With its large and well-developed mobile market and rising consumer demand for connected lifestyle services, France represents a good long-term opportunity for infrastructure investor-owners. However, the country’s mobile network operators - which directly control the majority of their passive infrastructure - are burdened by the high cost of developing next-generation services at a time of falling income from proprietary voice and messaging services. In pursuit of cost-efficiencies, operators should consider selling towers to specialised third-party providers in the short to medium term.

France is the third-largest market in Western Europe in terms of registered mobile subscriber numbers, with approximately 78.7mn accounts at the end of March 2015. 2G (900/1800MHz), 3G (900MHz, 2.1GHz) and 4G (800MHz, 1800MHz and 2.6GHz) networks are widely deployed across the country (‘metropolitan France’) and its overseas territories. 3G subscriptions predominate - there were 44.5mn 3G customers in March 2015 - but with lower bands having recently been opened to 4G services, the newer technology is making deep inroads into the market at a rapid pace. There were 13.2mn 4G subscriptions as of March 2015.

Operators’ strategies constrained by insular thinking

France’s four licensed mobile network operators have typically built their own passive infrastructures to support their respective networks. While this has involved constructing and operating their own towers, smaller antennae have been sited on buildings, cooling towers, electricity pylons and other high-rise installations to ensure quality signal coverage in both densely and sparsely-populated areas, as dictated by operational requirements.

Orange claims to have been operating 20,400 2G sites at the end of 2014, along with 18,500 and 6,900 sites that supported 3G and 4G services, respectively. The company does not say how many of these support multiple technologies, neither does it say how many of these sites are directly owned.

Numericable-SFR (the result of the 2014 merger of mobile operator SFR and cable broadband operator Numericable) claims to have had more than 18,500 radio sites at the end of the year, owning 5,200 pylons directly.

Bouygues Telecom - currently the third largest player in terms of subscriber numbers - claimed to be operating more than 15,000 sites across France at the end of 2014; it does not state how many of these are directly owned.

Mobile Subscription Market Shares, Q115

Free Mobile - part of the Iliad Group states that it operated 4,423 3G and 2,009 4G sites at the end of 2014, but does not provide any additional information, such as the number of sites that supported both technologies.

The French players adhere to the traditional mobile operator business models, including the belief that they need to be both an infrastructure owner/operator as well as a service provider. The high costs of building and maintaining networks, as well as acquiring the spectrum that binds these networks together are weighing on their operating margins; this investment will take many years to recoup as income from traditional voice, messaging and call termination/roaming services is being eroded by competitive and regulatory change.

There are few signs, as yet, that the French operators see any real need to divest core network assets that still have monetisable value and we believe they will remain resistant to the notion that selling towers to third parties will make their remaining business more sustainable in the long term. This insular thinking needs to change and, as evidenced by recent tower divestitures in ‘challenging’ neighbouring markets such as Italy and Spain, commercial needs can dictate a change in thinking.

Free stands out as being one of the most disruptive players in the mobile industry, having amassed a subscription market share of approximately 13.4% in under four years. It is close to overtaking Bouygues Telecom, if it has not already done so when eliminating dedicated mobile data connections serviced by the number three player. Free’s arrival prompted Orange, SFR and Bouygues to cut their prices, affecting profitability and ultimately sending SFR into a merger with Numericable and Bouygues to consider exiting the market.

The four players already share passive infrastructure in the mobile space and also collaborate to deploy fibre-to-the-home (FTTH) in markets where it would be prohibitively expensive to invest in next-generation access networks individually. Ultimately, the operators’ strengths are in content and services; to be able to justify continued investment in this area, they will inevitably turn to asset disposals. The old-guard players will be reluctant to concede defeat, however, and it will take more radical thinking from upstart Free to force the issue. Free has already offered to sell Bouygues’ towers in return for regulatory approval to acquire that company; its offer was rejected, but the notion of tower separation is at least on the table.

Who will buy?

There are few specialised independent telecoms towers companies openly at work in Europe, so we believe the likeliest buyers of these assets will be those companies already servicing the broadcasting and utilities sectors. In this regards, we believe the TDF Group is well placed to acquire French telecoms towers. With 9,500 sites across the country, it already serves the telecoms sector with backhauling facilities, access to datacentres and support for content distribution networks. The four mobile network operators already make extensive use of its facilities and its deep technical expertise gives it the resources needed to ensure continuity of service for the time-sensitive telecoms market.

TDF has also branched out into telematics, providing wireless connectivity for smart meters in homes and offices as well as supporting the development of intelligent highways, connected cars and smart toll road payment systems.

France - M2M SIMs Growth Trends (’000)

The growth of the telematics market is tracked by the French electronic services regulator, ARCEP, which notes that the number of machine-to-machine (M2M) SIMs totalled 8.736mn at the end of March 2015. This represented quarterly and annualised growth of 5.8% and 20.2%, respectively. We expect the number of dedicated M2M connections to grow at a faster pace over the coming decade as more and more ‘objects’ are connected to create the so-called Internet of Things (IoT).

With tens of millions of objects set to be connected to French networks over the next 10 years, so networks will be pressured to cope with increased traffic. We believe today’s mobile network operators are ill-equipped to deal with this rapid rise in (mostly data) traffic and that they need to focus on software-developed solutions that can effectively manage such loads. To do so effectively, they need to offload key infrastructure to specialised providers, particularly those with no direct stake in the content/traffic business to ensure impartiality in an age when expectations of network neutrality will become ever higher.

International players would be interested

Besides TDF, there are a number of European and international tower/infrastructure specialists that would be very interested in paying a premium for France’s telecoms towers. Abertis (now Cellnex) in neighbouring Spain has acquired a small batch of towers from local players Telefonica and Yoigo, while the Spanish units of Vodafone and Orange will almost certainly be considering tower disposals as they move to absorb the high costs of acquiring wireline broadband/pay-TV players. Cellnex has already moved to set up a dedicated telecoms towers unit and has mooted the possibility of overseas acquisitions to bolster a business that is already recording strong revenue growth (see ‘Abertis Plan Highlights Potential Of Europe’s Towers Market’, October 31 2014).

In Italy, Telecom Italia has spun its towers off into a standalone unit, Infrastrutture Wireless Italiane (INWIT), in which it sold a 40% stake through an initial public offering (IPO). The cash-strapped operator could well be persuaded to sell further stakes in the years ahead, which would be beneficial to the market in terms of transparency and neutrality.

INWIT will be competing for business with RaiWay (a unit of broadcaster RAI) and Mediaset-owned EI Towers, companies that could merge in the near future: EI Towers had bid EUR1.23bn to acquire RaiWay earlier in 2015, but the bid was blocked due to government opposition and concerns over market dominance. With INWIT now established and 3 Italia considering the purchase of Wind Telecom (a deal that may necessitate the sale of excess towers or the pooling of the enlarged entity’s entire towers portfolio), EI Towers may be able to convince regulators that its market dominance is now less of an issue. Reportedly, Mediaset plans to sell up to 40% of the merged business and to aggressively target the European telecoms, broadcasting and IoT markets.

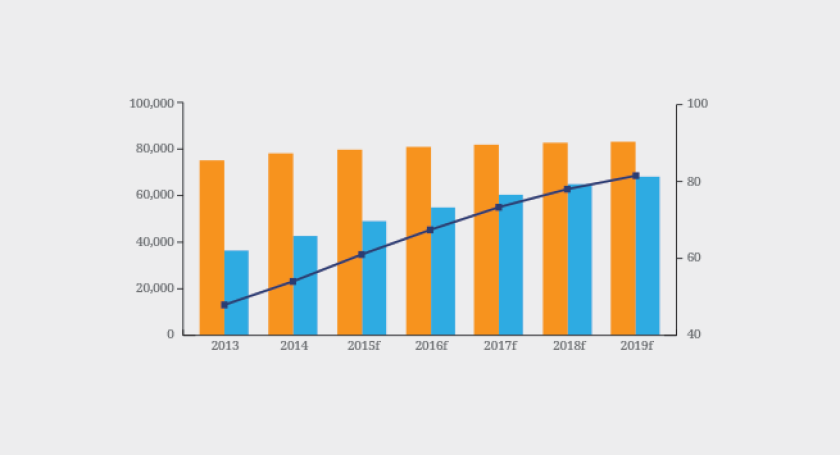

France Mobile Market Growth Outlook, 2013-2019

And what of global players?

Few towers companies have truly global footprints; most are content to expand regionally, as is the case in Latin America and Africa, where companies such as IHS Towers, Helios Towers and American Tower Corporation are seeking out investments that complement their regional footprints. In Asia, towers companies have generally kept to their local markets, so we do not expect companies such as Bharti Infratel, Reliance Infratel or Tower Bersama to move into Europe.

The only non-European towers company likely to take an interest in France, Italy or Spain might be American Tower. The company has a small unit in Germany, operating 2,000 towers. But its appetites seem limited to emerging African and Latin American markets at present, where the price per tower generally reflects the low population densities. Europe may, therefore, already be too expensive for players from outside the region.

France’s National Frequencies Agency (ANFR) claims there were - in theory - 54,107 2G-ready sites at the end of May 2015, of which it believed 52,003 were in service. In reality, it believes 39,251 were in service. Meanwhile, 53,355 sites theoretically supported 3G service, although just 38,017 were thought to be actually doing so. As for 4G, 21,371 sites were - theoretically - available and in service; in reality, it was closer to 17,493.

Even allowing for the fact that a large proportion of sites supported two or more technologies, this still means that the French towers market is one of the largest in Europe and supports one of the most data-intensive user bases. Tenancy space on French towers could therefore soon be at a premium and investors that are first to market should see considerable returns on investment over the long term.