Pakistan is another market to watch in Asia, with its combination of steady telecom market growth, considerable inventory of towers which are ripe for optimisation, and amenable regulatory regime. Nevertheless, this is still a challenging market with grid and security issues, and more than a little complexity in terms of operational realities. It’s been considered too risky by many investors to date, but that may be changing. In this editorial, TowerXchange takes a look at the mobile and tower market in Pakistan to share some insight into conditions on the ground, and identify the next big opportunities.

An introduction to the mobile market in Pakistan

With a population of over 185mn and a growth rate of 1.64% according to the UN, Pakistan is the world’s sixth largest country. The population of Pakistan is spread across its territory, and only 38% live within urban centres. Although the telecoms industry in Pakistan faces several challenges including transportation infrastructure and grid issues, unstable regions sometimes culminating in instances of tower sabotage, there is strong demand for connectivity in this country and the government is willing to support its development from a regulatory perspective.

As of Q4 2014 GSMA Intelligence put the number of mobile subscribers in Pakistan at 138.1mn, and SIM penetration at 74%. Geographic coverage of the country is over 90%. This is no small feat given the existence of the Federally Administrated Tribal Areas (FATAs) which require a high degree of local knowledge and connections to operate in.

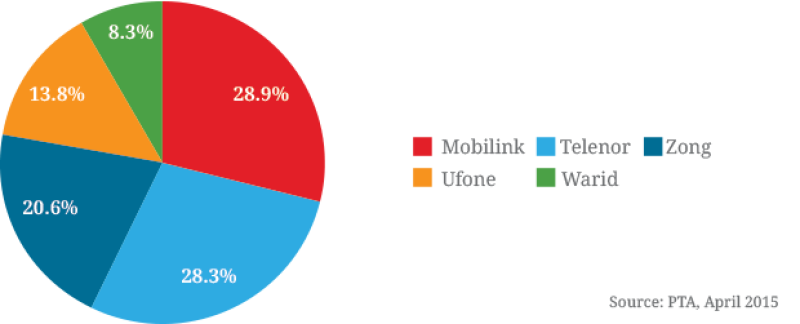

The MNO market has a healthy level of competition with five active service providers. Mobilink (VimpelCom) leads the market with 38.1mn subscribers, Telenor is a close second with 37.3mn subscribers, and Zong (China Mobile) is third with 27.2mn subscribers. Ufone is the fourth largest provider with 18.3mn subscribers, and Warid is a distant fifth with 10.9mn subscribers. It’s early days for mobile broadband penetration, with just over 13mn 3G and 4G subscribers in the country, representing 10% of the market, but with a young population (median age 23.2) this is expected to grow quickly.

3G was first launched in Pakistan in Q4 2014 and coverage now exceeds 50-60% in top population density markets; service launches in new cities are continually coming to market. Zong (China Mobile) and Wateen (Abu Dhabi Group) have also launched 4G LTE services and their coverage is expanding rapidly. The CIA Factbook estimated Pakistan’s GDP per capita (PPP) at US$ 4,700 in 2014 and listed the GDP growth rate in 2014 at 4.1% which will help support this development. At the same time international investments, particularly from China, are increasing as the high level of demand is starting to offset the risks associated with this market.

Pakistan is host to the usual cluster of non-traditional MNO prospective tower tenants, one of the most important of which is Wi-Fi broadband service provider BurQ, which is targeting 2,500 tenancies in the next four years – read about BurQ in an interview later in this special feature.

Total teledensity in Pakistan

Pakistan’s tower market

At this point there are only two companies with any substantial activity on the ground in Pakistan: edotco and Towershare, and the vast majority of the estimated 28,000 towers in the country are still operator captive. edotco is soon to receive approval to begin construction of its first 200 build to suit sites, and plans to leverage its 13,000km fibre network to deliver 3G and 4G. Towershare has a small footprint and is helping its MNO clients to optimise their existing infrastructure, often in challenging areas of the country. The acquisition of over 4,500 of Warid’s towers by Towershare has been announced but not yet closed. TowerXchange has confirmed that two more of Pakistan’s five MNOs have an appetite to monetise their towers. According to the PTA there are six other local companies with licenses to provide infrastructure, at least one of which has been acquired by Towershare, but to date the others haven’t made any significant rollouts or participated in any major deals.

At this point the field seems to be wide open for more tower transactions and infrastructure sharing as demand for connectivity is surging and the average tenancy ratio is still relatively low at an estimated 1.3 with only 30% of the towers on the ground being shared. In addition to this the towers that have been rolled out to date have not always been planned with overall efficiency in mind and there are several areas with significant overlap, as mentioned in our interview with Towershare this month. Finally, ARPU is very low at US$2 meaning that MNOs in this market are under strong pressure to optimise networks and ensure profitability.

Tower licensees in Pakistan

Progressive regulation, but local inconsistencies

The regulator in Pakistan is very proactive in supporting the development of telecoms in Pakistan and is perceived to be one of the region’s most progressive; the PTA was just re-elected for a third four year term as a member of the ITU council. There are, however, still unique operational challenges and regulatory issues in Pakistan.

Like many other markets different states and municipalities have their own regulations on telecoms infrastructure and rights of way. The layers of bureaucracy added by different regional governments also means that the tax regime in Pakistan is costly and complex. Changing policies can lead to the economics of infrastructure deals being unpredictable in the long term. It requires a good deal of familiarity with this market to negotiate permits. Infrastructure maintenance is also challenging on the ground and requires personnel with experience dealing with the different local governments.

Pakistan mobile subscriber market share

Unstable grid

The instability of the power grid is another obstacle to be overcome in Pakistan. This is a market that still experiences regular outages, typically around eight hours per day and potentially longer in the Summer months when the grid is further strained.

There has been active investment in the grid and there are several coal and hydro plants set to come online over the next couple of years. However, it remains to be seen if this will be enough when as many as 1,000 to 2,000 new towers are expected to be rolled out per year to support demand for capacity. As in other markets in the region, autonomy and efficiency are the watchwords and both edotco and Towershare are poised to integrate battery hybrids and renewables.

What to expect next in Pakistan

With a market that is seemingly so ripe for the towerco model and infrastructure sharing, the industry is eager to know where the next major tower deal will come from. There is ongoing speculation that the number one and number two MNOs in this market, Mobilink, owned by VimpelCom, and Telenor are actively seeking to divest their tower assets. Exact numbers aren’t known at this point, but based on market share these portfolios are somewhere in the region of 5,000 to 7,000 each, and it would have a huge impact on Pakistan’s fledgling tower industry if these came to market at the same time. There could be several potential buyers for these portfolios including Pakistan’s two most active towercos, Towershare and edotco, while Indian or even Indonesian towercos with an interest in expansion into a new market, with sufficient capital to invest, and with an appetite for a relatively high risk, high reward tower market may also participate in a Pakistani tower auction.