It seems as though the deal flow in the Indian tower market is resuming again after the slowdown in the wake of the 2012 telecoms regulatory restructuring. Details emerged this week about a major potential transaction with the controlling share of India’s one of India’s largest towercos being put up for sale. The substantial investments being made by the leading Indian carriers in spectrum auctions are starting to have an impact on the market, and the race is on to meet increasing demand for data services and grab a share of the future market for 4G in India. Towercos will be watching closely to understand what this means for the Indian tower market.

Deal overview

Reliance Communications (Rcom), India’s fourth largest carrier is considering the sale of its majority stake in Reliance Infratel, India’s third largest towerco with an estimated 45-50,000 tower assets. The company has requested bids from up to six investment banks to manage the monetisation process and is aiming to conclude the process within the next two weeks. The banks that have already been approached are reported to include Morgan Stanley, Bank of America, Merrill Lynch and JM Financial. Rcom included the following statement in a filing to the Bombay Stock Exchange (BSE): "The company keeps exploring and analysing various strategic alternatives. As one of such alternatives, it has invited certain Investment Banks to make proposals for running a process to monetise the valuable tower and fiber assets held in its subsidiary, Reliance Infratel Ltd, within the current financial year."

Rcom owns a 96% share in Reliance Infratel; the remaining 4% is owned by other investors including George Soros’ Quantum (M), NSR Partners, Galleon, HSBC Daisy Investment (Mauritius), Drawbridge Towers, and Investment Partners B (Mauritius). Rcom will aim to sell a minimum of 51% of its share in the company, and may seek to sell a higher percentage. Rcom will obviously maintain its tenancy on the towers in this portfolio to keep its all-India footprint as it continues to expand its services.

Overview of the Indian market

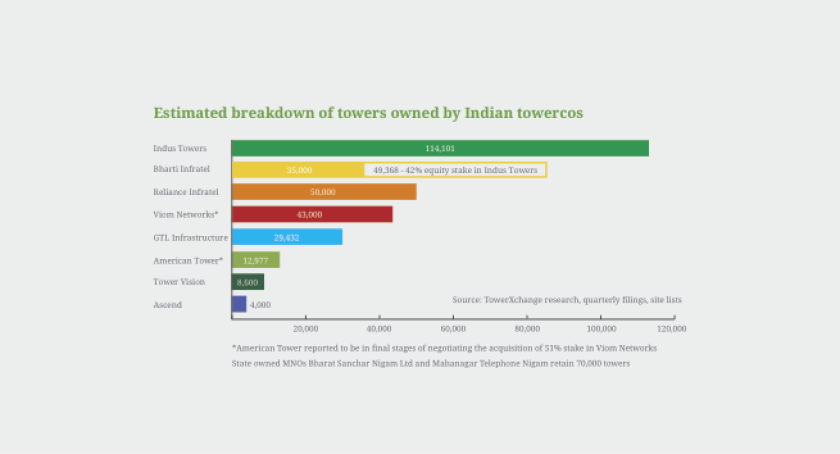

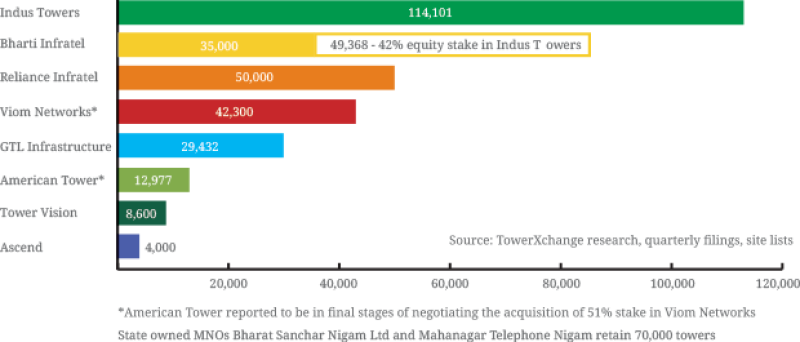

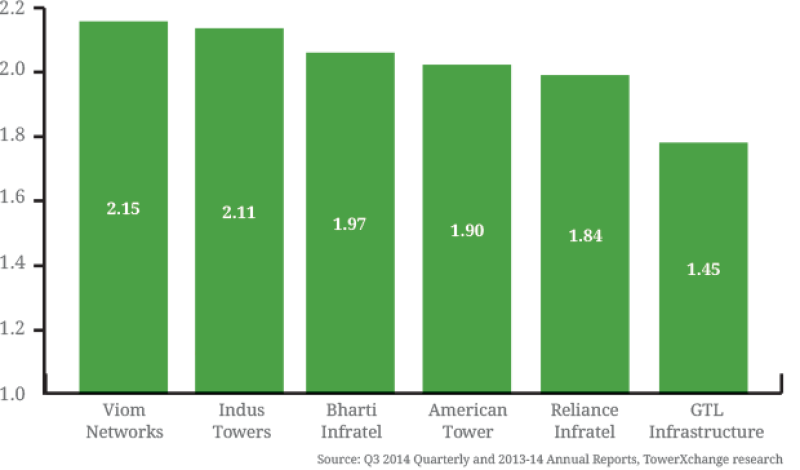

The Indian telecoms market is the second largest in the world with 941mn mobile connections. There are an estimated 400,000 towers deployed in India, providing coverage of 90% of its geography. 70% of these towers are currently operated by towercos, and the tenancy ratios of India’s five largest towercos are at or approaching 2.0, and average ~1.5 across the country.

Over the past seven years operators and towercos have built an average of 50,000 new towers per year to keep pace with the growth of data services in the Indian market. It is estimated that operators and towercos will need as many as 600,000 new points of service (combining new towers and co-locations) to meet the growing demand for 3G and 4G.

Valuing the Reliance Infratel towers

Rightly or wrongly, the general perception is that Indian towers are not worth as much on a per site basis as, for example, towers in North or South America, SSA or Europe. Some of that perception is related to the finely tuned efficiency of Indian tower building, which can see a greenfield GBT built for as little as US25,000. Some of that perception is related to a misconception that India is awash with tenants who struggle to pay their bills - the cancellation of 122 licenses in 2012 has cleared out most of the struggling operators.

Then one must tackle the question as to whether a tower owned by an operator-led towerco such as Reliance Infratel is worth inherently less than a tower owned by a truly independent towerco. Some would suggest that an operator-led towerco might not as aggressively lease up excess capacity to competitors. TowerXchange’s most recent estimate of the tenancy ratio at Reliance Infratel puts it at 1.84 (Q4 2014), suggesting a solid level of lease up, although still lagging Viom Networks, Indus Towers and Reliance whose tenancy ratios are all above two. Ultimately, if a tower becomes more attractive to a network planner if transferred from an operator-led to an independent towerco, it indicates potential pent-up demand for new tenancies.

Determining an accurate estimate of the value of this portfolio is challenging due to the lack of recent deal flow providing comparisons in India. The Economics Times reported that Bharti Infratel has close to 86,000 towers and was valued at about Rs 74,000 crore (US$ 11.6 bn) as of Tuesday, as per data on the BSE.

Based on this estimate Reliance Infratel’s enterprise value should be at least Rs 20,000-25,000 crore (US$ 3.1 bn to US$ 3.9 bn), factoring in its considerable fibre network assets.

Spectrum auctions

Huge investments have been made in spectrum recently with Indian operators spending close to US$50bn on auctions over the past four to five years; these auctions are ongoing and expected to continue until 2018-2019. Rcom has expressed strong interest in gaining ground in the competition to deliver 4G services in India. It is likely that the sale of Reliance Infratel has been planned to reduce the company’s debt which stood at nearly US$6bn at the end of 2014, and to free resources for future service development. Rcom is in fierce competition for spectrum with the top three Indian carriers: Bharti Airtel, Vodafone India, and Idea Cellular and they invested heavily in the latest auctions, having made bids worth Rs 4,299 crore (US$ 671 mn) with an upfront payment of Rs 1,106 crore (US$ 172 mn) to become the first Indian carrier with a nationwide 800MHz footprint for future 4G rollouts.

It remains to be seen who the potential buyers may be, but it is likely that American Tower Corporation will be a candidate, as they are known to have a strong interest in expanding their footprint in the Indian market. Speculation around AMT’s acquisition of Viom Networks has died down, and TowerXchange would be surprised if AMT would want both Viom and Reliance Infratel’s portfolios. Indeed, with Viom seemingly more in a selling than a buying mood, at least in their domestic market, with GTL Infrastructure in financial difficulties, and with India’s other large towercos already strongly associated with Reliance competitors, one challenge for this process might be to attract enough credible bidders.