When we mooted the idea of covering the European market at the TowerXchange Meetup in Johannesburg last year, we were met with some sceptical looks. For many of the execs who have worked in the African market over the last five years, Europe is a far cry from the tower business as they know it. Disparate markets, a strong MNO attachment to the network as a competitive advantage, slow growth compared to the boom in Africa or Asia and a lack of obvious precedent for towerco activity make Europe seem a million miles from the meteoric rise of the towerco in emerging markets.

But once you scratch the surface, there’s a depth and scale in the European market which represent solid and sustainable growth. For the purposes of or coverage of the region, TowerXchange defines Europe by landmass rather than political boundaries, incorporating Western Europe, Central and Eastern Europe, Russia, Ukraine, Turkey and (where relevant) the CIS. Across this region there are around 30 independent towercos currently active and with at least 65,000 towers under management between them. According to TowerXchange’s recent ‘Top 110 towercos’ list, European towercos and infracos make up five of the top 20 towercos in the world and a further two of the top 20 towercos hold a major stake in the European market.

History of the European tower market

As the mobile market grew in the 90s and early 2000s, the majority of European countries were quick to adopt new technologies. Operators competed on network coverage and quality, and towers were built rapidly and often in close proximity to each other. As in the U.S., there was also plenty of existing infrastructure which could be employed including broadcast towers, utility structures and fixed line infrastructure. From this use of infrastructure evolved a different breed of towerco whose foundations lie as much in existing assets in the space, as in acquisition or build to suit.

Investment and appetite in the European tower market

While the European tower market won’t necessarily offer the kind of EBITDA multiples you might see in emerging market tower markets, there is certainly an appetite for investment in infrastructure.

Institutional and infrastructure funds have invested heavily in European infrastructure over the last decade and they have an increasing appetite for the long term, steady cash flows towers represent, and can outbid the private equity firms who often want to buy cheaper and target faster growth. However as with most infrastructure in Europe, there’s a shortage of assets and a lot of capital looking for strong investments. Circumstances are ripe for further growth in the European tower industry.

There’s a shortage of assets and a lot of capital looking for strong investments. Circumstances are ripe for further growth in the European tower industry

TowerXchange was told that on average buyers will pay 12x EBITDA in Europe for a tower portfolio, although Abertis’ estimated 16x multiple for the Wind Towers in Q1 2015 has shaken a conservative industry and will no doubt influence pricing in future. The disparity between operators’ expectations and towercos’ valuations in Europe has slowed the pace of European tower transactions for over ten years. As far back as 2003 Crown Castle’s entry into the European market was curtailed after they found themselves unable to agree valuations for European tower portfolios, and over the last decade the divestment of several more tower portfolios including Orange’s towers in Spain and Bite Group in Latvia have been postponed due to a failure to reach agreements on pricing.

However the appetite for investment in the market is at an unprecedented level and as more deals are closed valuations will be easier to reach, the gap between U.S. and European valuations will begin to close and TowerXchange believes we will see a deal pipeline beginning to fill up.

With funds such as Arcus and Alinda investing in several towercos across the continent, Macquarie and Brookfield active in the sector, and funds such as Providence Equity Partners, who have significant tower assets in Africa, teaming up with local partners to bid for European tower portfolios, the liquidity in the market promises a busy future for the European tower market.

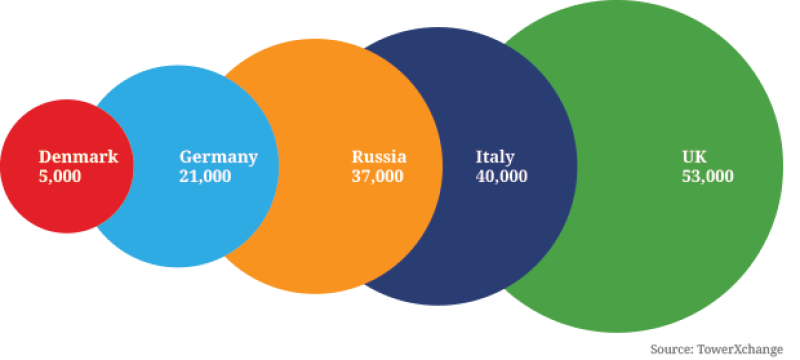

Figure 1: Estimated tower numbers across Europe (macro structures only)

Broadcast towers and the telecoms industry

The European and U.S. markets are differentiated from emerging markets by the volume of existing infrastructure which predates mobile phone usage. Broadcast infrastructure in particular, often originally owned by the state or state-supported entities, lends itself well to additional use for communications and has created towercos which are strong market leaders in their own countries, but with limited interest in an international portfolio. Among others Arqiva (UK), TDF (France and Germany), EI Towers (Italy) and Emitel (Poland) all offer both broadcast and communications infrastructure. Abertis has used a strong background in broadcast to create a more entrepreneurial towerco with international ambitions.

Broadcast towers lend themselves well to communications as they are generally in excess of 100m high (often as much as 300m), well positioned for maximum coverage ,and strong enough to support a large number of tenants. Towercos with both a broadcast and communications infrastructure can not only benefit from employing existing infrastructure but also from economies of scale when dealing with suppliers across both portfolios of tenants. Synergies between the two types of tenant also means they can more quickly achieve the scale needed to support skilled teams in house for technical work or project management.

Joint ventures, carve outs and network sharing

The fact that Europe lacks the volume of high profile tower deals experiences in other markets often masks the fact that Europe is actually ahead of much of the world in terms of infrastructure sharing. From sharing agreements to joint ventures and carved out infracos, there are very few markets in Europe where some kind of infrastructure sharing isn’t taking place.

Most notable among these are MBNL and CTIL in the UK. MBNL, a business spun out of T-Mobile and Three almost ten years ago (now incorporating T-Mobile’s merger with Orange to form EE), is a RAN sharing organisation which goes much deeper than any other partnership of its kind, seeing itself as a partner and service supplier to two shareholders. CTIL, although more of a simple passive infrastructure sharing organisation, represents the remaining UK operators, O2 and Vodafone, meaning that in the UK market there are barely any remaining operator-captive towers.

Further network sharing ventures include T-Mobile and O2 in the Czech Republic, Bougyes Telecom and SFR in France and various JVs in Sweden (Net4Mobility, SUNAB and 3GiS), where infrastructure sharing is mandated by the state.

Capacity, infill and heterogeneous networks

In a market where LTE roll out is well underway and the European Commission estimates 5G will not begin to roll out until 2020, network growth in the next years will centre around urban infill capacity and indoor solutions. As it becomes increasingly clear that heterogeneous networks will be needed to provide depth and flexibility of capacity, European towercos are seeking growth through the provision of DAS, metro cell and small cell networks to cities, local government and venues, as well as supplementing the macro network.

Figure-2

The European towerco landscape

There is no one model for independent towercos in Europe. Both publicly listed and private equity-backed organisations are thriving and the continent boasts a strong ‘middle market’ as well as top 20 global companies.

The market is dominated somewhat by the broadcast/communication tower hybrids mentioned above. Arqiva (with 10,550 telecom towers in the UK) and TDF (with around 11,000 towers available to the telecoms industry in France) lead two of the biggest towercos in Europe by some margin. In Germany the biggest towerco is Deutsche Funkturm, which offers over 24,500 structures, of which 8,500 are macro towers. Deutsche Funkturm is a subsidiary of Deutsche Telekom, and it is believed was intended to be spun out for a trade sale when it was created in 2002, although 13 years later it remains under Deutsche Telekom’s control. These organisations, while market leaders, have not demonstrated any ambition for significant expansion through acquisition in Europe.

There are also a good number of middle market towercos such as Wireless Infrastructure Group (UK), FTP (France) and Towercom (Ireland) who may not have the capital to bid for a large tower portfolio but continue to grow through smaller scale acquisitions and build to suit.

There are however several towercos in the market who are likely to have the appetite for a large scale acquisition, and could be the catalysts for an acceleration in the European transfer of assets to independent towercos. The Spanish company Abertis, fresh from their most recent acquisition of Wind’s Towers in Italy, are about to complete and IPO in order to raise the capital they need for further expansion. If recent rumours are to be believed, they are also keen to acquire Telecom Italia’s assets 11,000 assets in Italy before they undertake an IPO, giving them a strong market position in southern Europe.

Further East, Global Tower, spun out of Turkcell, which owns more than 20,000 structures in Turkey, and a total of almost 8,000 macro towers across Turkey and the Ukraine, could have an appetite for international expansion into Europe or Asia.

Staying in the East, Russian Towers, although currently geographically specific, boasts some impressive investors and could be in a position to raise the capital needed to acquire a significant tower portfolio in Russia when the opportunity arises. They would likely encounter competition from ESN Group should a substantial sale and leaseback come to market in Russia.

Two large international towercos, Protelindo and American Tower, also manage assets in Europe (Netherlands and Germany respectively) and could be well placed for further investment in the region should the opportunity arise.

The Americans are coming - looking to the future

With reliable grid access, a wealthy market and strong growth potential, there is also no reason why an attractive European portfolio would not raise the interest of another large international player, indeed, Crown Castle have been active in Europe in the past (before selling their UK assets to Arqiva) and US investors such as KKR have been linked to European deals in the past. Recent interest including Brookfield’s recent acquisition on the entrepreneurial Wireless Infrastructure Group and American Tower’s bid for the Wind portfolio indicate that the European market holds plenty of interest for the big US players, who certainly have the expertise in developed markets to offer a compelling story to European operators. As expectations close in terms of valuation, we may see a new dynamic in the European market, although as Abertis’ outbidding of American Tower for the Wind portfolio demonstrates, there is enough expertise and capital in Europe to challenge the established players.

Looking back as far as 2008, there have been at least ten tower deals of scale in the European market. It’s clear at a glance that Abertis have been the most acquisitive towerco in the market, spending at least €1.2 billion on towers in Southern Europe since 2012. Although KPN have conducted the most tower transactions, Wind, a subsidiary of Russian firm Vimpelcom, has divested the greatest number of towers in a deal which may well inform their strategy with other tower portfolios.

As MNOs consolidate the need to dispose of spectrum means MVNOs may well enter the market and passive infrastructure will be opened up more effectively in the hands of independent owners

With most of these deals taking place in the last three years, there is momentum building in the tower industry and it seems unlikely Abertis will be able to continue their charge across Europe unchallenged. There are several factors which may well increase the appeal of tower divestments; firstly the simple momentum driven by more and larger deals with higher values already taking place, which will bring more capital to the market and which will close the gaps in value expectation between operators and towercos. Secondly the drive for fibre and LTE+ roll outs, plus substantial debt from a recent wave of M&A activity across Europe, will force operators to lighten their balance sheets and reduce capital expenditure where possible. Finally, there may well be increased regulatory pressure on operators to share towers – as MNOs consolidate the need to dispose of spectrum means MVNOs may well enter the market and passive infrastructure will be opened up more effectively in the hands of independent owners.

What does the future hold for European towers?

With more deals rumoured in Southern Europe over 2015 and the potential for significant market consolidation in many Western European countries, there is plenty of opportunity for entrepreneurial towercos to find ways to grow the tower market in Europe. TowerXchange expects to see an increasing number of large scale deals happening over 2015 and 2016 and at least two large towercos expanding their reach across borders on the continent.

I’m delighted to be personally leading TowerXchange’s research into the European tower market, with a view to launching the first TowerXchange Meetup Europe, provisionally in London in Q1 2016. If you have a view on the European tower market, would like to be interviewed in the TowerXchange Journal or would like to participate in the TowerXchange Meetup Europe, please contact me at: frose@towerxchange.com.