When the music stopped in the sale of Nigeria’s towers, HTN Towers and SWAP we’re left standing whilst IHS and American Tower sat on 69% of the country’s towers. It looks like a smart move to consolidate HTN and SWAP’s respective portfolios (Helios Towers Nigeria, now HTN Towers, has 1,203 towers, SWAP 702) within one sales and marketing operation, giving them a footprint in 34 of 36 Nigerian States and increasing their relevance in network planner’s thinking. The announcement that HTN Towers will manage and market SWAP’s sites may be a precursor to a full merger, before or after a potential IPO which HTN Towers is exploring.

Making history in the Nigerian tower business

Both HTN Towers and SWAP claim to be Nigeria’s, indeed Africa’s first towerco; SWAP as a function of completing a tower transaction with Starcomms in 2010, HTN Towers (then Helios Towers Nigeria) already had a BTS business in Nigeria at the time of their 2011 deal with Multilinks. As first movers, both portfolios contain some prime sites, and both have built robust, high quality structures capable of supporting multiple tenants. There is reportedly minimal overlap between the HTN Towers and SWAP portfolios – unsurprising given that they come from a similar vintage and with around half their towers from a BTS-driven origin that eschews building one tower too close to another. With 2,300 tenants on 1,200 towers, HTN Towers boasts one of the highest tenancy ratios in Africa at 1.9.

Shifting competitive dynamics among Nigeria’s towercos

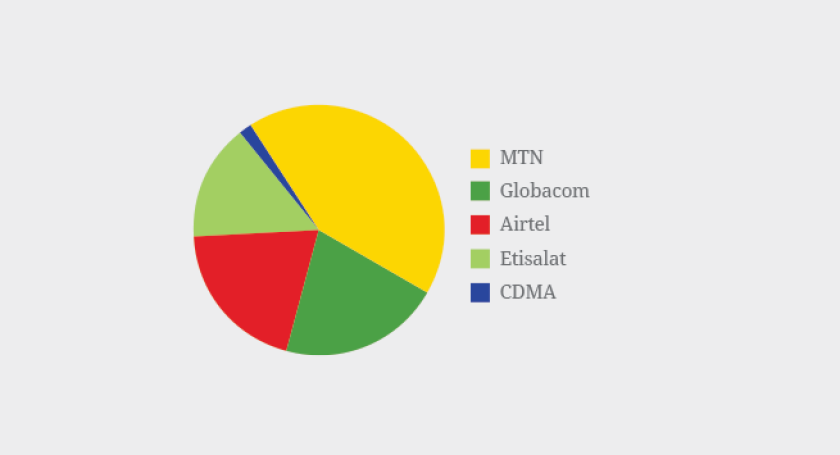

So, if their portfolios are good, why were both HTN and SWAP left in the cold as Nigeria’s towers came to market? First, there is sometimes a downside to being first movers as a tower market opens up. The first MNOs to sell might be those who most need the cash, as was the case with Nigeria’s CDMA operators who would ultimately struggle to achieve market share – currently Visafone and Multilinks’ 2.057mn subscribers represent less than 1.4% mobile market share. It took time to rebalance HTN and SWAP’s portfolios away from a bias toward these less credit worthy tenants, an exercise that has been largely completed –back in 2013 HTN Towers CEO Inder Bajaj told TowerXchange “When Telkom SA withdrew from the Nigerian market, its subsidiary Multi-Links (a CDMA operator) was one of HTN’s key customers. At HTN we decided to immediately re-focus our efforts on the core and stable GSM players like MTN, EMTS, Glo and Airtel… 95% of our business comes from Nigeria’s four tier one operators.”

Meanwhile, the two towercos who would lead the Nigerian market, IHS and American Tower, were building pan-African portfolios and credibility, particularly in partnership with the continent’s leading operator MTN, which then owned the most coveted towers in Nigeria. Whilst this was going on HTN Towers remained somewhat constrained by the geographical limitations imposed by Helios Investment Partners’ granting their other towerco, Helios Towers Africa, a pan-African remit, whilst HTN were restricted to Nigeria (a limitation from which they have since been freed – see sidebar). Thus when 16,241 MTN, Etisalat and Airtel Nigerian towers came to market in 2014, IHS had 10,500 towers in Africa, American Tower 4,851 and HTN Towers (then Helios Towers Nigeria) just 1,300. IHS and American Tower were able to leverage deeper relationships, established pan-African credibility, and strong balance sheets to secure the MNOs’ towers.

The machinations of tower auctions are seldom fully revealed in the public domain, but it is difficult to imagine anyone but IHS having both the capital and flexibility to acquire 8,850 towers from MTN Nigeria for US$882mn whilst allowing the MNO to retain a 51% equity stake. Helios Investment Partners’ towercos had assembled African assets relatively conservatively compared to some of their competitors in the land grab; avoiding deals that combined high valuations with high leaseback rates – leaseback rates that could come under downward pressure sooner – and agreeing that their MNO counterparts retain only minority stakes where requested.

Nigerian mobile subscriber market share

Meanwhile, Etisalat Nigeria attracted the highest cost per tower to date in an African sale and leaseback (US$277,060 per tower) despite not agreeing an exorbitant leaseback rate. Which is a long way of saying: it’s understandable that HTN Towers didn’t secure the MTN or Etisalat towers on the terms sought by the seller.

Whilst IHS was prevailing in negotiations with MTN and Etisalat, there was rumor that Airtel’s Nigerian towers might be divided into two portfolios, North and South, with the two acquiring towercos playing off against one another for service quality and the right to earn more BTS. HTN would have been a contender for one of those parcels, although the inequality of a potential North-South divide in terms of co-location potential may have scuppered the idea (Southern Nigerian is generally more prosperous than the North). Ultimately, American Tower subsequently acquired Airtel’s entire Nigerian portfolio for US$1.09bn.

It seems likely that, whilst the three Nigerian sale and leaseback processes were going on, American Tower looked at acquiring what is now HTN Towers, but ultimately passed on the opportunity. On the one hand their lack of operational footprint may have cost American Tower the chance of securing Etisalat’s towers: shortly after the deal then-CFO of Etisalat Nigeria Andrew Kemp told TowerXchange “Both IHS and American Tower’s offers were compelling propositions, but in the end IHS’s existing capabilities in Nigeria suggested they could provide a lower risk transition.” But on the other hand, with Gordon Porter and a strong management team already installed at ATC Nigeria, the notion has been validated that the U.S. towerco giant didn’t need to acquire HTN to have a credible Nigerian management team.

In the near term, if American Tower remains acquisitive in Nigeria there are smaller, less mature towercos than HTN Towers. These smaller towercos have less of the market’s growth potential realised and priced in – such acquisitions might look like lower hanging fruit than HTN Towers, with or without SWAP.

What does the future hold for HTN Towers + SWAP?

The potential merger of HTN Towers and SWAP has been discussed around their respective boardroom tables for years, and it should be re-emphasised that July’s announcement that HTN Towers would be managing and marketing SWAP’s towers does not yet constitute a merger. However, I like the prospective combination of HTN Towers and SWAP. In a Nigerian tower market where 79% of the towers are owned and marketed by towercos, amplifying the scale of HTN’s portfolio is a smart idea. Blending SWAP’s 702 Nigerian towers with HTN’s to create a portfolio of 1,905 towers gives HTN Towers+SWAP a 6% share of Nigeria’s 30,941 towers, and it gives them more stature in the eyes of prospective customers and prospective investors.

I wouldn’t want my commentary explaining why we think HTN Towers missed out on the acquisition opportunities in Nigeria to suggest I think it is less investible as a result – quite the contrary; HTN’s is a mature portfolio with many built-to-share towers generating good cash flow from a healthy tenancy ratio. It is undiluted by the integration of lower tenancy ratio operator towers, and unburdened by both the debt of substantial acquisitions and the subsequent investment of improvement capex. HTN Towers’ portfolio may be smaller than their competitors, but much of the work that has yet to be done integrating, improving and leasing up IHS and ATC Nigeria’s newly acquired Nigerian towers has already been done on HTN’s portfolio.

There are arguments for and against an HTN Towers IPO now, the foremost in favor being that towerco valuations are soaring worldwide, so there has never been greater investment enthusiasm for the asset class. On the other hand the devaluation of the NIRA is putting pressure on lease rates.

Whether HTN Towers comes to market alone or as a combined entity with SWAP, they have proved their operational capability and compatibility, which is a huge issue in the context of the huge power problem in Nigeria. If merged the two entities would doubtless save some SG&A and add a few million dollars to the bottom line quickly.

The HTN Towers story may not have played out as their pioneer founders may have envisaged – I don’t think being the #3 towerco in Nigeria was their objective – but I still think they may be rewarded with a healthy IPO if HTN Towers chooses to take that option, and I would not preclude a trade sale still being an option in the future.

HTN Towers+SWAP’s new pan-African remit

It was notable that when HTN Towers rebranded in July 2015 and dropped the world “Nigeria” from their company name, CEO Inder Bajaj emphasised their newly pan-African remit: “I am delighted to announce our rebranding to HTN Towers, which heralds a new phase in the company’s growth and reflects our pan-African expansion ambitions. We remain committed to providing best-in-class service to our customers in Nigeria and elsewhere as we continue to expand.”

Freed from their limited geographical remit, a combined HTN Towers+SWAP entity could be well placed to flex the traditional towerco acquisition model and create business models to address segments of the market which the ‘Big Four’ towercos are disinclined to address, given that they are integrating so many recent acquisitions. For example, HTN Towers could negotiate a deal with Sonatel, who are believed to seek a towerco partner in Senegal, Mali and the Guineas. TowerXchange sources suggest there has been finite appetite from Africa’s ‘Big Four’ towercos to engage in a Senegalese market where all three MNO’s (Sonatel, Millicom and Expresso) could have an appetite to partner with a towerco in a 3,000 tower market. It’s just this kind of opportunity that HTN Towers+SWAP might be well placed to address.

Nigerian tower market snapshot

Estimated tower count: 30,941

Towerco penetration: 79%

Current tower build rate: 3-4,000pa

Active towercos: IHS (53% market share)

ATC Nigeria (15%)

HTN+SWAP (6%)

BCTek (2%)

Hotspot and other small towercos (1%)

PaaS: Most towercos provide full power services

Source: TowerXchange, September 2015