The growth opportunities and the cash flow generated by Brazilian towers more than justify tower companies’ investment. However, on the Brazil round table hosted by David Porte, SVP of Operations for SBA Communications, the conversation turned to what was broken, and what needs fixing in the Brazilian tower market. Here the top ten challenges identified by an illustrious audience featuring five Brazilian towercos, as well as former tower strategists from Vivo, Oi and ON Telecom.

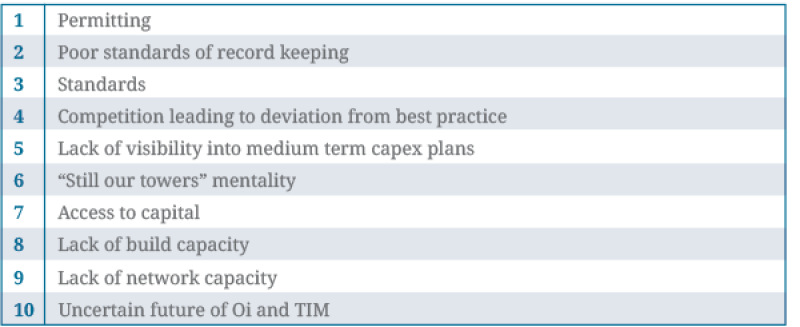

Top ten challenges facing the Brazilian tower industry

1. Permitting

Brazil is notorious for the complexity and amount of time it takes to progress from permit application to permission to build. “I wouldn’t call permitting a challenge because there’s nothing fundamentally wrong, but the biggest opportunity is to fast track permitting,” said one towerco.

Brazil’s Antenna Law, the Lei das Antennas, recently came into force, creating a standard approach to permitting across all municipalities, and introducing a 60 day ‘shot clock’.

Even before the Lei das Antennas takes effect, another towerco suggested “It’s a myth that it’s almost impossible to permit green field sites in Brazil. As long as you understand the path you must follow, it’s not necessarily more difficult than permitting anywhere else – in fact, I’ve found permitting in the Northeast of Brazil, which is relatively under-developed, easier than in the US.”

If securing a permit for a new site is not as complex as one might fear, there seems little doubt that fixing the legacy of permitting shortcuts remains Brazilian towercos’ number one challenge: “The rock you we most often fall on is permitting,” said one towerco. “Brazilian cell sites fall into three categories; fully permitted (which we call unicorns!) Permittable – sites that are compliant but for which a full set of permits were never attained. And unpermittable sites. The biggest challenges arise if the law changes and a site which was once permittable becomes unpermittable!”

2. Poor standards of record keeping

The poor standard of record keeping for the sites the towercos have acquired in Brazil has created a backlog of paperwork. Even where sites are fully permitted, documentation is not always complete, and municipalities seldom have duplicate copies. Whilst clearing the paperwork backlog remains a work in progress, a many of Brazil’s cell sites are not fully permitted.

As a legacy of forgotten bi-lateral swaps, the paperwork for which may have been lost, it is not unusual for a carrier to not be aware that they had an operating BTS at a third party site until the towerco tells them (and sends them a bill!) Likewise, tenants seeking co-location report frustration that the towerco’s asset register might suggest that capacity is available, yet when they get to the site unregistered, often unused, equipment hanging on the tower means capacity is not readily available.

3. Standards

One towerco complained that carriers pressing unrealistic timelines forced towercos to deviate from tower permitting and building best practices and standards. It was agreed that it was critical to adhere to common standards governing the capacity of structures and installation of fencing, standards for safe practice when working at height, and general standards for tower building.

The standards challenge is accentuated when the original drawings of an acquired site have been lost. We’ve heard of instances where a tower portfolio was offered for sale with no site drawings at all, which obviously makes it more complex to evaluate the structural quality of a portfolio.

“We’ve acquired 35 year old sites where we don’t even know the rebar,” said one towerco. “So we have every level of standards compliance from fixing those kind of scenarios to green field sites which we’ve built to our own high standards from the outset.”

4. Competition leading to deviation from best practice

As a function of the sheer amount of building and buying of towers in Brazil, and overheated competition, it again becomes difficult for the tower industry to standardise best practices. For example, the majority of towercos would love to standardise on a principle that no-one builds towers without permits, but if aggressive competitors are going to cut corners with permitting to accelerate time to market and secure build to suit contracts, those standards and best practices can be sacrificed as people try to build market share.

Long term revenue assurance is critical. This is why the robust MLAs of the established towercos are so important, and why it is critical that independent developers don’t deviate too far from the established business model. For example, if a carrier is granted a zero cost cancellation in their MLA, there’s zero revenue assurance, and that can be tremendously value destructive. Only a little less value destructive are cases where the carrier can cancel with payment of 20-30% of the remaining lease value. Even granting swap provisions, where a tenant has the right to swap 10% of their tenancies to other sites, adversely affects additional revenue potential.

5. Lack of visibility into medium term capex plans

License obligations require that Brazilian carriers build in new areas, yet the towercos report that they have very little visibility into the medium term network capex deployment plans of carriers – the issuance of new search rings will often be the first towercos hear about network extensions. The Brazilian government has identified 5,570 ‘cities’ (municipalities) which must be served by mobile operators in the coming years, yet the operator with the greatest coverage, Vivo, provides coverage in only 67% of those municipalities, with the other carriers lagging even further behind. While market-driven network extensions are always going to be unpredictable, extensions driven by compliance with ANATEL’s coverage obligations should be more predictable than they are.

This lack of visibility implications for finance too, with a comparison to the US market made by one round table participant: “AT&T deployed huge capital in the US last year, but this year they’re buying DirecTV instead. When a big carrier hits the brakes, there’s a risk that the towercos can go out the window. Whilst it remains difficult to predict carrier’s capex over the medium term, the financiers always ask for a five year prediction.”

6. “Still our towers” mentality

In the early stages of towercos participating in a market there is an immature, undefined relationship between towercos and carriers. We heard anecdotes where carrier’s staff had cut the towerco’s locks off a site and replaced them with their own – “they are still our towers” remains the attitude of some carriers’ employees, even after the CFO has sold them!

Attitudes change over time. Carriers come to understand that towercos are not just another supplier, they are a partner and landlord. “I’ve been into meetings where the carrier would slide their MLA across the table to us and demand we agree to their lease terms,” said one towerco. “It just cannot work like that. Because we share infrastructure, everyone has to be subject to same rules.”

7. Access to capital

How can we structurally improve access to long term capital for the domestic Brazilian tower market? Securing debt financing at reasonable rates was highlighted as a particular challenge, and one which continues to make it difficult for Brazilian towercos to compete with US firms with access to low cost capital and cheaper interest rates; “it’s hard to borrow at 13% and make money in the long term,” complained one local developer. One round table participant reported that the BNDES (Brazilian Development Bank) loan programme could be accessed but that it only covered new build sites, and it required that BNDES own first title on the steel.

Securing debt financing at reasonable rates was highlighted as a particular challenge, and one which continues to make it difficult for Brazilian towercos to compete with US firms with access to low cost capital and cheaper interest rates

8. Lack of build capacity

Despite the aforementioned overheated competition, voracious demand for new sites suggests that Brazil may have capacity for two to three times as many build-to-suit towercos as currently operate in the market. Certainly the sources TowerXchange have spoken to have suggested Brazil’s carriers would build more towers if they could!

The Brazil round table discussion highlighted Brazil’s particular deficiency of transmission sites.

9. Lack of network capacity

There is plenty of room for improvement in QoS in Brazil. Networks are maturing to the point where the carriers will compete less on coverage and more on capacity and QoS, which will improve medium term planning as networks densify.

10. The uncertain future of Oi and TIM

Continuing speculation about the future of struggling #4 carrier Oi continues to create uncertainty. Oi reportedly has a negligible capex budget, has built very few new towers, and acquired no spectrum in recent auctions. The future of TIM Brasil also remains uncertain, although they have not been as hamstrung in terms of deploying capital. If consolidation in Brazil is inevitable, it can’t come soon enough.

Conclusions

Claro notwithstanding, Brazil’s carriers have sold almost all their towers. As with any industry where non-core activities are outsourced, the reality is that the carriers didn’t care as much about their towers as they did about their subscribers, so improvement capex must be deployed. The costs of bringing towers acquired from Brazil’s carriers up to standard are embedded into towerco’s business plans – and accelerating the process of bringing those towers up to standard represents a critical opportunity for towercos to add value.

Carriers are gradually learning how to co-operate better with their towerco partners, giving them better visibility into medium term plans, and therefore more time to deliver according to standards and best practices, ultimately delivering a better quality of service to both tenants and to their subscribers.

The Brazilian tower industry is lead by an accomplished group of people with an acute understanding of these challenges, and I believe the best way to overcome such challenges in any market is to hand the towers over to a professional tower company and let them clean them up

Permitting remains Brazil’s number one challenge. It is critical that the Lei das Antennas be implemented swiftly and consistently by all municipalities to facilitate a predictable, accelerated permitting process, unlocking the carriers and towerco’s maximum investment in Brazilian telecoms infrastructure. Brazil has a legacy of short-cutting cell site permitting, and towercos are ideally positioned to clean that up. Amid a fiercely competitive market for build to suit opportunities, it is critical that Brazil’s independent tower builders don’t resume short-cutting permitting, or offer cancellation clauses within their MLAs, otherwise they risk harming or destroying the capital value of their sites.

Some US investors have a view of the tower business based on 25 years of doing business in their domestic market – they turn their noses up at emerging markets because “it’s not the way it’s done.” The reality is that there are sites in US with structural problems, and corners are cut when it comes to permitting everywhere in the world, the US included. The top ten challenges faced by the Brazilian tower industry are not greatly different from the top ten facing the US market, and if this article’s attempt to explain “everything you always wanted to know about the Brazilian tower market*” (*but were afraid to ask) has made you less bullish about the opportunity in Brazil, then that was not our intent. The Brazilian tower industry is lead by an accomplished group of people with an acute understanding of these challenges, and I believe the best way to overcome such challenges in any market is to hand the towers over to a professional tower company and let them clean them up.