By Kieron Osmotherly, Founder & CEO, TowerXchange: Since 2012, Cellnex (formerly Abertis Telecom) has acquired 2.5x as many towers as all their competitors combined in large-scale sale and leaseback transactions in Europe. Initially motivated and inspired by the American Tower success story, Cellnex has since stood toe-to-toe to outbid the global tower giant to secure a coveted portfolio of 7,377 towers from VimpelCom’s Italian opco Wind. Those assets have since formed around half of a portfolio brought to market in a landmark IPO on May 7 2015, an IPO which was well received and rewarded with an initial 11% increase, raising Cellnex from an initial valuation of just under €3.25bn to a high of €3.55bn, and heralding a new era of infrastructure sharing in Europe.

Cellnex adopts proven towerco ‘playbook’, adapts for Europe

‘If it aint broke, don’t fix it:’ Cellnex are not deviating unduly from the proven independent towerco business model. Towercos generate predictable, long term cash flows by acquiring and leasing up towers to additional tenants, and by generating ‘amendment revenue’ by leasing extra space to existing tenants for the addition of nextgen technology antennas. Towercos create efficiencies not just through the sharing of infrastructure, but the optimisation of operations and maintenance processes. Towercos also create value through organic growth: so called “build to suit” (BTS) programmes – Cellnex has built 150 greenfield sites to date, and in their investor presentation cite Arthur D. Little forecasts of a further 4,700 BTS sites divided between Spain (3,200) and Italy (1,500) by 2019. BTS opportunities tend to increase during the rollout of nextgen technology, a wave Cellnex is riding with 4G in Italy and Spain.

The towerco business model becomes more complex as a function of the level of engagement with energy and ground rent. However, with energy costs passed through to the tenant at 90% of Cellnex sites, and ground rental costs passed through at 76% of sites, Cellnex is mostly a ‘steel and grass’ business model – which means investors in Cellnex are exposed to less risk than, for example, within sub-Saharan African towercos.

If the core or their proposition leverages the proven towerco ‘playbook’, Cellnex has enhanced it with several unique plays designed to better serve the unique nuances of the European tower industry. For example, Cellnex has always been a telecom and broadcast infrastructure hybrid, and the two business models are good bedfellows, sharing common resources and processes, enabling Cellnex to effectively run diverse infrastructure portfolios on a single SG&A budget. While the telecom tower industry is typically an unregulated growth play, broadcast towers tend to be a more stable infrastructure play – in some markets functioning as a regulated monopoly. In its investor presentation (April 2015), Cellnex breaks down their portfolio into 13,591 telecom assets and 2,922 broadcast assets, of which almost 1,500 assets generate revenue for both telecom and broadcast P&Ls.

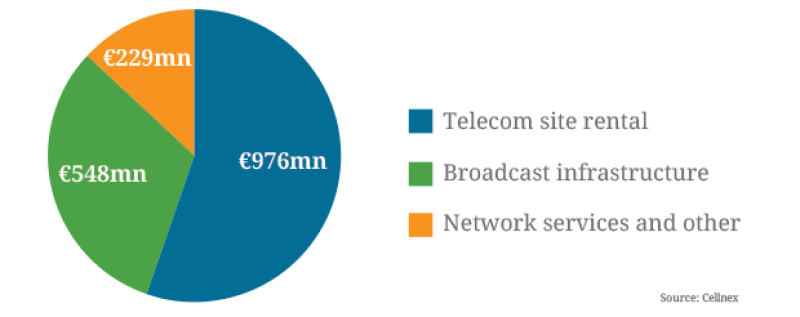

A third Cellnex revenue stream is generated by ‘network services’, provided from 1,430 sites and network assets, the majority of which are also used for telecom and/or broadcast. These assets enable a third ‘Network services and other’ revenue stream into which are bundled public safety and disaster relief services, telecom site connectivity and O&M, and various ‘Internet of Things’ and Smart Cities services.

Cellnex’s ‘triple play’ infrastructure services revenue streams

Another differentiator between Cellnex, many European towercos and their international cousins is the prominence of decommissioning services. While the tower count for every network we’ve studied in Europe is experiencing net growth, new sites for network densification and extension are partially offset by the decommissioning of selected parallel infrastructure. Cellnex decommissioned 129 sites out of an ongoing 221 site decommissioning programme in 2014. However in the majority of instances where models suggest cell splitting for 4G may require cell site densification, overlapping sites are not decommissioned but are mothballed. While decommissioning is a valid extension of Cellnex’s and other European tower companies business models, it should be valued differently from the core towerco business. While decommissioning represents the ‘cream’ of turnkey infrastructure projects, the pipeline of such engagements are at best ‘lumpy’ – decommissioning is a good business, but it’s not the same as the contracted, secure, long term revenues represented by tower leases.

Opportunities in the European tower market

While the African, CALA and certain Asian tower markets have experienced a tremendous volume of tower deals in the last five years, we haven’t seen the same wave of tower transactions in Europe. But that doesn’t mean Europe is a less investible tower market, just a very different market. Europe is seen as representing a more stable cash flow, infrastructure play rather than the aggressive growth play this asset class represents in emerging markets. There isn’t the same organic growth opportunity as in emerging markets in every country in Europe, but there isn’t the same level of complexity and country risk either.

The European tower market is ripe for consolidation. Whilst Cellnex has created a ’hot spot’ in Southern Europe with acquisitions in Spain and Italy, further tower sale and leaseback opportunities may follow both in Spain and Italy as well as in Portugal and Germany in the near term, and across Europe in the medium term.

The European telecom market is relatively under-penetrated by independent towercos compared to other continents, and has historically not needed the capital release that tower monetisation represents. However the cost of fiberisation, spectrum and LTE rollout, compounded by fierce competition and declining ARPUs, has brought many MNOs to reconsider monetising their passive infrastructure.

The European tower market had essentially been stalled by a gap in valuations between MNOs, who coveted the high teen multiple valuations seen in the US tower market, and a more conservative set of infrastructure investors who for a while had seemed to be the only parties interested in European towers, especially whilst the US publics seemed to prefer to deploy capital domestically and in CALA. The acquisitiveness of Cellnex has been critical in bridging Europe’s valuation gap. While I do not feel Cellnex have overpaid to build Europe’s first genuinely independent towerco of scale, their transaction counterparts have generally been able to secure full value. Finding that "win-win" middle ground has attracted other MNOs to consider divesting assets, which in turn has attracted competitive bidders and a flow of capital into European towers. Cellnex have been a ’market maker’ in European towers, a title their successful IPO gives them the capital to defend aggressively.

“The Americans are coming”

When speaking to key stakeholders in the emerging European tower market, we encounter two views: “hooray, the Americans are coming” and “oh no, the Americans are coming!” Opinion is divided as to whether the ’Big Three’ US towercos’ prospective entry into new European countries is a good thing – those in favor are either selling assets and looking to maximise valuation, or feel sellers need more than one credible buyer to feel they can maximise returns, while those opposed feel native European towercos have the digestive capacity to absorb European towers and that the participation of the US publics will drive up prices.

It seems clear that American Tower are keen to own more than a couple of thousand German towers on the continent, hence American Tower were reported to have bid on the Wind assets which Cellnex ultimately acquired. SBA Communications and even Crown Castle might also have an interest in Europe, and it’s not just the Americans who are coming – Indonesian listed towerco Protelindo already has a small portfolio in the Netherlands, acquired from KPN.

In this context, Cellnex’s aggressive bidding to build scale is all the more justifiable, and their IPO all the more necessary both to build an acquisition warchest capable of outbidding established towercos with their low cost of capital, but also to separate Cellnex as a pureplay towerco, rather than it remaining in competition for Abertis’s own capital with other non-telecom infrastructure investments.

A valid benchmark for Cellnex

While Cellnex, has positioned itself to build an ‘American Tower for Europe’, the success story of Crown Castle UK might provide a better benchmark. Through the privatisation of the BBC’s transmission division in 1997, Crown Castle acquired a £75mn revenue tower business in the UK. They supplemented it, invested in it and transformed it into a £233mn revenue tower business by 2003, in the process re-balancing revenues from a 60-40 ratio in favor of broadcast transmission to a 58-42 ratio in favor of the telecom tower and site business. That expansion was fueled by the rollout of 3G, which saw Crown Castle’s UK tenancy ratio surge to 2.9, and which saw the UK tower count rise from ~15,000 in 1997 to ~45,000 in 2003 when Crown Castle successfully exited the UK market through a £1.1bn sale (just over US$2bn, 11x EBITDA) to National Grid Wireless. (National Grid Wireless is now Arqiva, and you can read about the current state of the company in issue 12 of TowerXchange.)

I’m not suggesting that Cellnex will enter and exit European markets like Crown Castle did in the UK, but I am citing a precedent for tower companies to buy their way into a European telecom and broadcast tower market, and add tremendous value through organic and inorganic growth.

Tenancy ratio growth a critical metric

Cellnex has already achieved robust tenancy ratio growth within the telecom sites part of their business, rising from 1.09 in 2012 to 1.43 in 2013 to 1.68 in 2014. Wherever TowerXchange has encountered tenancy ratio growth in excess of 0.2 per annum, we’ve usually been looking at a very healthy tower business. We note that tenancy ratio growth in Cellnex’s “Network services and other” P&L is much lower at .02-.04 per annum, illustrating the differentiation between these business units.

Overview of the current Cellnex footprint in Spain and Italy

While Cellnex is positioning itself as a pan-European towerco, there is ample room for growth within their Southern European base.

In Spain, Cellnex owns and operates 3,704 towers. Axion operates a further 580 towers in Spain, joined by a handful of smaller towercos, bringing the total number of towers owned by towercos to ~4,400 or just under 10% of Spain’s 46,000 towers. The Cellnex investor presentation suggests that an extra 3,200 towers and 10,100 points of presence are required in Spain by 2019.

Cellnex acquired their Spanish portfolio from market leaders Telefónica, who tend to divest towers in selected bundles and may have more to sell. Telefónica’s market leadership in Spain is under pressure from Vodafone and Orange, both of which have retained their towers to date, although in Summer of 2014 Orange were rumored to be considering selling as many as 9,400 of their Spanish towers in a deal which could be valued at almost €900mn. Cellnex’s other anchor tenant is Teliasonera’s Yoigo, the fourth ranked operator in Spain.

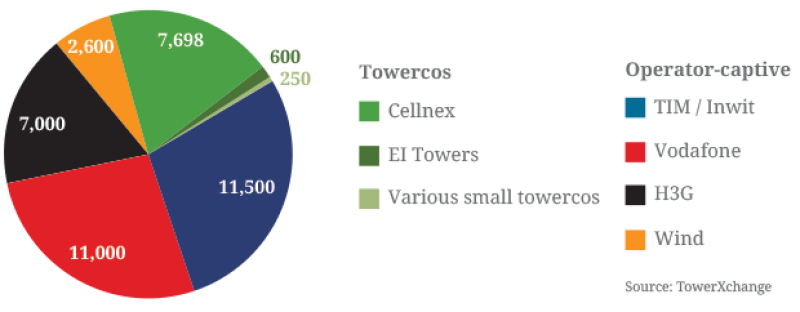

In Italy, Cellnex will own and operate 7,698 towers upon the closing of the announced acquisition of 7,377 towers via the purchase of 90% equity in Galata, Wind’s towerco, for €693mn. Cellnex already had 306 sites in Italy through the acquisition of a company called "TowerCo" for €95mn in June 2014 (although not all those sites were ground based towers, for example 94 were points of service in tunnels). Insofar as towercos are ever really in competition, Cellnex’s main competition in Italy currently comes from EI Towers, estimated to have a portfolio of around 600 telecom towers, plus a couple of thousand broadcast towers. Although they bid for Galata, EI Towers’ focus had appeared to be on the acquisition of broadcast towerco Raiway, a deal which faltered due to political wrangles, with Raiway potentially now on a pathway towards its own IPO. A “long tail” of smaller towercos, some of which could be selectively rolled up to supplement Cellnex’s Italian footprint, brings the total number of towerco owned sites in Italy to ~8,300, or 21% of the country’s estimated 40,400 sites. The Cellnex investor presentation suggests that an extra 1,500 towers and 3,800 points of presence are required in Italy by 2019.

The most obvious opportunity for inorganic growth in Italy would be the acquisition of Telecom Italia’s 11,500 towers, although the company has also filed for an IPO of their tower unit Inwit. The best valuation Telecom Italia could achieve would likely come through trade sale rather than IPO, and there is a precedent for the cash-strapped operator’s divestiture of towers in their recent sale of 6,480 towers in Brazil to American Tower, netting US$1.2bn. While we think a Cellnex acquisition of the Telecom Italia towers is the most likely outcome, obviously an IPO by Inwit would create a competitor of significant scale in the Italian market.

Who owns Italy’s 40,400 telecom towers?

It should be noted that the ’addressable market’ for towercos in Spain and Italy is not necessarily 100% of the towers - for example estimates suggest there are around 7,500 sites in overlapping locations in Italy.

Conclusions

What I like about Cellnex is that they don’t deviate unnecessarily from the proven towerco business model. They may have initially set out to build an ’American Tower for Europe’, and American Tower are a great role model, but Cellnex isn’t merely a copycat venture. Cellnex have refined the towerco business model for Europe, blending telecom and broadcast infrastructure, IoT and decommissioning services into the revenue mix. It’s a hybrid business model and should be valued as such.

Cellnex’s KPIs are solid, with tenancy ratio growth on their telecom assets in excess of 0.2 per annum. While cost per tower is a crude measure, prices in Europe are well below the established US, Brazilian and Indonesian markets, yet leaseback rates are generally healthy.

Having initially planned to sell 55%, Abertis subsequently sold 66% of Cellnex. Abertis had set an initial price range for the IPO at between €12-14 per share, settling at the top end of the range, meaning the IPO would have raised around €2bn. The Cellnex in which investors can now buy stock is currently a Spanish and Italian play, and there is an abundance of further inorganic and organic growth possible in both markets. The mere existence of native European towerco with a significant acquisition warchest to complete with the US towercos is likely to attract more assets to come to market elsewhere in Europe - Cellnex will have no shortage of options to deploy capital and expand their footprint.

Cellnex have kick-started a European market for larger scale sale and leasebacks by finding middle ground between towerco and MNO valuations – they’ve had to be aggressive to reach this point, but we like the assets they’ve bought to bring them to scale. Since 2012 Cellnex (then Abertis Telecom) has acquired ~11,000 towers in European sale and leasebacks, compared to ~4,000 by their peers (split across American Tower and FPS), while another formerly pan-European towerco, TDF, has retrenched to focus increasingly on their domestic French market. Today Cellnex are clear European market leaders in terms of acquisitive towercos, a position endorsed by a successful IPO.

However, there remain reasons for caution on the part of investors. The European tower market is distinct and less proven than the US and Indonesian markets, where listed towercos have thrived.

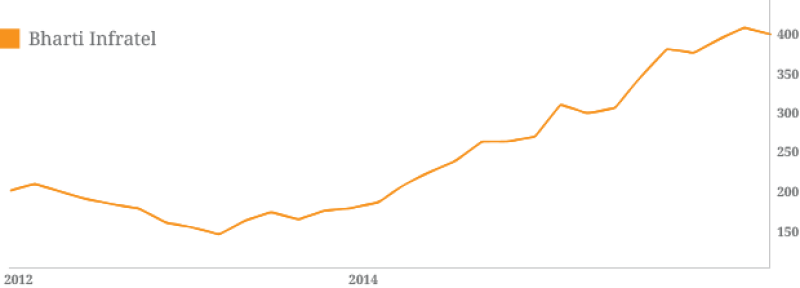

Towercos are also not immune to the vagaries of the global economy; even American Tower, SBA Communications and Crown Castle were almost penny stocks when the bubble burst in 2002-3, and dipped again at the outset of the last recession. The last major towerco listing, India’s Bharti Infratel, lost 37% of it’s value in the first twelve months before recovering and surging to a valuation, at time of writing, around double its stock price at launch. Robust towercos risk being ’the baby that can be thrown out with the bathwater’ when investors get nervous of ’technology stocks’, and the good towercos have ridden out recessions and come out stronger. Investors understand the asset class better now, they understand it is really an infrastructure play not a technology play, and that the model lends itself to high leverage. Towercos continue to attract 3-4x greater valuations than their MNO tenants. Towercos profile as a highly attractive infrastructure investment, a good long hold.

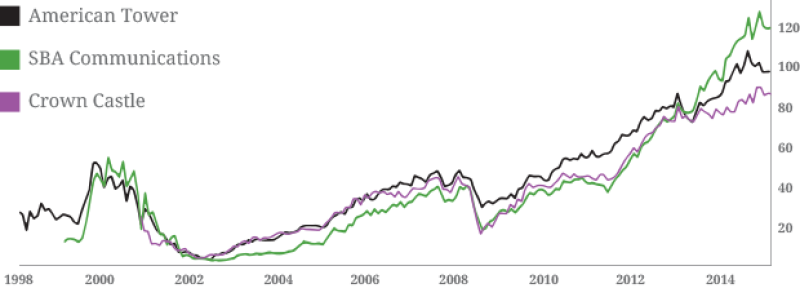

Illustration of the share prices of the ’Big Three’ US towercos (US$)

Illustration of the share prices of the ’Big Three’ Indonesian towercos (IDR)

Illustration of Bharti Infratel’s share price since listing (INR)

Addendum: reflecting on a successful IPO

Cellnex debuted on the Madrid Stock Exchange on May 7 2015 at a price of €14 per share, jumping an initial 11% to a high of €15.7. Cellnex President Francisco Reynés Massanet subsequently revealed that primary investors, joining Abertis Telecom who retained 34%, included U.S. investment fund BlackRock who bought 6.2% of the stock in the flotation, Spanish bank Caixabank who acquired 5% and serial towerco investor George Soros, who acquired 3%. Apparently half of the shares were sold to U.S. investors, which makes sense given their enthusiasm for the asset class, while 25% were from the UK and 10% from Spain.