Mobile market overview

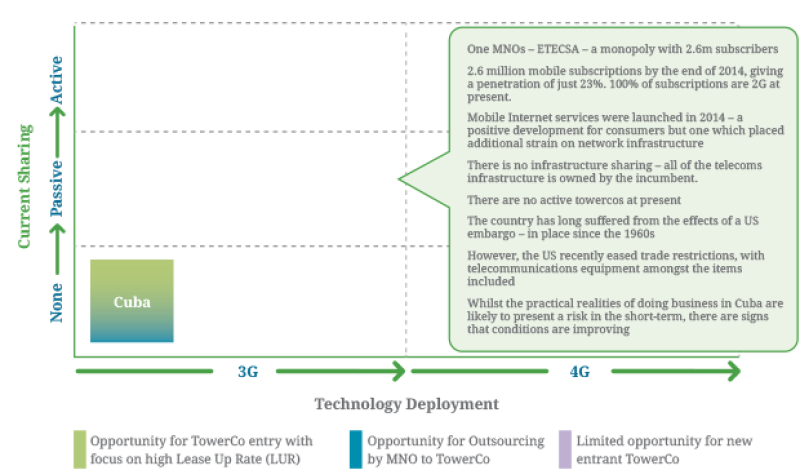

Cuba had a population of 11.3mn people and 2.6mn mobile subscriptions at the end of 20141, giving a mobile penetration of 23% – a very low level of penetration compared to other markets in the Americas and worldwide. Even a relatively undeveloped market like Haiti has penetration of 75%. 96% of mobile subscribers in Cuba had a pre-paid account. The low historic penetration stems from factors such as the lack of competition and the high cost of mobile ownership compared to income levels. There is a single Mobile Network Operator (MNO) serving the Cuban market – ETECSA (Empresa de Telecomunicaciones de Cuba S.A.) with 2.6m subscribers. According to Telegeography, ETECSA is wholly owned by the Cuban government via six state entities: Telefonica Antillana (51%), Rafin (27%), Banco Financiero Internacional (6.2%), Universal Trade & Management Corporation (11.1%), Banco Internacional de Comercio (0.9%) and Negocios en Telecomunicaciones (3.8%). Local financial services entity Rafin bought its 27% stake in January 2011 from Telecom Italia for US$706mn.

Key mobile market developments

Whilst Cuba has a very low level of mobile penetration, the market has been showing significant growth – with 260,000 new mobile subscribers added in Q4 2014, and annual growth of 28% across the year. 3G services have yet to be launched – 100% of subscriptions are 2G at present. ETECSA expects to activate another 800,000 subscriptions over the course of 2015 – driving penetration to around 30% – and indeed it has stated an aim to sign up 800,000 new customers in each year up to 2018.

Recent subscriber growth has been driven in part by the launch in March 2014 of mobile email and internet access, plus the increase made in the recharge validity period allowed for pre-paid customers – which was put up to 330 days. Growth is expected to continue as further new services are introduced – for example a balance transfer service is due to be launched this year – and as a result of several agreements struck with international players, a reflection of the fact that the market is starting to open up as Cuba gradually becomes less politically insular. For example, in July 2014 an agreement was signed between ETECSA and Orange. Under this accord Orange Horizons plans to offer its services and products to the Cuban monopoly operator, as well as sharing its expertise and setting up a technology training centre in Cuba.

Most notably, as a result of recent thawing of relations between the US and Cuba, there have been a number of moves by US companies to initiate activities relating to the market. For example, Florida-based SMS Cuba recently announced the launch of text messaging services between the two countries, enabling users to communicate directly with contacts on the island via a two-way messaging service. Previously, no text message service was available between the two countries from any US-based wireless carrier. In a similar move in March 2015 New Jersey-based IDT Telecom began handling direct international long-distance (ILD) traffic between the U.S. and Cuba, after signing an agreement with ETECSA, and Boost Mobile, a unit of Sprint, also recently launched a pre-paid plan tailored for customers making calls and sending texts to Cuba.

Coverage expansion

In order to cater for the growth which has occurred, ETECSA has steadily increased the number of base stations across the island from 350 in 2010 to just over 600, and plans to continue to invest in expanding coverage and improving service quality. In 2014 it added around 80 new cell sites, and carried out traffic management work in Havana and other areas due to an increase in traffic caused by the introduction of new services. In May 2015 Reuters quoted the Cuban finance minister Lina Pedraza as saying that the country is in advanced negotiations with Huawei to do more business on the island.

It should be noted in the context of infrastructure expansion that past experience would indicate that significant extra capacity is indeed required. According to the New York Times, when the mobile phone email service was launched in 2014 there was a very high level of take-up – with 100,000 people subscribing to the service, despite it costing 50 times the amount of many U.S. data plans – leading to the network being flooded and to the failure not only of the service itself but also regular voice and text mobile services.

Regulation

The last three years have seen significant developments in the approach to the telecoms market within Cuba, which have helped to stimulate its growth and development. In 2013 Cuba’s Ministry of Information and Communications (MIC) was renamed and restructured – to become the Ministry of Communications. At this point it became solely responsible for state regulatory functions, while business operations were taken over by two senior management organisations served by the ministry – the Correos de Cuba Business Group and the Computing and Communications Business Group. According to the Official Gazette, the move aimed at allowing for a more precise definition of the ministry’s mission and functions, as well as a more rational structure, composition and size.

Also in 2013 ETECSA reduced the cost of making a national mobile phone call to CUC0.35 (US$0.35) per minute from CUC0.45. ETECSA also introduced a calling-party-pays (CPP) system, meaning that mobile subscribers no longer had to pay to receive calls and text messages. In November of the same year ETECSA announced that the government had approved ‘Telecommunications Agent’ as a new category for self-employment, enabling individuals to market the company’s products and services.

Agents are therefore permitted to sell pre-paid recharge cards for fixed and mobile telephony and internet services, as well as collect payments for bills and offer local, national and international phone calls from their home. The agents are obliged to charge the same rates as ETECSA, with the company paying them a commission.

In 2014 ETECSA launched a promotion offering mobile customers a reduced rate for calls and SMS to international networks – with different promotional tariffs for communication by these means to ‘America (except Venezuela)’, Venezuela, and the rest of the world. In the same year the Ministry of Communications capped the rate which ETECSA can charge for mobile internet access at CUC1 (US$1) per megabyte of data (excluding service set-up charges) – in anticipation of the launch of mobile internet access. A change to regulations in 2015 has seen Cubans able to own up to three pre-paid mobile lines from ETECSA.

As stated above, 2015 has also seen the first signs of the benefits of improved relations between the U.S. and Cuba – with efforts to increase Cubans’ access to telecoms services seen as part of move to enable better communications between the citizens of the two countries. As part of this move in December 2014 the White House commented that it would authorise ‘the commercial export of certain items that will contribute to the ability of the Cuban people to communicate with people in the United States and the rest of the world’ – to include the commercial sale of consumer communications devices, related software, applications, hardware and services, and items for the establishment and update of communications-related systems. Whilst the U.S. trade embargo in place since the 1960s has not been lifted – and the Act which enshrines it is unlikely to be repealed given Republican control of the U.S. Senate and Congress – the easing of restrictions is likely to have a positive effect on the development of the mobile arena in Cuba. Indeed, in March 2015, a delegation of U.S. telecoms officials conducted a three-day visit to Cuba – during which talks were held with Cuban officials on this very subject.

The tower sharing market

The tower sharing market is currently non-existent in Cuba – given that there is monopoly with regard to the operation of mobile telecoms, with all of the infrastructure in place owned by the incumbent. However, the recent political moves to foster improved relations between the U.S. and Cuba – including the degree of specific focus on opening up the telecoms market to U.S. providers – are a sign that the involvement of foreign infrastructure providers, including potentially towercos, may become feasible in the next few years.

Having said that, there are significant practical barriers to be overcome by any company thinking of investing in Cuba – from the availability of land on which to locate towers and permissions required to use it, to shortages of diesel and all manner of equipment. Bureaucracy, rules on foreign investment and a shortage of skilled labour also stand to make market entry difficult in the short term. Whilst the signs for the future are positive, the reality of doing business in Cuba remains hard

[1] GSMA

Guest columnist Ed Siegle

Ed Siegle is a Principal Consultant in Mott MacDonald’s Technology & Communications Division. He has 20 years of experience as a consultant, primarily focused on the telecommunications industry, working for operators, vendors, investors, regulators and public sector organisations. His particular expertise lies in market analysis, commercial due diligence, product and market strategy development, demand forecasting and business case production.

In the course of his career he has worked for clients in the UK, Europe, the U.S., Africa and Latin America. He has spent over two years living and working in Latin America, including 18 months in Brazil where he helped establish new offices for two consultancies. Over the past three years he has been part of a Mott MacDonald team commissioned to execute a series of advisory projects for towercos looking to invest in developing markets.