Some of the critical stakeholders in the development of the Peruvian telecom tower market assembled for the annual round table at the TowerXchange Meetup Americas in May 2015. Here we share insights from their conversation, plus TowerXchange’s own analysis of a tower market poised for transformational growth in the next three years.

Entel shakes up mobile market

Peru was effectively a comfortable, relatively slow growth duopoly between Movistar and Claro with Nextel only active in the big cities, but Entel’s acquisition and nationwide vision has stimulated network investment.

One towerco suggested that their biggest concern was that carriers were spending aggressively on customer acquisition at the expense of investing in the networks – certainly the incumbents operators were reportedly nervous about competing with the new entrants.

It is clear that there is plenty of room for tower market growth in Peru, which has one of CALA’s lowest SIM penetration rates (101% according to GSMA Intelligence, Q4 2014).

There is currently a fledgling 4G market, but the three market leaders all have launched. Claro, Movistar and Entel’s 4G services already account for over 4% of subscribers. Movistar and Entel secured spectrum in AWS band and, although Claro bid unsuccessfully, they cleared spectrum in the 1900MHz band which had become largely redundant in the delivery of 2G services. More spectrum is coming with a 700MHz auction imminent.

In terms of infrastructure sharing; Movistar has been the most inclined to share but Viettel have to date remained reluctant, while Claro is also less motivated. RANsharing has been observed in Colombia, although not yet in Peru, although it may only be a matter of time until RANsharing is undertaken the country.

Non-traditional tenants could play important role

Peru has a good crop of non-traditional carrier tenants, including WiMAX provider Olo, which plans to rollout 1,000 LTE BTS. ISP Movilmax was also launched in early 2015.

DirecTV also plans to launch an LTE fixed-wireless service on top of their content delivery systems, but may enter the mobile market in future. This raises the issue of what the implications will be if and when AT&T acquires the company. DirecTV tends to be taking tenancies at 120’, typically in clusters within cities, particularly in Lima. DirecTV had previously issued search points instead of search rings, but they have since changed their outlook.

Viettel is only building a fixed network; they’ve announced mobile services but were yet to launch at Q1 2015. Their tender requires deployment within one year. When they first entered the market, Viettel’s declared intent was to discount mobile rates by 25%, but rates have since reduced regardless. Viettel puts an emphasis on low cost, accelerated deployment, and has used a similar strategy in other countries such as Mozambique. At least one towerco in the region reported that they had sold co-locations to Viettel.

Stakeholders bullish about Peru’s tower market

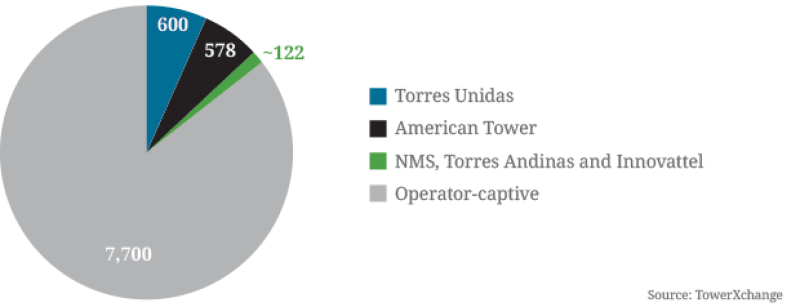

Towercos currently own a little over 14% of Peru’s 9,000 towers. Ground rent is a pass through pro rata.

Telefónica (Movistar) have already sold 468 towers to American Tower back in 2010. Torres Unidas now claims to have over 600 sites in Peru, having acquired 350 from Telefónica. Torres Unidas has the right of first refusal to buy the Olo portfolio.

In terms of growth potential, one towerco stated that “tenancy growth is huge, we’re building tremendously”. Over a three to four year horizon all the towercos were bullish about average tenancy ratios reaching around two, although, much of the predicted growth rates depend on whether AT&T is behind DirecTV. The Ministry of Transport and Communications has called for an increase from 9,000 to 22,000 cell sites over the next three years, an increase of almost 2.5x in tower stock.

one towerco stated that “tenancy growth is huge, we’re building tremendously”. Over a three to four year horizon all the towercos were bullish about average tenancy ratios reaching around two, although, much of the predicted growth rates depend on whether AT&T is behind DirecTV

Who owns Peru’s ~9,000 towers?

Record breaking build to suit

American Tower added a greater percentage of new sites in Peru than anywhere else worldwide in Q4 2014. Last year 1,300 new sites were deployed by Entel, which were all outsourced to towercos. There has also been plenty of capex deployed already, for instance carrier announcements suggest:

Claro is investing just under US$1bn to extend coverage and capacity between 2015-17

Telefónica is spending US$1.8bn between 2014-16; Telefónica added 1,432 new sites in 2014 alone

Entel is deploying capex of US$1.2bn between 2014-19

Viettel is spending US$400mn installing 2,000 towers and laying 15,000km of fibre

Whilst one towerco suggested they anticipated a substantial build in Peru to continue steadily over the next two to three years, another towerco suggested that there would be fewer builds this year. They suggested that of the DirecTV search rings, 95% of rings could be served with one of their existing towers, summing up that they felt that around 200-250 new towers would be built this year in Peru. Two of the other towercos felt that estimate was pessimistic, one suggesting that Entel were likely to issue ~280 new search rings, requiring both GBTs and rooftop sites, albeit that permitting of many the required greenfield sites would be challenging as many are sites Entel were unable to secure and construct themselves.

In summary, there was consensus that 2015 was likely to be slower than 2014, with 2016 likely to be a better year for new site builds in Peru. But in general, Peru remains one of CALA’s fastest growing tower markets.

Rooftops, masts and towers

Quality contractors for rooftops, masts and towers are hard to find in Peru, and can be more expensive than other countries. One towerco suggested that most build-outs consisted of rooftops, typically with 6-9m structures, for which they had to reinforce a large number of roofs, complicated by the fact that a lot of neighborhoods didn’t have a registry of plans.

The most in demand structures seemed to be 24-30m towers and 6-9m poles. Regulations require the use of particularly strong bases.

Participants report that, to date, there there has been enough steel available locally to meet demand for telecom structures.

Urban and rural fibre

Peru has fibre all along the coast and in the big cities. A ‘National Fibre Backbone’ has been launched with a focus on connecting farther-flung regions where it hadn’t been economic to deploy fibre to date. Therefore, most round table participants didn’t see the National Fibre Backbone project having much impact on their more urban-centric activities.

Meanwhile, it seemed that Viettel had been installing fibre all along the coast, typically hung from electrical poles.

Regulation; permitting eased, but looming spectre of regulator interference in pricing

Peru’s previously notorious permitting regime should be eased by new legislation coming into law this year which creates a uniform administration process. The new regulation tries to regularise all towers before 2012. These regulations mean that if a tower operator applies to a municipality for a permit, and if that municipality doesn’t respond, then the tower operator has a de facto license.

The new regulation creates exact parameters of how a permit application filing needs to look. As a result a file cannot be rejected unless there is a genuine failure in the filing. However, the municipality has up to two years to respond, but if they find an error in your application they can make you take the site down.

The regulation also includes some common elements from the Chilean ‘Tower Law’, such as some potentially expensive guidance on concealment.

This regulation was approved by the President a couple of weeks prior to TowerXchange Meetup Americas 2015, and is retroactive.

Whilst the regularisation of permitting process is seen as positive, Peru’s tower regulation has not been universally welcomed due to a requirement to submit Service Level Agreements (SLAs) and lease rates quarterly. The regulator also claims they have the right to “implement measures”.

Whilst the regularisation of permitting process is seen as positive, Peru’s tower regulation has not been universally welcomed due to a requirement to submit Service Level Agreements (SLAs) and lease rates quarterly

One towerco is working to modify the law and has refused to comply, suggesting that Ospitel cannot regulate the unregulated tower industry, and that “intrusion into lease rates is something none of us need.” The same towerco called for support from his peers in lobbying the Peruvian regulator: “it’s important all towercos sing from same songsheet”.

As the conversation at the Peru round table evolved, it became apparent that Peru’s tower regulation is not enshrined by an Act of Congress, meaning the regulators are able to regulate only licensed operators. They cannot regulate an unlicensed operator. So companies are only required to comply if they register in national registry of tower operators. The incentive to register is that you get to use the new law to get permitting law. Alternatively, at least one tower operator has declined to register and be regulated, forgoing the new permitting law, using the old processes, but avoiding the obligation to share SLAs and lease rates, and thus minimising the risk of the regulator interfering with lease pricing.

It is reportedly more difficult to build under old regulations. While it should be easier to secure build permits under the new regulations, once you gain a permit you may still have to overcome community objections.

No property tax is applicable in Peru unless you own the site, even then it’s relatively small

Power and security

Power in Peru is generally reliable, and backup gensets remain the responsibility of operators. Torres Unidas has nine off grid sites among over 600 sites, although there may be more needed as they move further inland.

Connection to the national grid is usually undertaken pretty fast. There is also not much theft reported in Peru. While one towerco had had a couple of sites attacked by drug traffickers, and like most countries there are a few small pockets where infrastructure builders would be reluctant to go, in general the security situation in Peru is good.

Conclusions

TowerXchange are bullish about the prospects for the tower market in Peru. Claro and Movistar’s comfy duopoly is already being challenged by the acquisition of Nextel by Entel, in particular their ambition to scale from an urban to a nationwide footprint. Entel could monetise their passive infrastructure in Peru to fund the nationwide expansion and 4G rollout.

In addition Viettel and, in particular, Olo and DirecTV (potentially with AT&T) represent the potential for further builds and tenancies.

There are good opportunities for organic growth in a market where the government has called for an increase from the current 9,000 to 22,000 towers. There have also been efforts to create an enabling regulatory environment, in part welcomed by towercos, intrusion into lease rates notwithstanding.

Peru is now a priority market in the CALA tower land grab. Torres Unidas and American Tower are expected to face increased competition in 2015 from other acquisitive towercos. This will create investment and sale opportunities for independent developers.