North Africa is a sizeable market, which boasts a number of leading international players such as Vodafone, Orange, Etisalat, Ooredoo and Zain. Unfortunately, with the exception of a potential deal in Egypt, there have not been any other passive infrastructure transactions in the region. While there are merits for passive infrastructure transactions, in the last three to five years, North African operators have had to focus on other more pressing issues such as the Arab Spring or dealings with the government or regulator. However, we are starting to see some light at the end of the tunnel, with ROIC optimisation and increasing 3G/4G investment needs and take up driving the passive infrastructure transactions discussion between operators.

Mobile telecom markets reaching maturity…

Algeria, Egypt, Libya, Morocco and Tunisia are all sizeable economies accounting for a total GDP of US$790bn. At present, North Africa accounts for a total of 240mn subscribers. Voice penetration is already above 100% in most markets. Data subscribers and data usage are expected to grow, fuelled by investments in 3G and LTE networks. Most countries have three mobile operators, with the exception of Libya which is a duopoly. Competition is expected to intensify, with the planned entrance of a number of MVNOs in some of the markets (e.g. Telecom Egypt move to the mobile market as an MVNO, the entrance of two MVNOs in Morocco and one MVNO in Tunisia).

…while passive infrastructure markets are still in their infancy

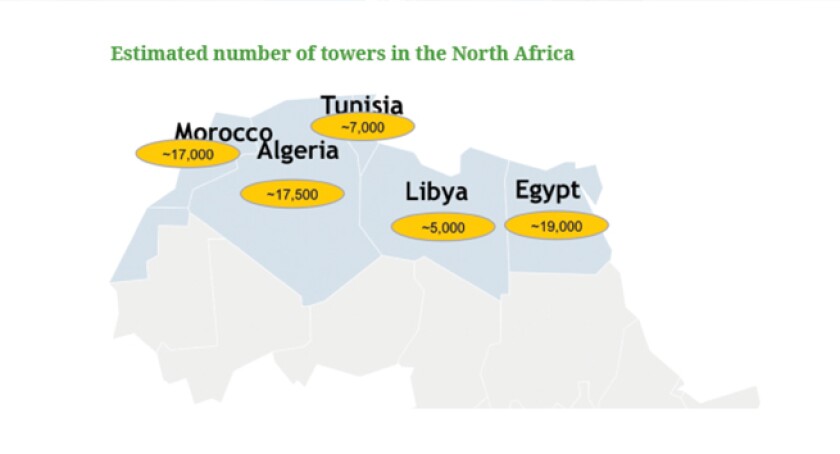

Delta Partners estimates over 65,000 mobile telecom towers in North Africa, the most sizeable countries being Egypt (~19,000 towers), Algeria (~17,500) and Morocco (~17,000), followed by Tunisia (~7,000) and Libya (~5,000). The markets in North Africa have good 2G population coverage (between 98%-100%), which indicates limited future demand for towers for coverage purposes. Therefore, future rollout is expected to be mostly driven by 3G and 4G deployments and growth.

Site sharing and bartering among operators is not very common: we are only aware of Mobilis and Djezzy’s agreement to share towers in Algeria and Meditel and Wana’s agreement in Morocco. However, managed services, network rollout and tower installation are well spread out and are usually provided by independent players such as Mobiserve, Alkan Networks, EEC Group and Tubprofil, which helps to set the scene before sale-leaseback agreements come into play in the future.

The ongoing sale of ~3,000 towers belonging to Egypt’s Mobinil (majority owned by Orange) is the first real attempt at a sale-lease-back deal in the region. After a lengthy process spanning over two years (2013 and 2014), the transaction is expected to be completed this year. Bidders have not been disclosed. But a transaction of this sort may pave the way for future deals in the market, setting a precedent in the region.

Estimated number of towers in the North Africa

So why have there been so few passive infrastructure transactions in North Africa?

While there is no clear answer for the lack of passive infrastructure transactions in the region, a possible reason may have been due to the past Arab Spring events that have re-shaped a significant part of the political landscape of North Africa. Furthermore, North African operators may have turned their focus in the past on other more pressing issues related to network rollout, licensing requirements, competitive scenarios and dealings with the government or regulatory authority (e.g. VimpelCom’s situation with Djezzy in Algeria).

However, the North African markets are showing signs of improved macro and political stability, liberalisation and enhanced regulatory frameworks. This, coupled with the continued demand for passive infrastructure and the presence of international operators who have passive infrastructure outsourcing on their agenda, could bring North Africa back to the top of the agenda again since it adds to the diversification of the portfolios of tower operators and provides potential attractive growth prospects. From an operator’s perspective, the benefits (including the impact on ROIC) from the sale of passive infrastructure, increased competition with the introduction of MVNOs in these markets and the bigger investment requirements for network upgrades (including LTE), can make operators in North Africa re-consider the merits of passive infrastructure sale/outsourcing.

More passive infrastructure activity expected in the region?

North Africa is one of the last untapped passive infrastructure markets. Recent political turmoil during the Arab Spring had reduced investor confidence and raised issues regarding direct investment schemes and exit strategies. However, the improved macroeconomic stability, together with increased focus on infrastructure sharing on behalf of regulators and MNOs, has led to an improved outsourcing readiness across the region. Therefore, we expect more passive infrastructure deals to occur in the region. Driven by the presence of international mobile operators, we foresee that there will be further consolidation in North Africa, in particular Egypt, and expect to see deals in larger markets such as Algeria and Morocco.

Main drivers of the passive infrastructure markets in North Africa (click the image below to enlarge)