In December 2014, STP closed a transformational 3,500 site deal with XL Axiata, a deal which concentrated over 90% of STP’s revenue as coming from Indonesia’s Big Four operators from 2015 onwards, while consolidating their position in a competitive tower market. Despite these critical motivations, the deal has been criticised by some commentators and analysts due to the fact that XL Axiata unilaterally created many of the terms, initiating a bidding competition among towercos. During the recently concluded Mobile World Congress in Barcelona, TowerXchange sat with Nobel Tanihaha, President Director of STP, to discuss the deal in detail and get his take on why the deal made sense for the towerco.

The December 2014 STP-XL Axiata deal consolidated STP’s position as number three towerco in Indonesia with 6,651 sites, behind Tower Bersama (with 15,195 towers) and Protelindo (11,216) but was criticised by commentators for terms such as discounted rental rates which could create a harmful precedent in the industry.

However, if we look at the consequences of the deal as explained by the company’s President, Nobel Tanihaha, it becomes clear that STP has created a lot of value through this transaction.

At the time of the transaction, Moody’s suggested that “the (XL Axiata) sale is credit negative for the Indonesian tower industry because it increases the probability of increased price competition”. On the other hand, Fitch said “Fitch does not view the XL/STP deal as setting a precedent for tower rental pricing, and should not lead to heightened price competition. In sale and lease-back transactions, low lease rental payments can be offset by larger up-front cash payments, so they do not necessarily act as pricing benchmarks for standard non-sale leasing agreements.”

Nobel’s commented on the topic during our meeting in Barcelona “I tend to agree more with the Fitch view. Just to add more on the topic, a sale and lease back deal should not be viewed in the same way as new build or co-location. Sale and lease back is about IRR on the deal which connects lease rate and sale price. It has nothing to do with new construction and co-location pricing. Greenfield projects have different dynamics of costs depending on the location and tower type, whereas co-locations have to do with location and speed to market.”

Successful bond issuance

In February 2015, STP sold a US$300mn, five-year bond on the international market - its first bond and a great step forward for the company. During our meeting, Nobel noted how the bond wouldn’t have been possible without the XL Axiata deal which contributed to scaling up the towerco to the desired level in order to issue a bond and become a credible player among the investor community.

Deal structure made sense for STP

Additionally, Nobel highlighted how the XL deal was right on track within STP’s acquisition EBITDA parameters, specifically at 8.2x versus the company’s 6-9x historical average. He admitted that XL Axiata designed the deal unilaterally, which was an unprecedented move in the Indonesian industry, and effectively selected the winner purely on the basis of its bidding price. However, the time was right for STP as TBIG was dealing with the PT Telkom deal and unable to bid and Protelindo simply didn’t put up a fight, allowing STP to close the deal at a reasonable price of US$460mn.

In fact, with an average price of US$131.4K per tower, the deal didn’t appear overpriced and the only substantial difference compared to standard sale and leaseback deals is the absence of an escalator for opex, which is on paper a bad deal for STP. However, if we look closely, STP’s opex has been dropping steadily, allowing the company to maintain an EBITDA margin at or above 83%. Further, the co-locations on XL Axiata towers did come with escalators, and combined with escalators already included in STP’s existing tower tenancies, the inflation risk is fully covered. So even if the rental price set up by XL is lower than average, thanks to STP’s ability to keep its costs down while scaling the business up, the deal is still profitable, according to Nobel.

the deal might have not made sense for TBIG or Protelindo, but it did help STP to consolidate their position as the third towerco in the country, and was critical to their bond issue

STP has been courting XL Axiata for quite some time now and Nobel recalls an attempted deal back in 2007 which didn’t materialise: “Since 2007, we’ve learnt a lot and we are now in a stronger position and were able to leverage the competency of an in-house team which includes a number of former XL Axiata employees. Thanks to their past experience, this recent deal was a pretty fast one. They knew the assets and were able to read through the terms very efficiently. Minimal due diligence was needed, which is a plus!”

STP acquired a portfolio with an average tenancy of 1.66 with Hutchison as its main supplementary tenant. However, Nobel noted that Indosat and Telkomsel have historically avoided renting competitors’ sites, so now the towers are an independent towerco’s hands, STP can target them and hopefully acquire them as tenants on the former XL Axiata towers, leveraging its strong existing relationships with both MNOs.

In conclusion, Nobel highlighted how the deal might have not made sense for TBIG or Protelindo, but it did help STP to consolidate their position as the third towerco in the country, and was critical to their bond issue.

Tenancy revenue increasingly concentrated on Indonesia’s ‘Big Four’ MNOs

“We were very busy cleaning our balance sheets,” Nobel told me. “In fact, we wrote off Bakrie from our books in order to eliminate bad debt. That resulted in our revenue dropping US$10mn per year but at least, we have cleared our books and any funds coming from that stream is actually a plus.”

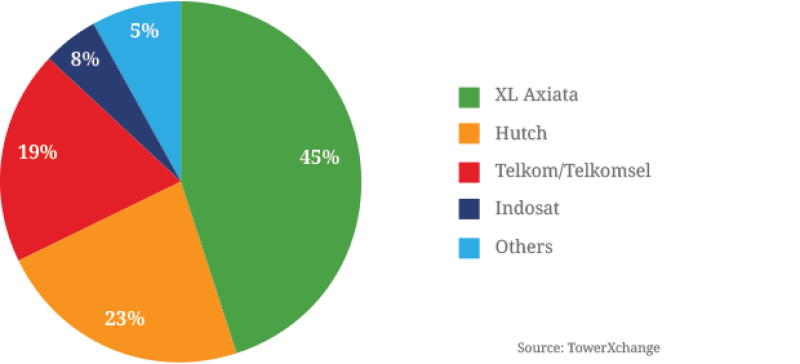

Bakrie Telecom is part of Indonesian giant Bakrie Group, which has been carrying a considerable debt load for quite some time now. Currently, the company is looking at restructuring its debt and preparing a repayment plan for its creditors. As Bakrie Telecom had been STP’s counter-party in their second sale and leaseback in 2009, back in 2010 Bakrie Telecom represented a massive 53% of STP’s revenue. Thanks to the XL Axiata deal, Bakrie represents only 9% of revenue and will not be booked as revenue going forward, with previous debts now written off. Indeed post-acquisition and subsequent to excluding all of Bakrie related revenue, 92% of STP’s revenues come from Indonesia’s ‘Big Four’ operators (XL Axiata 45%, Hutch 23%, Telkom/Telkomsel 19% and Indosat 5%). This restructuring has a very positive effect on STP’s long term credit worthiness.

92% of STP’s revenue post-XL Axiata deal comes from Indonesia’s ‘Big Four’ MNOs

Diversifying revenue streams

In the meantime, STP continues to diversify its revenue streams and Nobel highlighted a few of their competitive differentiators during our chat.

“We are very involved in bringing fibre to the home and indoor right now. Thanks to the 20-year permit STP was granted, we have the right to dig and install fibre and this is a core expansion area for us at the moment.”

Additionally, STP is investing in micro-cells and Nobel explained the ratio behind this decision at the end of our meeting “we want to enter the density game, not only the coverage one. To solve density issues, you can’t rely exclusively on building macro-sites anymore, especially with the advent of 4G LTE. In-building solutions are critical as data will keep expanding indoor rather than outdoor.”

While wrapping up our chat, Nobel told me that STP is extremely satisfied with how things are moving and that since the bond, the price has been steadily trading up although the desired liquidity will take some time to kick in.

The conclusion we can draw from this is that the XL Axiata deal was a good match for the towerco and happened at the right time for both companies. STP has been able to leverage its stronger position while scaling up its portfolio considerably and according to its President Director, the deal’s unusual terms were still favourable for the towerco.