Southern Europe (for the purposes of this article: Spain and Italy) might conjure up images of good food, good wine and a relaxed way of life, but in terms of telecoms towers, there’s very little that’s laid-back about this market. Acquisitions, take overs, IPOs and over US$1 billion spent in the last three years paint a picture of a region which is at the forefront of Europe’s independent towerco revolution. Dominated currently by Cellnex (formerly Abertis Telecom) but with a healthy number of smaller towercos and with new competition poised to enter the market in the form of TIM’s listing tower business Inwit, Southern Europe may well be the test bed for the independent towerco model before it rolls out across the rest of the continent.

Market overview

Although Southern Europe took an economic battering during the recession, Spain and Italy seem to be recovering from the negative growth they suffered after 2008. Although Spain’s austerity measures drove unemployment to a high of 27.7% in 2013, rising labour productivity and lower inflation have helped to improve foreign investor interest in the economy and to reduce government borrowing costs. The government’s ongoing efforts to implement reforms – labor, pensions, health, tax, and education – are aimed at supporting investor sentiment. The government also has shored up struggling banks exposed to Spain’s depressed domestic construction and real estate sectors by successfully completing an EU-funded restructuring and recapitalisation program in December 2013.

As a founder member of the EU, Italy is Europe’s third-largest economy. Public debt has increased steadily since 2007, topping at 133% of GDP in 2013, but investor concerns about Italy and the broader euro-zone crisis eased in 2013, bringing down Italy’s borrowing costs on sovereign government debt from Euro-era records. The government still faces pressure from investors and European partners to sustain its efforts to address Italy’s long-standing structural impediments to growth, such as labour market inefficiencies and widespread tax evasion.

The telecoms landscape - Spain

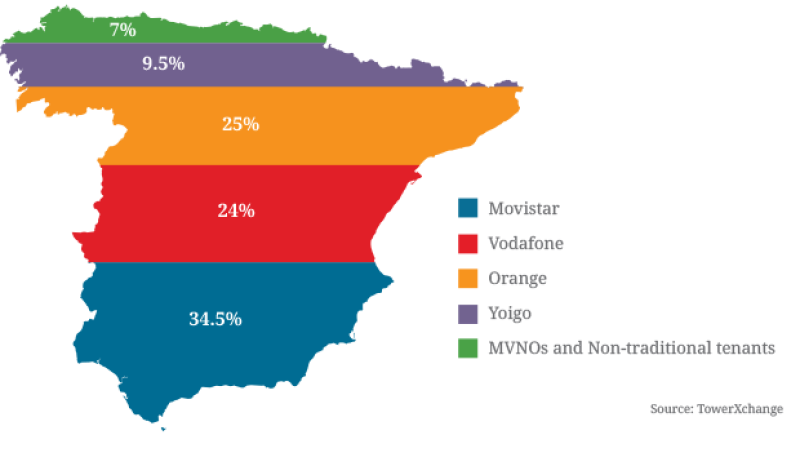

With over 109% mobile penetration and a growing 4G market, Spain’s mobile landscape is lead by Telefónica’s Movistar, which has been operating in Spain since the launch of GSM services in 1995. Second place in the market is hotly contested, with Orange just drawing ahead of Vodafone in 2014. Some way behind the three leaders is Teliasonera’s Yoigo, which launched in 2006 and which shares a significant proportion of its network with Telefónica.

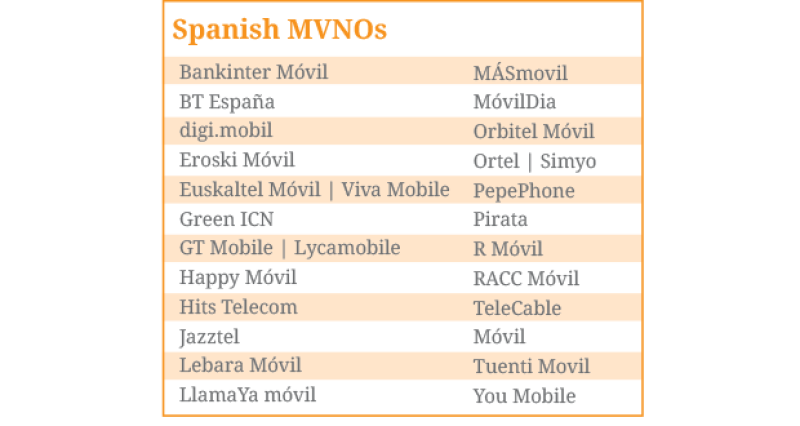

Although no firm data is available, MVNOs in Spain hold a reasonable chunk of market share and TowerXchange estimates that Spain’s MVNOs (including Jazztel whose acquisition by Orange should increase the latter’s mobile market share by 3%) account for around 7% of the market - see the infographic for a list of Spanish MVNOs. Orange’s bid for Jazztel was approved by the EU competition watchdog in May 2015 and is expected to close for €3.4bn in the next few weeks. Another integrated services provider with some mobile market share, Ono, was acquired by Vodafone in July 2014 for €7.2 billion, indicating that the fight to gain the upper hand in terms of market share as well as diversification into broadband and entertainment services is driving a highly competitive market in Spain.

Mobile market share in Spain

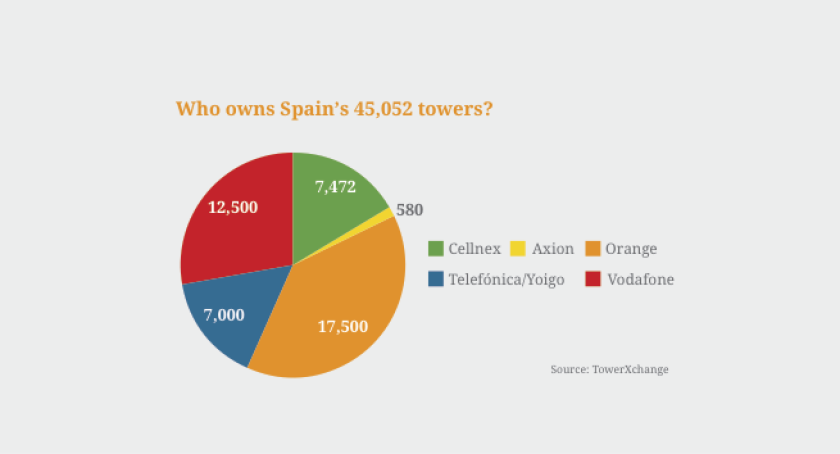

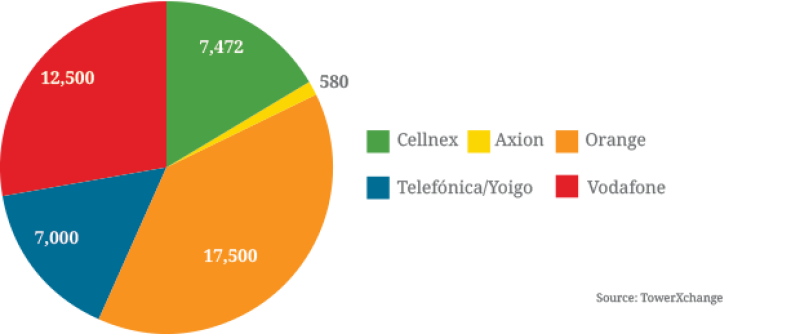

Who owns Spain’s 45,052 towers?

The telecoms landscape - Italy

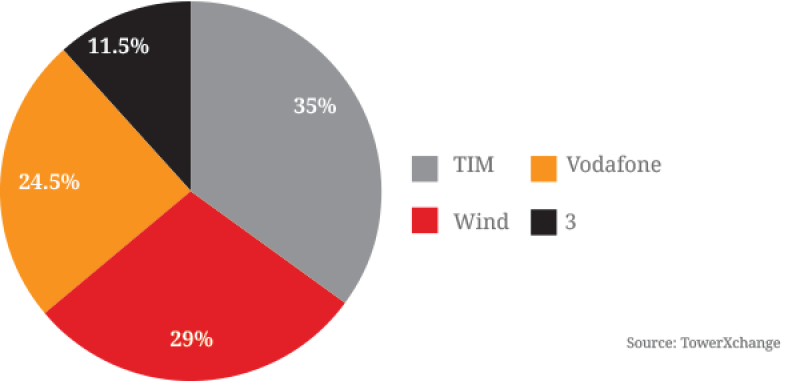

Another four-operator market, the owners of Italy’s mobile network operators have been beleaguered by debt and the need to fund ambitious growth plans on other continents, creating a further driver for consolidation and asset divestiture. The market is led by the former national operator, Telecom Italia (TIM), whose offering across mobile, fixed line and broadband gives them a solid lead in the country.

With Vodafone securely in second place, a merger between the third and fourth ranked operators in the market, Wind and Three, may take place in 2015, although at the time of writing there were still some niggles in the long running discussion in terms of management and board representation. LTE+ is currently rolling out in major cities in Italy, and market penetration stands at around 144%, one of the highest penetration rates in Europe.

Mobile market share in Italy

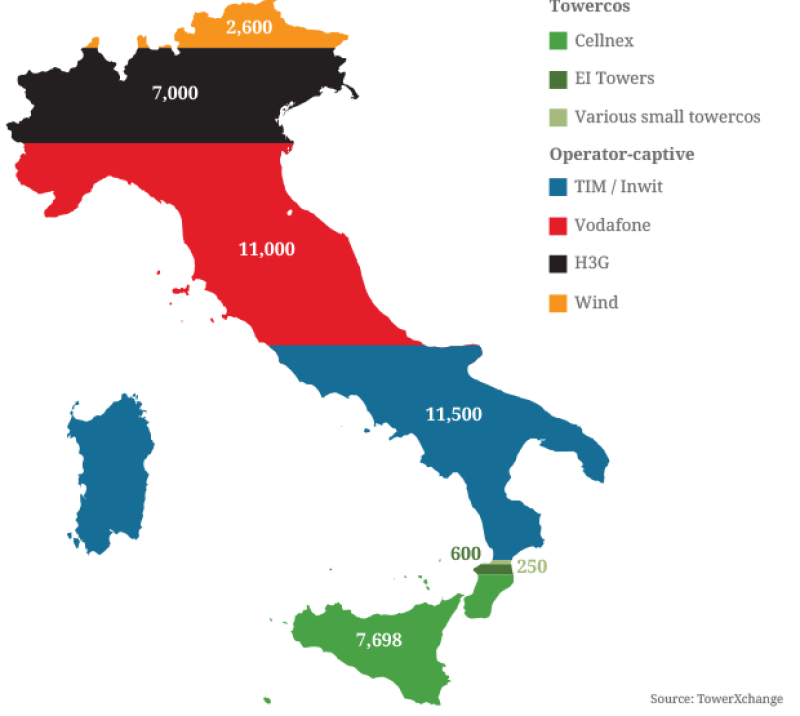

Who owns Italy’s 41,419 telecom towers?

The telecom towers landscape

TowerXchange’s sources tell us that there are around 45,000 telecoms towers in Spain in total, the majority of which are still operator-captive. Cellnex (formerly Abertis Telecom) own 7,472 towers, acquired over multiple phases from Telefónica and Yoigo in 2012, and Axion hold around 580 towers in the south of the country. Despite rumours of subsequent tower divestment, the majority of towers remain under the control of the operators with 17.8% of the Spanish market’s towers in the hands of independent towercos.

By contrast, we estimate that around 48% of Italian towers are currently controlled by independent towercos, in what is quickly becoming one of the fastest-moving and hotly-contested markets in Europe. Cellnex’s portfolio in the country is made up of 306 sites acquired from TowerCo (a mixture of towers, sites and points of service) and their most recent deal with Wind, in which they acquired 90% of the equity in Wind’s towerco Galata, 7,377 towers, for €693mn. This gives Cellnex a total of 7,698 towers in Italy, all acquired within the last three years. Additionally, Italian towerco EI Towers owns a portfolio of around 2,500 towers in Italy, of which around 600 are pure telecom towers and the remainder are broadcast towers. TowerXchange also believes there may be as many as 45 small ‘mom and pop’ towercos in Italy, mainly in the south of the country and each owning a handful of towers across private property, bringing the total estimated number of towerco sites in Italy to around 20,067.

Additionally the former state broadcaster Rai Way owns 2,300 broadcast towers nationally which are not yet widely offered to the telecoms market.

Of the remaining 21,352 sites still owned and run by operators, Telecom Italia holds the largest share with 11,519 towers, although with those assets transferred to Inwit, and Inwit set to IPO imminently, they will soon be considered towerco assets.

Towercos, acquisitions and takeovers

The Spanish market is currently dominated by Cellnex, although smaller towerco Axion has been present in the country since 1999 and currently operates 580 sites, mainly in the Andalucia region. Axion was acquired by Antin Infrastructure Partners in 2011, the same investor who founded FPS Towers in France. TowerXchange believes that Axion has grown through built to suit, with no significant telecom tower acquisitions reported.

Cellnex’s recent IPO has raised significant interest (see Cellnex IPO a landmark in the emergence of a European tower industry on page XX) and has given the company a level of credibility which will allow them to propose partnerships with Europe’s biggest operators based on opex reduction, rather than solely based on the need to release cash through the sale of towers, as has been the case in many European deals to date. In summer 2014 Reuters reported that Orange had commenced a process to sell around 9,400 towers to an independent towerco, although this deal has not gone ahead as yet. It seems feasible that Cellnex’s new proposition may reignite the interest of Spain’s remaining operators in monetising their towers.

Given Orange’s experience of divesting towers in Africa, it is not implausible that they may be interested in divesting towers in order to reduce their opex commitments, and the motivation that tower valuations not suffer from ‘last mover disadvantage’, particularly given the extensive site crossover in the Spanish market currently, may encourage the operator to reconsider the sale. Meanwhile, Vodafone seem less inclined to divest tower assets, preferring to structure network sharing joint ventures such as CTIL in the UK and Indus Towers in India.

In Italy, the market is far from settled. The most imminent and significant change to the tower landscape in 2015 will come with the development of Telecom Italia’s tower assets. As this article is written, Inwit, Telecom Italia’s towerco division, is pressing ahead with an IPO of their towers, believed to be valued at up to €2.34bn and seeking to raise €936mn from listing a 40% stake in the company with a share price set from €3.25-3.90. Rumours of an outright trade sale to Cellnex had previously been voiced, and it would certainly make sense from Cellnex’s point of view to consolidate their position in the Italian market and eliminate a potential competitor, but as the IPO plans progress, it seems less and less likely that the towers will be acquired. Most recently, rumours have also hit the market that Inwit may have an interest in acquiring non-Telecom Italia tower assets themselves in order to become even more competitive in the market – this is backed up but rumours of potential M&A activity with the former state broadcaster Rai Way.

TowerXchange expects to see a more pragmatic language of partnership coming from both Cellnex and Inwit when the IPO progresses as both parties aim to cooperate in order to minimise the commercial impact of any duplication on their portfolios. Inwit will benefit from an existing strong relationship with Vodafone, which represents the lion’s share of their second tenancies, and the potential merger of 3 with Cellnex’s anchor tenant Wind means the Italian market will continue ti restructure, and both towercos are also aware that the Italian government is watching with interest.

We are also continuing to monitor the attempts of EI Towers to gain a significant stake in former national broadcaster Rai Way. At the time of writing, EI had submitted two proposals for acquisition, initially for at least 66% of the company, then reducing their required stake to just 40% after their bid was blocked by government. On May 5 2015 it was widely reported in the business press that the EI Towers board were under investigation for stock price manipulation, and since this time no news has been released on any potential developments.

What’s next?

TowerXchange is in little doubt that Cellnex will be aiming to make more acquisitions in Europe over the next 12 months, and it seems likely that the familiar territory of Southern Europe will appeal to them in this respect. In addition, Inwit’s impending IPO, EI’s ambitions and the probability of further consolidation in the market means there is no risk of a slowdown in the immediate future.

Cellnex seem confident that their IPO and the highly visible support that the process has lent them means European operators will be more open to divestment for opex reduction purposes, rather than just for a cash injection. If this is the case, we may well see competition amongst European operators to bring their towers to market quickly to achieve the best valuations and avoid ‘last mover disadvantage’. With less than 20% of Spanish towers currently managed by independent towercos, and with further tower assets in play in Italy, there is certainly room for more activity in this part of the world.