Mozambique’s impressive economic growth outlook, combined with a predominantly rural population, generates good tower sharing opportunities. However, while fast-growing operator Movitel’s parent Viettel remains closed to tower sharing, the country is unlikely to become the next area of expansion for any of Sub-Saharan Africa’s leading tower companies.

Viettel still an unlikely participant

Without participation from Viettel-backed Movitel, the country’s fastest growing and now largest mobile operator by subscriptions, Mozambique is unlikely to see the entry of any of Africa’s ‘big four’ tower companies into the market over the next year. However, depending on how Viettel’s strategies in Cameroon and Tanzania take shape, we believe the operator may warm to the prospect of tower sharing over time. In both markets, Viettel is up against two or more major regional players, with penetration rates already between 60-80%, and where tower sharing is the norm. Viettel initially tried to go it alone in Cameroon, but after losing most of its 3G exclusivity window to network roll-out challenges, it is understood to have eventually partnered with IHS Towers for co-location in some areas.

In Tanzania, Viettel is spending US$1bn to build out its networkLike in Mozambique, it will have a strong focus on expanding rural coverage and BMI expects it will partner with Helios Towers Tanzania in built-up urban areas, especially following the difficulties it faced in Cameroon.

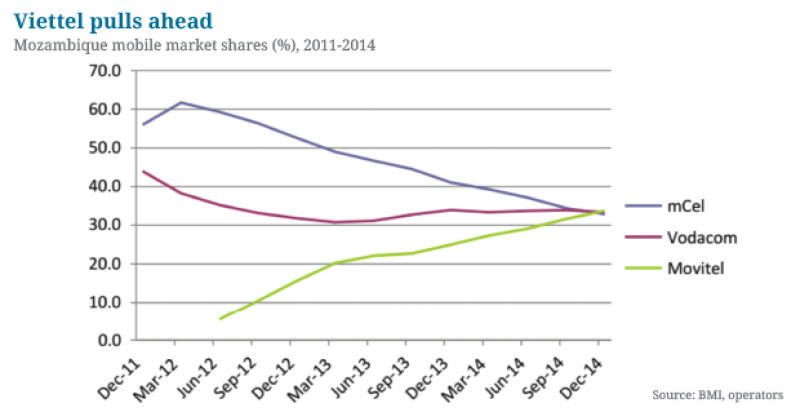

In Mozambique however, Motivel entered the market when the penetration rate had just reached 30%, leaving enough room for it to invest heavily in expanding networks to underserved areas and achieve a dominant position in less than three years. By June 2014, just two years after launching services, Movitel reportedly had 2,800 cell sites in Mozambique, accounting for around 50% of total towers in the country, as well as 25,000km of fibre, accounting for 70% of total national fibre coverage. BMI estimates that by the end of 2014 Movitel had 5.1mn mobile subscriptions, giving it a market share of 33.8%, narrowly ahead of Vodacom’s 33.4% share, and driving state-owned mCel’s sharp decline to a 32.9% share.

With its wider network coverage playing a key role in rapid subscriptions growth BMI expects the operator will seek to build up a comparable range of services to its competitors, such as mobile financial services and partnerships with content providers, before thinking of outsourcing infrastructure and inviting competition into underserved regions. But Viettel’s ambitious expansion plans, in Sub-Saharan Africa and elsewhere (Peru, Myanmar, Cambodia), will stretch its financial capacity. If investment costs in these markets scale up faster than planned, then the operator may consider boosting its coffers by exploring tower sharing options in Mozambique.

Vodacom and mCel explore other options

In October 2013, Israeli-based Mer Group announced that it had partnered with two of Mozambique’s leading mobile network operators to provide full turnkey tower site solutions. This includes site design, tower supply, site construction, and hybrid energy system design and implementation. BMI believes Viettel’s two competitors are the MNOs in question. Likusasa, the South African engineering and construction group, has also been contracted to build 800 sites for Vodacom in Mozambique. Strong competition from Movitel in its first 18 months of operation pushed its rivals to reduce operational costs by outsourcing network management. This is a growing trend across Sub-Saharan Africa, with the operational savings enabling operators to maximise their capacity to invest in new services and network expansion.

While Viettel remains closed to the idea of tower sharing, BMI believes continued outsourcing of network management and partnerships with rural network specialists is a more likely course of action for Vodacom and mCel.

Increasing regulatory pressure

Viettel enjoys a strong relationship with the Mozambican telecoms regulator and government, in no small part because its local partner SPI is owned by the ruling FRELIMO political party. SPI is a holding company and has a 29% share in Movitel.

However, the government is beginning to apply more pressure on telecoms operators to embrace network sharing in rural areas, in order to achieve universal internet access goals. In January 2015, the government announced three projects to encourage internet access in the country, among them the promotion of infrastructure sharing in rural areas.

While the government has not previously shown signs of belligerent behaviour towards foreign companies, meaning any drastic action such as confiscation of network assets is very unlikely, it may try to apply more pressure on Movitel to consider tower sharing through SPI’s stake in the company.

Whether or not added government pressure is likely to factor into Viettel or other operators’ willingness to share infrastructure in rural areas, BMI believes it is the most cost effective approach. Mozambique has a population density of 33 persons per sq km, which is considerably lower than in regional key markets; for example Tanzania has 53.7 persons per sq km, Cameroon has 48 and Kenya has 78.5. BMI estimates that 68% of Mozambique’s population lived in rural areas in 2014, with the urban population not expected to become a majority until 2050. Even though Mozambique is set to experience strong economic growth over the five years to 2019, lower incomes and spread out populations in rural areas mean few single tenant towers are likely to be profitable.

Economic boom, but politically tense

Though starting from a low base, Mozambique paints a promising picture in terms of economic growth. The country has vast reserves of both coal and natural gas. Mozambique began exporting coal in 2011 and by 2013 it already accounted for 12.2% of exports, at US$503mn, according to the latest data from the Bank of Mozambique. Exploration into new coal mines is still ongoing, underpinning BMI’s forecast for production capacity to increase from 6.1mn tonnes in 2014 to nearly 8mn tonnes by 2019.

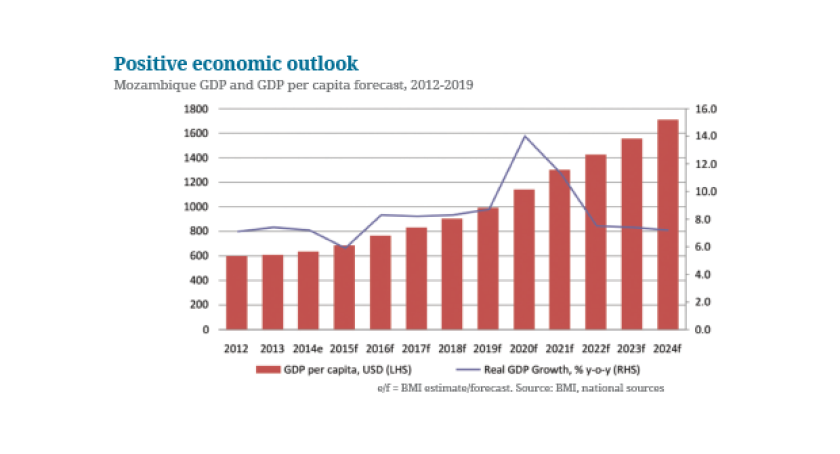

Meanwhile, Mozambique also has the largest proven reserves of natural gas in Sub-Saharan Africa. While the era of lower oil prices means investment into extracting the resources has been postponed, the sheer size of the reserves guarantees that they will eventually be tapped. BMI expects Mozambique to begin benefitting from natural gas exports around 2020, resulting in the sharp rise in real GDP growth to 14.5% for that year. That said, the offshore sites are likely to benefit from most of the early investment, which will limit the positive impact in terms of job creation and infrastructure development that would come alongside investment in onshore sites. Driven by rising export capacity, BMI forecasts real GDP growth to average 7.9% over the five years to 2019, and GDP per capita to double to nearly US$1,300 between 2014 and 2021.

While the majority of economic growth is set to come from the extractive sector, BMI nevertheless expects the benefits to feed through to private consumption growth. We forecast private consumption to grow by 6.3% a year on average between 2015 and 2019, well ahead of the regional growth rate of 3.3%. This macroeconomic trend is most closely tied with increased usage of telecoms services, and therefore bodes well for greater take-up of both voice and data services among consumers.

Politically, Mozambique has a more risky profile, due to ongoing tensions between the ruling Mozambique Liberation Front (FRELIMO) and the opposition Mozambican National Resistance (RENAMO). Following FRELIMO’s comprehensive win in the October 2014 general elections, RENAMO leader Afonso Dhlakama denounced the results as fraudulent and declared that his party would not take up its 89 seats in the 250-member parliament.

The party subsequently ended the boycott in early February 2015, in order to utilise voting rights for a forthcoming bill on regional autonomy in six of Mozambique’s 10 provinces.

Given FRELIMO’s decisive parliamentary majority the autonomy bill is unlikely to pass, which may in turn mobilise its supporters to take alternative action. This raises the risk of a resumption of violent insurgency, as seen in 2013-14, which could result in considerable damage to mobile network infrastructure. However, BMI does not believe this will lead to the outbreak of another civil war.

Aside from these tensions, Mozambique’s government is grappling with pervasive corruption and poverty. Without a strong political opposition to place checks on FRELIMO, the government has limited incentive to tackle corruption, other than the risk of alienating foreign aid donors. The high levels of corruption will make it difficult to ensure the equal distribution of wealth generated from natural resources, which will have an important impact on the level of demand for telecoms services from the rural population. This is one of the key reasons for our weak growth forecast for the 3G market, where we expect 3G subscriptions to account for just 17.3% of the entire mobile market by 2019.

Conclusion

Without Viettel on board, the presence of just two other MNOs