It seems like the Mexican tower ecosystem, and the mobile operator market which it serves, is metamorphasising into a completely new structure, creating tremendous opportunities for savvy investors, and tremendous risks for those who fail to appreciate the nuances of the change. The headlines are obvious: Telcel is being forced to reduce their market share below 49%, leading to the potential disposal of assets, including the carve out of 10,800 towers to their own towerco Telesites. Meanwhile, AT&T acquired both third and fourth ranked operators Iusacell and Nextel Mexico, sparking a BTS feeding frenzy in the country.

Market overview

There are 103.4mn connections among a population of 124.5mn in Mexico, representing just 83% SIM penetration (compared to 152% in Costa Rica, 140% in El Salvador, 120% in Nicaragua, 111% in Guatemala, and 101% in Honduras). Smartphone penetration is growing whilst prices are falling, which means 42% of those connections are mobile broadband (market statistics courtesy of GSMA Intelligence, Q4 2014).

An RFP is due to be issued in October 2015 for a shared wholesale LTE network. Spectrum is being cleared for LTE and incumbent MNO trials have commenced, with over half a million subscribers already secured, so expect a surge in demand for infill sites. With AT&T entering the market, significant capital is already being deployed by Telcel and Telefónica to extend and densify their networks.

The MNO battle for subscribers remains concentrated at that higher value end of the Mexican market, and one could make a case that only Carlos Slim and Telcel seem to have much appetite to serve Mexico’s 60mn 2G, lower value customers, which in part explains Telcel’s dominant position in Mexico, which finally prompted newly empowered regulator IFETEL to seek to restructure the market.

Estimated breakdown of tower ownership in Mexico

Addressing the dominant position of Telcel; the carve out of Telesites

In July 2014 IFETEL, seeking to end Telcel’s dominant position in the market and to promote competition, directed Telcel to reduce their national market share in Mexico to less than 50%. However, this won’t bring about a “fire sale” of Telcel’s core telecoms operations nor of their towers; Telcel insist any assets will be sold at market prices.

At least 10,800 towers are initially being carved out to Telesites, which is operated from the offices of Grupo Carso; Carlos Slim is literally keeping the assets “in the family”. It remains to be seen whether Telesites might be compelled to be sold in the future, but most tower industry commentators, including TowerXchange, do not expect the assets to come to market in the foreseeable future.

The proof is in the pricing

Just how serious América Móvil is about creating a bona fida tower company might best be evidenced by the lease rates they charge for co-location. There is no suggestion that any América Móvil-derived towerco should offer discounted tenancies, but the maturity of Mexico’s existing towerco ecosystem means the pricing of leases and build to suit programmes is brutally competitive. If an América Móvil towerco charged significantly higher than market rates, few tenants would be attracted onto the towers, and status quo would be maintained.

However, while Telesites remains preoccupied with the integration of assets and the building of new towers for Telcel, it may be premature to expect much pro-active marketing of the sites for co-location – for example, it took years rather than months for India’s operator-led towercos to add many third party tenants to their towers.

The changing shape of Mexico’s tower market

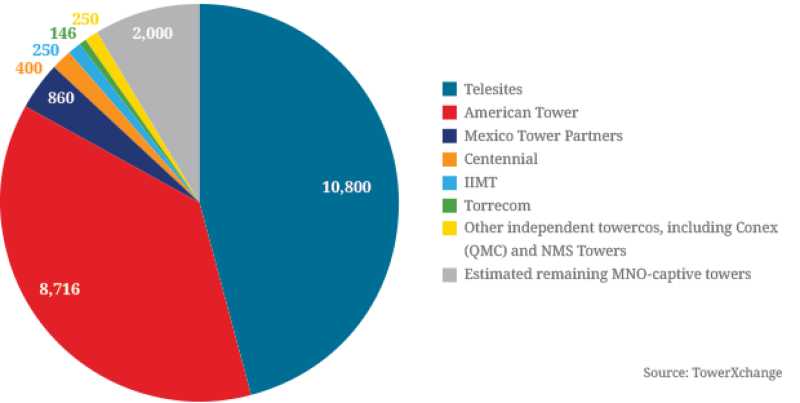

Mexico is now one of the most penetrated towerco markets in the world, with an estimated 91% of the country’s 23,000+ towers owned and operated by independent towercos, if one counts Telesites’ 10,800 towers as independently owned.

American Tower (AMT) has been established in Mexico since 1999, where it currently owns 8,716 towers. AMT’s notable recent Mexican acquisitions include a total of 2,138 towers acquired from Telefónica for US$445mn in Q3-4 2011, 883 towers acquired for US$250mn from Axtel in Q1 2013, and the acquisition of 1,666 towers from Nextel for US$398mn in Q3 2013.

Telefónica and Nextel (now AT&T) are believed, to retain a handful of remaining towers each – totaling perhaps 350. While it is not clear whether Telcel is transferring all their towers to Telesites, a form 6-K América Móvil filed with the U.S. SEC in April 2015 states "the Spin-off (of Telesites) will increase the number of towers in Mexico that are accessible to any telecommunications operator from 45% to 90%", suggesting ~2,000 towers remain operator captive, perhaps including some choice Telcel sites.

Mexico is now one of the most penetrated towerco markets in the world, with an estimated 91% of the country’s 23,000+ towers owned and operated by independent towercos

Between them, a host of independent towercos own a further ~1,500 Mexican towers. These include QMC Telecom (trading locally as Conex), NMS Towers, Torrecom, IIMT (which has 250 towers, plus the rights to install telecoms equipment on CFE’s electricity towers), Centennial and Mexico Tower Partners. Mexico Tower Partners (MTP) is the portion of the GTP business which Marc Ganzi resisted selling to AMT when the rest of GTP’s portfolio was sold to the US-giant for US$4.8bn in 2013. Don’t underestimate MTP – with around 860 towers, it might be less than a tenth of the size of AMT, but the combination of Marc Ganzi’s Digital Bridge and Macquarie’s MIRA makes them formidable competitors.

Mexican towercos report that the country’s 3G overlay is almost complete. Telcel has the most 3G work remaining, but Mexico’s other operators largely started with 3G, so have little left to do. Telcel are anecdotally reported to have the most 4G sites, but it is very early days for the 4G rollout.

Power costs are passed through to the tenant – it’s a pure “steel and grass” business model in Mexico.

AT&T market entry sparks BTS feeding frenzy

AT&T have made a smart move to enter the Mexican market by acquiring the Mexican wireless business of NII Holdings (Nextel Mexico) for US$1.875bn, as well as Iusacell for US$2.5bn, representing a total of almost 12mn subscribers, including a substantial proportion of the county’s high value, corporate subscribers. AT&T may have acquired premium spectrum at a distressed asset discount, but they have also bought two companies which own very few towers, having sold the vast majority to AMT.

Mexico’s tower companies have already met with AT&T executives who explained that their number one rollout priority will be co-location, particularly given the time to market advantages it offers. The entrance of AT&T, checkbook in hand, has triggered Mexico’s incumbent operators Telcel and Movistar to accelerate their own network investments

Mexico’s tower companies have already met with AT&T executives who explained that their number one rollout priority will be co-location, particularly given the time to market advantages it offers. The entrance of AT&T, checkbook in hand, has triggered Mexico’s incumbent operators Telcel and Movistar to accelerate their own network investments, sparking a feeding frenzy of build-to-suit projects. Some of our contacts have suggested that as many as 5,000 new towers could be built each year for the next three years, suggesting the Mexican tower count could rise by two thirds over that time – one of the fastest growing tower markets in the world.

AT&T’s acquisition of Nextel Mexico from the bankrupt NII Holdings represented the best possible news for Mexico’s tower industry, particularly for American Tower. AMT had acquired 1,666 of Nextel’s towers, paying what most analysts reckoned to be full value at US$239k per tower for sites with an anchor tenant with questionable credit worthiness. The conversion of that bankrupt anchor tenant to AT&T, even coupled with the consolidation of AT&T’s other Mexican acquisition Iusacell, represents a net win for AMT and for it’s competitors who similarly welcome an uptick in their tenants’ thus their own investibility.

A shared LTE network for Mexico

In another component of the government’s strategy to boost competition in Mexican telecommunications, the Mexican Transport and Communications Ministry has published a formal request for expressions of interest from companies and consortiums interested in deploying a US$10bn wholesale national broadband network in Mexico, utilising 90MHz of spectrum cleared in the 700MHz band. A full RFP is due in October. The so-called “carrier of carriers” would likely become a tenant on a significant number of Mexico’s shared towers.

How much will really change?

América Móvil has not sold much in the way of Telcel assets yet. Telcel has not shed many subscribers yet. Their preferred strategy seems to be to wait for churn and competition to gradually erode their market share below 50% and to pay whatever fines IFETEL throws at them in the meantime. But with AT&T and Movistar concentrating on the smaller, higher value end of the market, with Telcel not prepared to cede much ground there, and with América Móvil not needing the cash from a tower sale, thus retaining as much control over the towers, and upside, as possible, I feel little will change structurally in the Mexican market in medium term beyond an acceleration of build and co-location.

Conclusions: What does this all mean for Mexico?

The Mexican tower market should be considered mature; highly profitable but highly competitive. Any aspiring new entrant towerco into Mexico must also compete with seven incumbent Mexican towercos.

Remaining sale and leaseback opportunities are extremely limited in Mexico. Movistar (Telefónica), Unefon, Nextel and Iusacell (the latter two now owned by AT&T) have sold their towers. In the unlikely event of the Telesites assets coming to market, I don’t foresee there being credible bidders beyond AMT and MTP, with BMI analysis suggesting Mexico’s towers have already set a mark as the most expensive in LatAm.

There may be build to suit, IBS and special structure opportunities to be found by smart telecom real estate investors, but in terms of large scale towerco activity, Mexico is probably best left to the incumbents and to the publicly listed towercos with their relatively low cost of capital.

The towercos in Mexico, and their partners, have thrived and will continue to thrive even if Telesites brings its towers to market. While Mexico needs tens of thousands of additional towers and additional tenancies, the country will not support seven towercos in the long term. Some will remain smaller build to suit plays, some will inevitably be consolidated.

Implications for the CALA tower market

If América Móvil wholeheartedly embraces the independent towerco business model by proactively marketing the Telesites towers, and if that towerco thrives as we would expect it to, TowerXchange would expect to see the model replicated in several of América Móvil’s other CALA markets, with or without the prompting of local regulators.

América Móvil’s success may be viewed with a degree of jealousy by their competitors, but their success is a product of smart, flexible and sometimes aggressive market building. If the restructuring of Telcel and creation of Telesites really does represent América Móvil’s bona fida first towerco, it probably won’t be their last. There could be a major new player in the CALA tower market in the coming years!