During the second TowerXchange Meetup Americas, experts involved in the Colombian market gathered to discuss key trends, challenges and opportunities faced by the local telecom tower industry. With permitting and community acceptance of the towerco model high up on the list of top issues, Colombia is still a very profitable market for the telecom tower industry as a whole and one that has been able to attract as many as twelve towercos to serve the national territory.

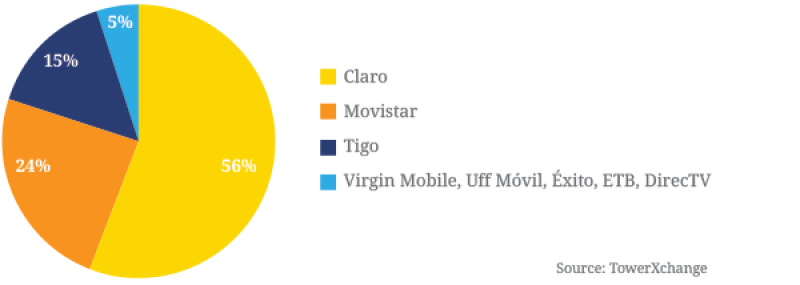

Colombia is the third most populous country in the region, after Brazil and Mexico, with an estimated 48mn people. The country is host to three strong carriers with Claro enjoying a dominant position despite shrinking market share since 2012. Claro holds 56% of the market (compared to 62% back in 2012), followed by Movistar with around 24% and Millicom’s Tigo with approximately 15% market share.

While Claro’s position has been slowly weakening, other players have entered the market, while Tigo merged with fixed line operator Une-EPM back in 2014. Additionally, a number of MVNOs players such as Virgin Mobile, Uff Móvil, Éxito and ETB are building subscriber bases while Satellite TV provider, DirecTV, started a 4G LTE service in July 2014. Colombia’s incumbent operators are already deploying 4G on the AWS band, but it’s very early days for the rollout. Tigo, Movistar and ETB have infrastructure sharing and roaming agreements in place to accelerate their 4G rollout.

Mobile market share

Thanks to this dynamic carriers’ landscape, Colombia has attracted as many as twelve towercos, six of which are local and the rest international. The size and potential of the Colombian tower market attracted American Tower to enter the country, while other active towercos include Continental, Innovattel, Centennial and NMS. Torres Unidas, Phoenix Tower International and Torres Andinas were all in the early stages of opening up operations in Colombia at time of writing. Another of the region’s largest towercos is reportedly considering an entrance in the country which would create even more competition.

While there is clearly great enthusiasm for the Colombian tower market, TowerXchange don’t see the obvious pathways to substantial sale and leaseback opportunities as Entel would appear to provide in Chile and Peru. Claro still sees the network as a competitive differentiator and even if, years into the future, they did decide to monetise their Colombian towers, their own towerco Telesites might be the most likely vehicle to bring those towers to market. Of Colombia’s other operators, Tigo has already sold most of their towers (to American Tower back in 2011), while Movistar started monetising their Colombian towers in 2010 but discontinued the process in 2012.

Country risk is low compared to neighbouring Venezuela

On the political front, the country’s perceived risk is definitely lower than that of neighbouring Venezuela and the potential threat of asset nationalisation isn’t seen as realistic. However, the local currency - the Colombian Peso - has been fluctuating over the past year and it’s not uncommon for towercos to try to stipulate contracts in US$.

In terms of regulation, the government has been cooperating with the telecom industry to identify locations suitable for greenfield projects. However, there are still plenty of municipalities opposed to new deployments. Training sessions on the impact of radiation and the safety of towers have been organised within various municipalities with the concerted efforts of public entities and industry players.

Community acceptance remains the number one challenge in Colombia

The Colombia roundtable discussion dwelt at length on the community and the necessity to educate the population on the real value brought in by the telecom industry. In spite of the fact that connectivity is a sought-after service in Colombia, there are still plenty of rural and suburban communities fighting against the installation of new sites.

People tend to complain about Colombia’s poor QoS but on the other hand, oppose new sites because of the fear of radiation. The reality of working with and educating local communities tends to represent a bottleneck in terms of project timelines, but is also the only way to ensure that projects can be developed.

Local communities lobby not only against new sites but also in an effort to ensure that noise produced by generators is reduced. The industry has responded by reducing the noise emitted by generators and is now introducing smaller and quieter equipment. Camouflaged towers are now increasingly popular in the country in an attempt to reduce the visual impact of new sites.

The reality is that with the advent of 4G LTE, cell site densification is a necessity and towercos and carriers alike have to engage the population to ensure they obtain their buy-in, especially since it’s been estimated that the country needs as many as 10,000 new sites over the next three years to reach optimal coverage.

With each municipality able to establish their own rules, towercos certainly don’t have an easy task when it comes to obtaining permits. Colombia has not seen the same level of involvement by the central government in standardising permitting processes as we’ve seen in Brazil and Peru.

The new 4G auction will push cell site densification

The upcoming 4G spectrum auction, which follows the auction held in 2013, will create an obligation for carriers to share infrastructure as well as provide coverage in 40 remote areas in the 1,900MHz band in 50 additional areas in the 900MHz. And with these obligations, more towers will be needed.

As previously mentioned, it’s been forecast that these coverage goals will require an additional 10,000 towers to be met. Coverage challenges are compounded by capacity issues; there is rooom for improvement in QoS in the country as users experience plenty of dropped calls on a daily basis.

Back in 2013, Claro, DirecTV, Avantel, Tigo Colombia (in a joint proposal with State-owned ETB) and Movistar were awarded several blocks to rollout 4G networks with substantial coverage obligations. However, to date only 5% of mobile users are actually connected to 4G. The upcoming auction will put a serious strain on carriers and require considerable investments as well as a dedicated effort to engage local communities in the process.

Government and regulatory challenges

The regulatory environment does not seem as favorable toward the towerco business model in Colombia as in other CALA countries. For example, there isn’t the same pressure on dominant operator Claro as seen in Mexico, the National Law designed to ease permitting has not to date prevented local government entities and communities from blocking site construction or closing down sites, and it was only as recently as 2013 that the spectre of asset nationalisation was raised in a Senate proposal. The Colombian government also owns a 50% minus one share stake in the combined Tigo and Une-EPM entity.

Security: rural vs urban

Experts report that towers built in remote areas, where the logistics can be extremely tough, tend to be safer and protected by the local community which sees connectivity as a major leap forward. On the other hand, urban projects are sometimes hindered by corruption and we’ve heard reports of tower owners being asked to be asked to pay fees to criminal gangs in exchange of access to a certain neighbourhood.

Conclusion

In conclusion, in spite of some challenges represented by Claro’s dominant position, the huge number of towercos already present on the territory and the opposition of local communities to cell site construction, Colombia is perceived as a healthy market and one where towercos still have plenty of opportunities. With 10,000 new sites likely to be planned and deployed over the coming years, Colombia is one of the most active and attractive markets in the CALA region.