordeoo phase one and two towers as they would have had to change their energy business model.

Thankfully, phase three of the rollout finally sees both Telenor and Ooredoo’s appointed towercos take on responsibility for acquiring and operating power systems. The dimensioning of a typical Telenor and a typical Ooredoo site remain fundamentally different however, primarily due to the large, power-hungry (but ultimately efficient) equipment Ooredoo is deploying.

28. What exactly is Ooredoo deploying that is so different from Telenor?

Ooredoo is using 4 way Rx diversity with a dual antenna configuration, an innovative approach that requires 30% less sites to generate the same coverage. This is a great approach from an holistic network planning perspective, but each site consumes ~20% more power than traditional solutions, so they are complex sites to dimension.

29. What will be done with those phase one and two power assets originally owned by Ooredoo?

Ooredoo appear increasingly inclined to outsource the management, or ultimately divest, the power systems they initially retains on their ~2,500 phase one and two sites.

Whilst various ESCO models and suppliers have been considered and rumoured, TowerXchange understands that at least a portion of Ooredoo’s Myanmar power assets have been outsourced to IPT PowerTech.

30. Why haven’t we seen the ESCO business model widely adopted in the Myanmar tower rollout?

One challenge is that ESCOs want to build distributed, micro-generation with telecom towers as anchor tenants. But ESCOs need permission to sell excess power to local communities and businesses, and to sell excess power back to the grid. That permission has not, to date, been forthcoming from Myanmar’s regulators.

Another challenge is identifying a kWh rate that Myanmar’s MNOs and towercos find digestible. In virgin territory like Myanmar, pricing is going to be a challenge. For example, few sites have yet been lit in the Northern States beyond the reach of the better roads, in an environment where unrest persists, so there is little data on the delivered cost of a litre of fuel to the country’s most difficult to operate sites. For an aspiring ESCO the risk is not just in the selection and installation of capitally intensive hybrid power systems, it’s also in the Service Level Agreements that MNOs and towercos use to assess quality and consistency, and in the application of penalties when performance targets are not met.

ESCOs’ capital requirement and risk exposure is multiplied when one considers the scale required to make an ESCO a credible business partner in Myanmar – is 100 sites enough? 500? 1,000? Indeed, do any ESCOs have the balance sheet to finance power at the ~5,000 or so sites each MNO or towerco might have in Myanmar by 2018?

31. Whose energy equipment is being deployed to Myanmar’s cell sites?

Every energy equipment vendor in the world seems to have a Myanmar case study on their website! However the companies most often mentioned in TowerXchange’s conversations with the Myanmar towercos have been Flexenclosure (who have done a lot of work with Apollo), Heliocentris (IGT), Pace Power, Eltek, Cummins and EnerSys.

32. What is Myanmar’s electricity generation capacity?

According to informed estimates in the NCRA Energy Sector Brief, Myanmar had 3,495 MW of installed capacity in 2013. Because 76% of Myanmar’s power is generated by hydroelectricity, firm capacity (the amount of energy that can be guaranteed to be available) peaks at 1,958 MW during the monsoon season, dropping to 1,554 MW in the dry summer season.

Electrification stood at 26% of the population, dropping to an average of just 13% in rural areas.

The cost per kWh was estimated at US$3.5-5 for household use, and US$10-15 for private industry.

Average precipitation in Myanmar (in)

“The national electricity grid currently covers the country’s central area from Mandalay to Yangon leaving other regions practically in the dark. Within the grid, only Nay Pyi Taw, Myanmar’s capital, gets a steady supply of electricity for 24 hours a day while people and businesses in most other cities including Yangon have to resort to the use of small generators which makes electricity very expensive.”

Source: the NCRA Energy Sector Brief, June 2014.

34. Is the climate in Myanmar conducive to solar and wind power?

Solar radiation is sufficient for solar power to be a viable option in all but the farthest Northern reaches of Myanmar, although wind resources are finite; seldom above the 5.5-6m/s generally held to make wind power a viable option.

35. How will power be provided at rooftop sites?

Rooftop sites represent a challenge for backup power – even if the landlord has a backup generator, is he allowed to sell power to the owners of a rooftop installation? With the structural capacity and permissions limiting the number of rooftop sites suitable for DG backed up power, fuel cells may be an option for many sites.

36. How do Myanmar’s operators figure the TCO compares between solar hybrid and CDC hybrids?

One Myanmar operator revealed that their TCO comparisons, inclusive of the cost of installation, suggested that at a low power 1.5kW site, the TCO crossover between solar hybrid and CDC hybrid was after two and a half years, pushed out over five years with a 2.5kW load and over six years with 4.5kW multi-tenant loads.

37. How important is vendor finance?

Given the multi-tenant, higher load environment likely to evolve in Myanmar, MNOs and towercos will find justifying the funding of renewables difficult, particularly with so many other demands on their finite capex. With debt and equity capital raising still a challenge, vendor finance is critical. For example, Flexenclosure’s access to European export credit agencies provides good interest rates for opex models, which has helped them secure their largest order to date from Myanmar.

One Myanmar operator summed it up succinctly: “we’ve got to ensure alignment between technical requirements and financial realities to ensure the best TCO solution is adopted – not simply cheapest capex solution. If we can’t get funding, we can’t do it.”

38. What are the opportunities for RMS and site intelligence solutions in Myanmar?

Data on grid availability and quality is practically non-existent in Myanmar, and is necessary to inform the selection and configuration of power solutions. RMS also provides important data on which to base the optimisation of fuel usage (and reduction of fuel theft, although few instances of theft have been reported in Myanmar to date); DG start/stop and runtime; battery charge, discharge and replacement; and the efficient use of any renewables. Integrating and aggregating data from different suppliers is key, based on which performance metrics can be generated for the comparison of sites and the evaluation of equipment and service providers.

Tarantula has announced that IGT is using their system, while iTower, by Infozech Software, is being deployed by another of Myanmar’s towercos. Nexsysone is used by both Ooredoo and MPT (KSGM) as the exclusive site management platform to build their networks.

Other pertinent facts about Myanmar

39. What is the population of Myanmar?

In 2014 Myanmar’s first census for 30 years revealed a population of 51,419,420, concentrated in the Yangon (14.3%), Irrawaddy (12%) and Mandalay Regions (12%). 29% of citizens of Myanmar live in urban areas.

40. What is the local currency and how has it been performing against the US$?

In the last year, the Myanmar Kyat, or MMK, has fallen a little over 10% against the US$ from a high of around K 960 to a low of around K1,100 to the US$ (at time of writing).

Forex risk remains the first challenge cited by most towercos and their subcontractors working in emerging markets, and Myanmar is no exception. Towercos and MNOs in Myanmar are spending US$ and earning Kyat, so are exposed to fluctuations in the valuation of the Kyat, and US$ are increasingly hard to come by.

41. When is Myanmar’s rainy season and what are average precipitation levels?

Monsoon season runs through June, July and August with shoulder months in May, September and October. During the rains, a lot of rural tracks become impassable, and it can be impossible to lay foundations in sodden ground.

42. What do companies need to know about importing telecoms equipment into Myanmar?

Quoting local law firm Polastri Wint & Partners in their 2014 TowerXchange interview: “Until recently, private telecommunications operators and contractors were not permitted in Myanmar. Only Government-owned enterprises had the right to import telecommunications equipment – the market has only just liberalised. With an investment permit issued by the Myanmar Investment Commission and an import permit, issued by the Ministry of Commerce, foreign towercos and their suppliers can import telecommunications equipment, with the recommendation of the Ministry of Communications and Information Technology, and where relevant, with the issuance of a telecommunications equipment license issued by the Posts and Telecommunications Department (which list of equipment will be formalised once the Telecommunications Rules have been enacted). Importers will be required to provide detailed information on the equipment proposed to be imported including the volume and specifications of such equipment, as part of the application for an investment permit.”

Recommended further reading

Third party research

MNO interviews

Towerco interviews

TowerXchange’s Interview with Ayad Chammas, new CEO of Irrawaddy Green Towers

TowerXchange’s interview with Oliver Coughlan, CEO, Digicel Myanmar Tower CompanyTowerXchange’s interview with Philippe Luxcey, CEO, Apollo Towers Myanmar

Legal and regulatory resources

Profiles of Myanmar’s tower builders

Camusat’s perspective from the front line of the Myanmar tower rollout

i engineering: surveying, building and strengthening towers for the era of infrastructure sharing

Leadcom’s experience building 83 sites (concurrently!) in Myanmar for Apollo

Power and site management system provider perspectives

Flexenclosure secures $multi-million deal to rollout eSite for Apollo Towers

Eltek on the challenges and opportunities of green solutions in Asia

EnerSys supplies over 600 sites in first entry phase of installation in Myanmar

Selected TowerXchange editorials on Myanmar

Commentary on the abandonment of the joint rollout in phase three

How to resolve the ‘Mexican standoff’ on tower power in Myanmar

Finally, latest Asian tower market data to contextualize Myanmar tower rollout